Click here to download the report

Key Highlights

- Nerolac introduced Neropoxy Solvent Free coating for water pipelines and C5 Fluoro Polymer Coatings, IPNet, Polysiloxane, and anti-carbonation systems for High-Performance Coatings

- The Managing Director, Mr. H.M. Bharuka, retired after 36 years of service, and Anuj Jain was appointed as the new Managing Director with effect from April 2022

- The company operates in 2 segments, Industrial and Decorative, with their revenue ratio being 45:55 in FY 2022

- The company integrated its subsidiaries Marpol Private Limited and Perma Construction Aids Pvt Ltd for better market penetration and increased operating efficiency

- The company added a resin facility in Sayakha and an emulsion manufacturing facility in Amritsar in FY 2022

Indian Paint Industry

- Valued at $8 billion

- Asian Paints leads the industry with 44.33% market share, followed by Berger Paints (11.73%),

- Nerolac (8.94%), and other players capture the remaining 35%

- Grasim’s entry with a 1.3 billion litres capacity expansion outlook. It plans to set up plants with a production capacity of 1332 million litres per annum

- Major growth driver in the industry is the rise in disposable income of the average middle class, urbanization, and the growing rural market

102 Years of Legacy in the Paint Industry

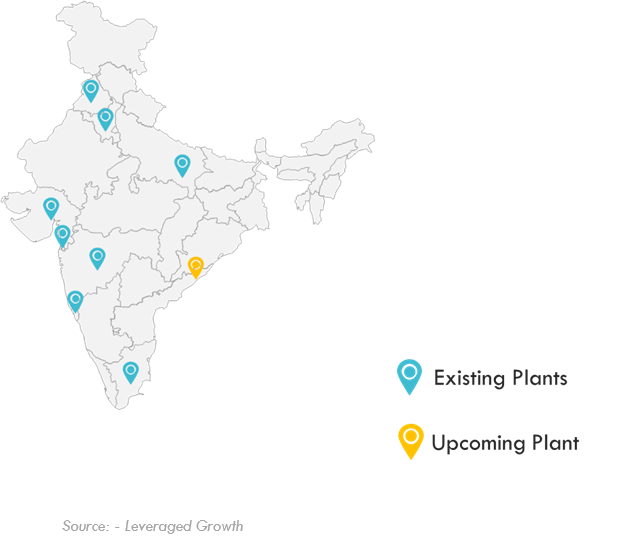

Kansai Nerolac Paints Ltd. (NSE: KANSAINER), now in its 102nd year, is a subsidiary of Kansai Paint Co., Ltd., Japan. It is one of India’s prominent players in the Paint industry, with leadership in industrial coatings and a sizable share in the General Industrial and High-Performance coatings space. Paints are used on the finishing lines of electrical components, material handling equipment, automotive industries, and other general-purpose industries. As of 31 March 2022, the Company had eight manufacturing plants with subsidiaries in Nepal, Sri Lanka, and Bangladesh. Nerolac has entered and grown its presence in new markets and product segments, such as High-End Wood finish, Construction chemicals, Auto Refinish, and Coil coatings.

Journey

The company began its journey as Gahagan Paints and Varnish Co. Ltd more than 100 years ago in Lead Industries, UK, 1933, acquired the company. In 1957 the company was renamed Goodlass Nerolac Paints Ltd. Later, in 2000, the company became a subsidiary of the 8th largest paint company globally, Kansai Paints, Japan. Katsujiro Iwai, following Japan’s efforts to minimize the reliance on imported goods, launched Kansai Paint in 1918. Because of the economic instability, Kansai struggled to survive in the initial years, but when the company launched the first lacquer paint, it established a firm foothold. By 1933, the Company had spread its wings outside Japan. In the late 20th century, Kansai looked at Asian markets for further growth. It was rebranded as Kansai Nerolac Paints Ltd in 2006. Kansai Paints currently holds a 75 percent share in the company. Nerolac completed the merger of its Indian subsidiaries, Marpol Private Limited and Perma Construction Aids Private Limited. The Scheme became effective on 21st October 2021, according to necessary filings with the Registrar of Companies.

Key Personnel

Nerolac witnessed a significant key personnel change this year with Mr. H. M. Bharuka, Managing Director, retiring after 36 years of service. He joined the company in 1985 and became its Managing Director in 2001.

