Click here to download the report

Campus Activewear: Athleisure Super-Giant in the making?

Overview

Campus Active Ltd. (NSE: CAMPUS) is India’s largest sports and athleisure footwear brand in terms of value and volume in Fiscal 2021 (13.6 million pairs). The company has over 425 distributors in 28 states and 664 cities with a pan-India trade distribution network. The firm had 19,200 stores and 5 production sites in India, with an annual assembly capacity of 28.8 million pairs as of December 31, 2021. Furthermore, it has an extensive online presence in D2C, which complements the trade channel in underpenetrated geographies. Having a 17% market share in branded sports and athleisure footwear, Campus is one of the fastest-growing brands in the space from FY 2019 to FY 2021.

Campus Activewear IPO Makes a Strong Debut on NSE, BSE

Campus Activewear made its stock market debut on May 9, 2022, with its shares listing at ₹360 per share on the NSE, around a 23% premium over its issue price of ₹292. During the trading session, the stock surged to ₹418 despite global issues and a bearish trend in the broader market.

Backstory

Incorporated in 2008 as a lifestyle-oriented sports and athleisure brand, Campus has a comprehensive product assortment for the whole family. The brand provides a variety of styles, pricing ranges, and an appealing product value proposition.

Hari Krishan Agarwal, Chairman, and MD have over 37 years of experience in the Indian footwear industry. He is an ex-director of Action Shoes Private Limited. He always wanted his firm to go public because he regarded the super-niche Sports and Athleisure industry as a big opportunity in India. This specialized trend had already played out 15-20 years ago in the United States and China, and the Agarwal family foresaw it in India.

Nikhil Aggarwal, son of Hari Krishan Agarwal, is the Whole-Time Director and CEO of the company and has14 years of experience in the footwear manufacturing and trading sector. He has completed a Workshop and an Executive Education program at INSEAD, Singapore.

The company has appointed Raman Chawla as CFO, Archana Maini as CS, Piyush Singh as Chief Strategy Officer, Raghu Narayanan as Supply chain & Operations country head, and Uplaksh Tewary as Retail country head. All key managerial personnel possesses multi-year experience in leading MNCs. The company maintains employees’ interest in the company through ESOPs.

Industry Analysis

In congruence with the rise in per capita GDP, brand awareness, and discretionary spending, the Indian footwear market registered a CAGR of 9% in value terms and is expected to grow by 17% CAGR in the coming years.

The share of organized players has grown at a CAGR of 13% in the past five years, which is expected to grow by 22% between 2022-25, supported by heavy marketing and increasing urbanization. Also, the organized sector’s market share will increase from 34% to around 38%. Sports and Athleisure, a 12000 crores market, is the management’s focus. 55% of this market is captured by brands, of which Campus caters to 17-18% market share. There is an underlying threat of competitors entering the niche, but the opportunity to gain market share seems lucrative.

Business Model

The company focuses on creating a niche in the Sports and Athleisure segment, targeting India. The target price range is between ₹500 and ₹3500.

The management is single-category focused, unlike other domestic brands that focus on multiple categories. Inspiration for this move was brands like Nike, which have created wealth by focusing on a single segment. The decadal CAGR of the company is around 27%.

The company’s cash flows are negative as they have recently set up two manufacturing plants for Uppers and Soles. According to the CEO, the industry is very Capex light, as a 100 crore Capex could generate around ₹500-600 crores of sales. The labor-intensive nature of the business commands efficient management of the supply chain.

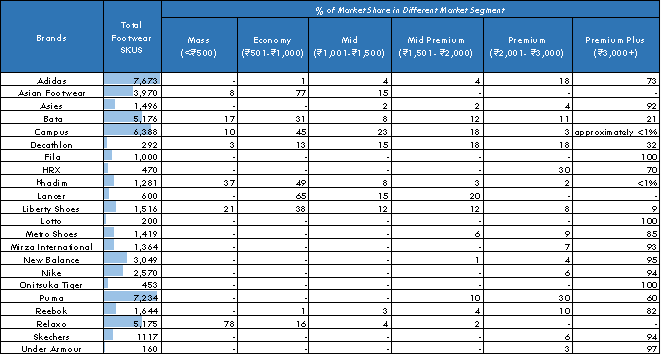

Brand wise segmentation

The company caters to a wide range of price points, including Entry (~38%), Semi-Premium (~21%), and Premium (~41%). Revenue contribution from premium products has increased from 31% in FY 2019 to 41% in the first nine months of FY 2022.