Under his leadership, KNPL won numerous accolades in various areas, notably the Golden Peacock Award for Corporate Governance, Best Managed Company by Business Today, Great Place to Work by GPTW, and recognition as an ESG leader in India by CRISIL. Mr. Bharuka featured amongst India’s Top 50 CEOs and was awarded a lifetime achievement award by the Indian Chemical Industry. Mr. Bharuka served as the first non-Japanese Director on the board of Kansai Paints, Japan, and is also credited for leading KNPL’s expansion into the Indian Subcontinent.

Mr. Anuj Jain, Managing Director, was appointed on 1st April 2022. He joined the company three decades ago as a management trainee. He has been a part of the board as the Executive Director since2018.

The Indian Paint Industry

The Indian Paint Industry, valued at around USD 8 billion, is the fastest-growing paint economy, with double-digit growth over the past two decades. With over 3,000 paint manufacturers, this sector encompasses almost all global majors. 75% of the industry can be attributed to architectural/decorative paints and 25% to industrial paints.

Within the Indian decorative segment, Asian Paint and Berger Paints are the largest players, with the segment contributing more than 80% of their overall revenues. The Industrial paint segment is highly dependent on the automotive sector, which has been a leading consumer of industrial paints, with 40-50% of demand coming from it. Moreover, Grasim Industries and JSW Group entering the industry combined with expansion interests by existing players are expected to change the structure and competition in the Indian paint and coating manufacturing industry by 2023. The Covid pandemic had hit the Indian Paint Industry in the previous two years. Nonetheless, significant participants have forayed into new investments along with capacity expansions.

Though the industry is growing, it is also prone to the major risk of change in raw material prices, such as resins, pigments, solvents, additives, and oils, which can hamper its growth. Besides creating low Volatile Organic Compounds (VOC) and eco-friendly paints, industry players are innovating to develop nanopaints, a type of paint that can alter surface properties according to user-defined parameters. This recent innovation has helped manufacturers create a product that can improve energy efficiency by helping structures absorb and reflect thermal energy. The key areas include reducing the use of Formaldehyde for indoor pollution and fast painting turnaround through quick drying and no odour formulations.

Business Model

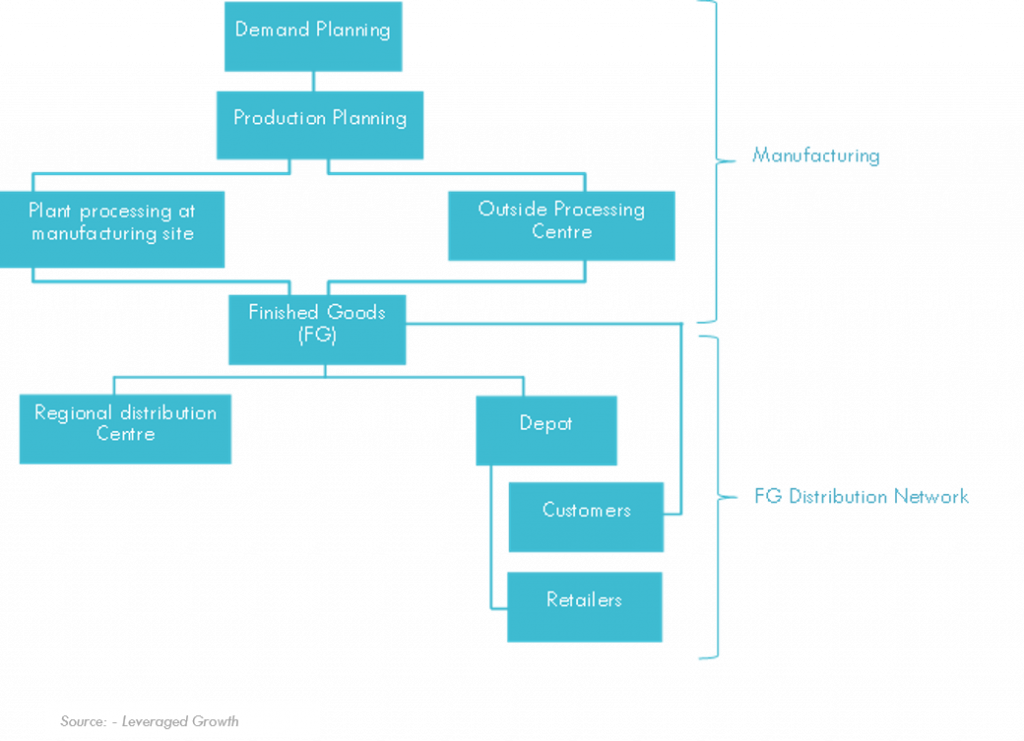

One of the most critical factors for a paint company is its supply and distribution network. KNPL has a Pan-India presence with 99 sales locations and a large supply base totalling more than 500 direct raw material suppliers, of which roughly 350 are local. To promote local growth, the Company tries to source its raw materials from local vendors; but some specialized raw materials are imported as the Company

has no other alternative.

The Company operates in two segments, Industrial and Decorative, with the Industrial to Decorative revenue ratio remaining at 45:55 in FY 2022:

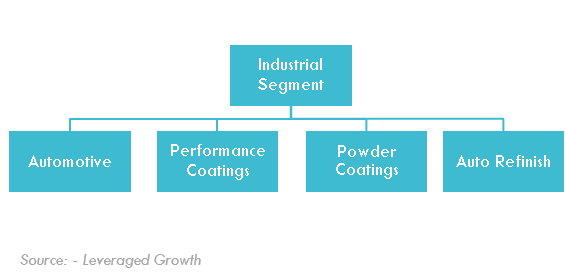

1. Industrial Segment – Multi-locational manufacturing setup has been influential in maintaining its leadership position. Price increases have been insufficient to offset the inflation in material prices. This segment continues to witness inflation on a higher solvent base and delays in taking inadequate price increases. The company expects further price hikes in the first quarter of FY 2023.

2. Decorative Segment – Good demand momentum was observed in the second and third quarters of FY Nerolac is reviving its advertisement campaigns to focus on this segment. Price hikes have been sufficient to hedge against inflation issues observed in the markets.

Nerolac has been gaining market share in the Industrial component area, whereas its decorative segment market share has been falling. This could be because of the lower ad spending during the previous two years. In response, the company is trying to increase advertisement expenditure and build its portfolio across segments.

Subsidiaries

KNPL previously had three Indian and three overseas subsidiaries in Nepal, Sri Lanka, and Bangladesh. To enhance growth and to de-risk the business, the Company forayed into the business of Adhesives and Construction Chemicals. The company has successfully integrated its subsidiaries, Marpol Private Limited and Perma Construction Aids Private Limited, into itself to leverage synergies, resulting in better market penetration and operational efficiencies for the Powder Coating and Construction Chemicals segment. The Company is also looking forward to having its footprints globally, thereby increasing operations inorganically.

SWOT Analysis

Strengths

Technological advantage

- KNPL’s hallmark of success is technological innovation and a big focus on R&D. This has helped the company deliver high-quality service with quick turnarounds and cost savings while reducing its environmental impact.

- The Company uses advanced digital tools like Machine Learning and the Internet of Things (IoT) to secure business benefits. Recently, they have shifted from text-based to digital content, including augmented reality ads and 360-degree videos, giving consumers a more immersive experience.

Branding and Marketing Strategy

- The company has launched multiple brand-building campaigns for “Beauty Gold Washable” and “Excel Mica Marble Stretch and Sheen” products throughout the year. It highlights the protection features of exterior products and communicates the durability through strategic associations with top news channels in several languages.

- The company partnered with television giants, including IPL, Big Boss, etc., to reinstate their brand proposition.

Robust Supply chain

- The Company has deployed cutting-edge IT tools to improve the efficiency of its supply chain andsales process. The Company has adopted SAP Leonardo, which brings together ML, IoT, Blockchain,and Big Data

Research and Development

- The company uses cutting-edge technologies in its Research and Development setup, which constantly improves through support provided by its parent company, Kansai Paint Co., Ltd., Japan, and the entire Kansai group of companies.

- Activities carried out in Research and Development include developing new products for Automotive, Performance Coating, and Decorative segments along with up-gradation of critical processes for cycle time reduction and energy saving.

Weaknesses

Change in customer’s preference

- The products become obsolete too quickly due to rapid urbanization and increasing disposable income, especially in the decorative segment. As per Mordon Intelligence Report, demand for vinylbased wallpaper is expected to grow by 28.5% CAGR over 2019-2024, impacting the sales of the paint segment.

Geographical Market

- The Company does not have a well-diversified geographical market with a negligible presence in East India. Most of its plants are located in the north, with a few in the south and west of India. KNPL can try expanding in the Eastern Region, which will help the Company get easier access to its Bangladesh subsidiary, subsequently minimizing transportation costs and time.

Opportunities

Infrastructure Development

- The market expectation is that the government would continue its help in promoting infrastructure, which adds to the industry’s momentum.

New Market segments

- Globally, there are very few players who produce insect repellent paints. These paints can be used to repel or kill insects by the active insecticidal ingredients present in the paint. Currently, no paint company in India has manufactured such kinds of paint. Thus, KNPL can try capturing this opportunity.

Threats

High Competition

- Although KNPL is the market leader in the industrial segment, there is a threat of getting replaced due to tough competition and continuous technological innovation by other organized players like Asian Paints, Berger Paints, etc. Grasim Industries and JSW Group entering the industry combined with expansion interests by existing players will further increase the high competition.

Changes in government rules and regulations

- Most paints manufactured in India contain harmful substances like mercury, lead, etc. These paints emit a significant amount of VOCs into the atmosphere during the painting process, affecting

Differentiating Strategies

- Technological Orientation – Their in-house R&D facilities and high-end technology across strategically located plants enable unique need-based solutions for customers. Close collaboration with Kansai Paint Co., Ltd., Japan, and its group companies, Oshima Kogyo Co. Ltd., Japan, Cashew Co. Ltd., Japan, and Protech Chemicals Limited, Canada, provides high-end, home-grown technology solutions catering to the specific needs of the Automotive Industry. Some solutions created using this collaboration are high solid anti-chip primer with a reduction in VOC and Metallic colours with 3C-1B Technology which offer energy conservation and increased productivity.

- Product Innovation – Focusing on continuous innovation in diverse market segments enables improved finish quality, consumption, and environment-friendliness. An example of the same is applying their environment-conscious “Healthy Home Paints” positioning. The company introduced a complete line of 100% Heavy Metal Free by Design and Low VOC products, providing painting solutions across several pricing ranges.

- Focusing on Capacity Expansion – All the manufacturing plants are strategically located near the key OEMs (Original Equipment Manufacturer). These plants have in-house resin & emulsion manufacturing capabilities. This year, the company added a resin facility in Sayakha and an emulsion manufacturing facility in Amritsar (Goindwal Sahib).

- Continuous market segment and geographic expansion – KNPL strengthened its tie-up with the Italian company ICRO Coatings to focus on high-end wood coatings. The Company is also augmenting its PU category wood-coatings range to ensure a strong presence in wood coatings. During the year, the company focused on increasing the premium product range while broadening its health and hygiene divisions. Moreover, the company expanded beyond India through acquisitions in Nepal and Bangladesh and a Greenfield JV project in Sri Lanka.

Michael Porter 5 Force Analysis

1. Barriers to entry –

- Distribution Network- The top companies in the list have a comprehensive sales and distribution network spanning all across the country and outside, thus making it difficult for a new player to enter. Nerolac has established an extensive distribution network with over 99 depots and seven distribution networks.

- High Working Capital- Procuring imported raw materials in bulk is time-consuming and pricesensitive, while days of trade receivables are generally 30 days. The raw material prices are affected by the volatility of crude derivatives, titanium dioxide, and monomers prices.

- Technology- The industrial segment is more technology-intensive than the decorative segment. Most unorganized players cater to the decorative segment due to zero or minimal access to technology. Nerolac has built a comprehensive R&D setup, upgraded its IT infrastructure, and works with its parent company, Kansai Paint Co. Ltd., to leverage technology.

2. Bargaining power of suppliers –

- Most of the raw materials are petro-based derivatives, thus making the paint industry critically dependent on suppliers. Therefore, the bargaining power of suppliers is moderate to high. E.g.- one of the raw materials, Titanium dioxide, faces a global supply shortage, leading to higher prices by suppliers.

3. Bargaining power of buyers –

- Given the Indian market, customers are primarily price-sensitive. With close substitutes offered by Asian Paints and other industry giants and the entry of Grasim, the bargaining power of the buyer seems to be on the higher side.

4. Rivalry among competitors –

- This industry has tough competition given the oligopolistic nature with a few players in the organized sector. Due to barely any product differentiation, advertising and distribution play a key role. In the unorganized sector, competition is majorly based on pricing.

5. The threat of substitutes –

- The threat of substitutes in this industry is minimal. The only substitute for paint currently used is wallpapers, but the buyer’s propensity to substitute is low due to high price and low durability.

Branding and Other Initiatives

- This financial year, the company introduced a new brand expression of “PAINT+.” PAINT+ embodies the commitment to offer quality and services beyond essential paint solutions leveraging their Japanese expertise and centennial legacy. Nerolac’s focus on innovation and technology has led to the introduction of newer paint solutions like the “Neropoxy Solvent Free Coating” for the internal coating of water pipelines and C5 Fluoro Polymer Coatings, IPNet, Polysiloxane, and anti-carbonation systems for high-performance coatings segment. Also, the company introduced new products like a high solid anti-chip primer with a reduction in VOC and Metallic colours with 3C-1B Technology which offer energy conservation and increased productivity through collaborations with Kansai Paint Ltd.

- The Nerolac brand has increased its brand value through various marketing initiatives. Contractors and painters are the essential influencers for the brand, even though the end-users make the ultimate decision. Therefore, KNPL gives importance to regional and straightforward communication at the store level.

- “Ab Walls Rahe Saaf aur Safe” was a fundamental proposition this year for the product “Beauty Gold washable,” focusing on the stain reduction feature.

- The Company undertook several livelihood and skill enhancements through rural areas training programs. The company collaborated with various education institutions and worked on development activities, including building classrooms and drinking water infrastructure. This contributed to their CSR initiatives and possibly helped get manpower.

- The company developed an application named “Pragati,” which painters can use to redeem loyalty points and receive real-time payments. It also includes various features and practical tools for colour picking, colour estimation, and tutorial videos providing knowledge and tips.

- The company was awarded the Best Supplier award from ‘Honda Motorcycle and Scooter India’ for the 4th consecutive year in the supply chain category.

Financial Analysis

1. Inflationary Pressure Weighing Down Margins: Profit after Tax (PAT) has been in the range without much volatility in the past ten years except FY16. The unusual spike in FY16 as Profit Before Tax increased by ₹535 crores is attributed to the sale of the company’s land and building at Perungudi, Chennai. High wages, low productivity, obsolete machinery, and expansion infeasibility led to the shutdown of the Chennai unit.

Revenue from Operations registered a 24.7% growth YoY basis, standing at ₹5948.90 crores. However, the PBDIT fell by 23.3% as the company grappled with high inflation across major raw material categories. Input prices increased due to global supply constraints, volatility in exchange rate & crude oil prices, and the MNCs invoking their “force majeure” clause in the wake of the pandemic. Force majeure refers to the non-fulfilment of the contract due to unforeseeable circumstances. The erosion of investment made in the company’s Sri Lankan subsidiary, caused by Sri Lanka’s severe political and economic downturn, raised the Exceptional items to ₹11.39 crores from the previous year’s ₹10.82 crores.

The company took cost-cutting initiatives and a 21% price hike to mitigate the inflation. However, the profit margins came under pressure. PAT for FY 2022 stood at ₹373.33 crores from ₹530.65 crores in FY21, down by 29.5%. Operating Profit Margin fell to 10.9% from 17.7%, while Net Profit Margin down to 6.4% from 11.2%.

In comparison, the market leader Asian Paints, registered a PAT of ₹3048.81 crores in FY 2022 from ₹3206.75 crores in FY 2021down by 4.9%. Also, the company witnessed a 34% growth YoY in its revenue from operations, standing at ₹29101.28 crores.

2. Very Low Debt: The capital expenditure (CAPEX) is estimated to be ₹175 crores for FY23, which KNPL will fund mainly through cash accruals. The company finances a significant portion of the CAPEX through internal accruals with minimal dependency on debt financing and has maintained a sizable liquidity surplus of ₹313 crores as of 31/03/2022. The working capital limit of ₹230 crores is underutilized, and cash reserves are enough to cover incremental obligations.

The debt level has declined from FY10 till FY17 as it had been repaying its debt. However, after FY17, the debt level started rising again as the company took term loans and overdrafts to acquire assets under management and fund its short-term requirements.

The adjusted net debt, i.e., (total debt-cash & bank balance), is negative. Also, equity has increased proportionately compared to the increase in debt over the past years. The debt-toequity ratio for the company has always remained below 1 (0.02), which is negligible.

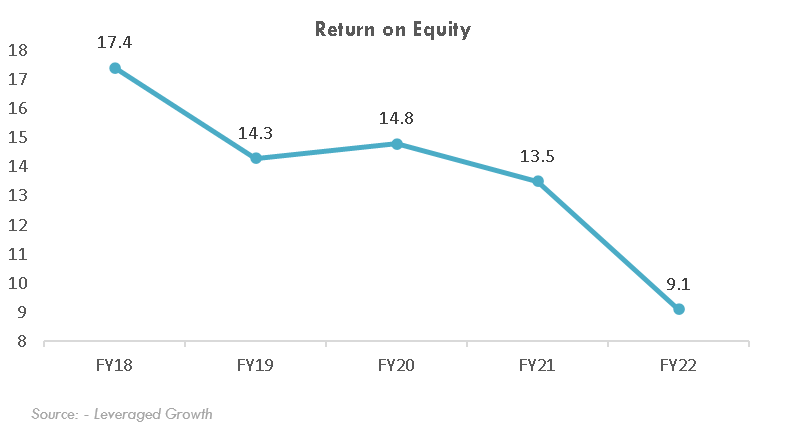

3. Return on Equity (RoE): RoE has been declining due to low asset turnover. Subdued demand for the paint products due to unfavourable macroeconomic factors like inflation and the lagging automotive paint industry brought down the RoE to 9.15% from 13.5%. Return on Capital Employed (ROCE) plummeted to 12%, owing to losses from subsidiaries and flat returns on a large liquidity surplus. The EPS also stood at ₹7, compared to ₹9.9 in FY21.

The company’s financial leverage has decreased from 1.61 in FY11 to 1.38 in FY22, contributing to a decrease in ROE. Therefore, KNPL’s low Debt/Equity ratio suggests that RoE is generated by the efficient use of assets and profitability rather than the financial leverage. Although COVID-19 has dampened the sales, the company has sufficient funds to fuel its growth in the coming future without taking huge debts.

4. Cash Conversion Cycle: The Cash Conversion Cycle measures the efficiency of cash flow management. The Cash Conversion Days for FY22 stood at 117 days, compared to a low 10-year average of 60 days. This increase is due to the rise in inventory days led by a demand slowdown in the decorative paint segment and unprecedented inflation. The cash conversion cycle of KNPL is high compared to its peer, Asian Paints, because Asian Paints has the network to restock its suppliers quickly, leading to low inventory days and a faster cash conversion cycle.

5. Dividend– The company has paid an interim dividend of 125% on 30-11-2021 and proposed a final dividend of 100%. The total pay-out stands at 225%, i.e., ₹2.25 per share, whereas the dividend for the previous fiscal year was 525% which included a special dividend of 200%. The dividend yield of Nerolac in FY 2022 was 0.56%, whereas that of Asian Paints was 0.71%.

6. Cash and Cash Equivalent (CC&E): KNPL has sufficient current assets to meet its liabilities. The significant increase in CC&E in FY16 was due to the sale of fixed assets and an increase in trade payables. CC&E for FY22 lies at ₹77.04 crores, down from ₹102.94 crores, as the margins deteriorated and the losses from the Sri Lankan subsidiary widened. The company has taken a slew of expansionary measures in the past few years that resulted in significant cash outflows like:

● Acquisition of Perma Constructions and Marpol Pvt Ltd to give a boost to chemical business

● Set up a dedicated manufacturing unit for coil coating

● Started a dedicated manufacturing capability for wood finish

● Took steps to boost its Nepal business. E.g.-The company started a project to upgrade their Birgunj Plant and implemented SAP ERP to make their operational processes more efficient.

Environmental, Social, and Governance

Environmental

Decarbonization

Nerolac is continuously working on increasing energy consumption from renewable sources. The company also undertakes risk assessment as per the Taskforce on Climate-related Financial Disclosures (TCFD) framework and works on reducing Specific Power Consumption (SPC) and Green Belt Development. The company commits to achieving 70% Electricity from Renewable sources by 2030

and Carbon Neutrality.

Resource use

Nerolac is working on reducing its water footprint through initiatives including developing water efficiency and promoting rainwater and recycled water consumption within its operations. The company leverages its R&D strength to create sustainable products and solutions. Improving water availability is another aspect of their initiatives, including watershed development projects, Incremental Specific Water Consumption (SWC), and Specific Hazardous Waste Generation (SHWG) reduction targets. The company aims to achieve 41% of its total energy consumption through

renewable sources by FY 2023.

Social

Nerolac focuses on community development by promoting Equality, Safe and Healthy Working Conditions, Employee Engagement, and a robust Code of Conduct. They have also developed a dedicated Internal Complaints Committee (IC). Concerning the same, the company has committed to achieving zero human rights abuse, zero incident-accident, and fostering a behavioural-based safety culture. The company also promotes diversity inclusivity by maintaining no discrimination based on gender, race, age, religion, and ethnicity.

Governance

The Company’s board consists of 8 directors and complies with SEBI (LODR) Regulations. The Board also consists of one Woman Independent Director. The Company has adopted a Code of Conduct for Board and Senior Management. No shares are pledged by the promoters, and the total promoter

holding is 75%.

The company maintains an Enterprise Risk Management setup to improve governance, including required Board oversight and statutory compliance. The company has committed to zero noncompliances and efforts to reduce enterprise risk. The company has featured in NSE 50 Companies evaluated based on ESG footprint, thus validating their continuous efforts.

Risk Analysis

The Paint Industry functions in a dynamic business environment forcing participants to prioritize Risk Management. Keeping this in mind, KNPL focuses on risk management to guard itself against adversities and derive the maximum benefit from good business periods.

- Cyclicality of the industry – Paint is a cyclical industry, and KNPL’s majority of sales come from the industrial segment. A slowdown in economic growth and other seasonal variations can affect the operations and financials of the Company.

- Commodity Risk – The paint industry uses around 300 raw materials, of which around 150 are Petrobased derivatives. As crude oil prices are volatile depending on macroeconomic factors, the raw material price also fluctuates. However, KNPL does not undertake hedging activities to hedge this risk.

- Financial Risk – Currency fluctuations and market volatility can potentially impact earnings. Therefore, adequate planning and discussions regarding hedging are essential.

- Operational Risk – Risks associated with product delivery, quality, and environmental impact, among other operational risks, are present in this Industry. In response, the company has developed robust mechanisms that ensure operational risks are taken care of while promising innovation.

COVID-19 Impact

Overall, the financial year 2022 was turbulent for the company and the industry at large. The first quarter witnessed muted volumes accompanied by supply chain shocks on the grounds of the Covid pandemic restrictions. The business environment did improve in the second quarter, with demand rising in the decorative paint segment. Semiconductor chip shortage continued to hurt the automotive paint sector. Material costs continued to grow due to increasing crude oil and chemical prices. Though the

business environment was volatile, KNPL continued its expansion across various horizons by introducing new solutions and entering new business segments and markets. In response to the COVID pandemic, the company has raised prices and is expected further to grow prices across segments in the near future. The price increases already made have been successful in offsetting inflation. However, further price increments are necessary for the Industrial segment.

The EndNote

Paint penetration in India is relatively low, but intense competition from new players could make the fight for market share difficult for all players. While inflation will inhibit margins in the near term, rising competitive intensity is expected to weigh on margins and earnings growth in the medium term. KNPL has plans to expand and strengthen its footprint outside India organically and inorganically

Considering these factors, an essential issue arises: will Nerolac be able to maintain its position in the Indian paint industry?

Stock Price History for the past ten years

- The Company announced a stock split on 26 March 2015 in the ratio of 1:10.

- The stock plummeted in FY20 on the grounds of the Covid pandemic.

Disclaimer: The report and information contained herein are strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied, or distributed, in part or whole, to any other person or the media or reproduced in any form, without prior written consent. This report and information herein are solely for informational purposes and may not be used or considered as an offer document or solicitation of an offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting, and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their investment objectives, financial positions, and the needs of a specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, other derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness, or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document are provided solely to enhance the transparency and should not be treated as an endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors, and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any Company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared based on information that is already available in publicly accessible media or developed through an analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed, or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, where such distribution, publication, availability, or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the firm nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

.

Contributor: Team Leveraged Growth

Co-Contributor: Yash Haralalka, Madan Gopal Sharma

Research Desk | Leveraged Growth