Brand wise Price segmentation compared to peers:

Differentiating Strategies:

1) Focusing on a Single Segment rather than giving attention to multi-segments or multi-brands has worked phenomenally for the company as it has shown a decadal CAGR of 27%.

2) New designs:

The industry is affected by trends, and regularly making new designs is the norm. The company has launched,

2020- 697 new designs, which are 54% of their revenue from the sale of goods.

2021- 583 new designs, which are 65% of their revenue from the sale of goods.

3) Advertising and sales promotion:

Advertisements on traditional networks such as TV, billboards, online ads, social media, etc., are essential to impact consumers’ minds and hold their attention.

The company spent 3.7% and 4.6% of revenue from operations on advertising and sales promotion in 2020 and 2021, respectively.

Moreover, the management claims to have over 2000 active designs at any time of the year, an extensive portfolio in a single segment.

4) Diversified Revenue Share:

The company is well-diversified among different geographies and focuses on underpenetrated markets.

We observe sales are migrating from traditional distribution channels to the online D2Cs segment. It

is profitable for the company as D2Cs have higher EBITDA Margins.

SWOT ANALYSIS

A. Strengths

1) Distributors, COCOS, FOFOS, and Large Format Stores (LFS):

Campus has over 400 distributors as of September 30, 2021.

It has 48 COCOs (Company-owned, company-operated) and 3 FOFOS (Franchise-owned, franchise-operated) by the end of the period on September 30, 2021. Recently, the CEO claimed to reach 60 COCOS and 30 FOFOS)

By the end of FY 2019, the number of COCOs increased from 32 stores to 37 by the end of FY 2020, to 45 stores by the end of FY 2021, increasing further to 48 stores by the end of September 30, 2021.

Campus also operates over 800 counters situated in Large Format Stores (“LFS”), as of September 30, 2021 (“Counters”)

2) Manufacturing Ecosystem:

Through its manufacturing facilities, the company can manufacture 37.5% of its requirement of soles and 8.98% of shoe uppers in-house while it assembles 100% of its products in-house. As such, the company is dependent on the continued operations of these manufacturing facilities for production.

Three of the manufacturing facilities in Baddi Facility (Himachal Pradesh), Dehradun Facility, and Campus AI Baddi (Himachal Pradesh) Facility commenced in FY 2005, 2009, and 2015 respectively are responsible for assembling.

3) Raw Material Procurement:

Approximately 85% of the company’s raw materials are sourced locally in India. The remainder of the raw materials is sourced from China, South Korea, and other South-East Asian countries. The company also supplies all of the raw material requirements of their fabricators. Currently, the company procures raw materials on a purchase order basis at negotiated rates. Details of the raw material supplied and share of raw material cost are as follows in FY 2021 and the six months ended September 30, 2021, are as follows:

B. Weaknesses

1) Leases:

Campus leases the space for all the COCOs as of September 30, 2021.

It spent ₹2.5 crores, ₹3.9 crores, and ₹3.7 crores on rent in FY 2019, 2020, and 2021, constituting 0.43%, 0.53%, and 0.52% of the revenue from operations in the same years.

2) Credit Risks:

The total trade receivables amounted to ₹162 crores, ₹144 crores, and ₹98.2 crores, representing 51.8%, 33.4%, and 25.6% of the company’s total current assets, for FY 2019, 2020, and 2021. Hence, credit risks are associated with the company.

Campus had executed agreements with its distributors, which carry a credit term ranging from 30 to 60 days. The company stated that if it encounters significant delays or defaults in payment by the customers or is otherwise unable to recover its trade receivables, cash flows from operations may be inadequate to meet the working capital requirements.

For FY 2019, 2020, and 2021, allowance for expected credit loss and trade receivables written off amounted to ₹4.8 crores, ₹7.4 crores, and ₹6.4 crores, representing 0.8%, 1%, 0.9% of revenue from operations, respectively.

3) Seasonality:

The average selling price of Campus experiences moderate fluctuations during the year. There is quarter-on-quarter volatility as seasonality comes into effect. In the summer and rainy seasons, the customers typically purchase more open footwear than closed footwear. According to the Technopak Report, open footwear primarily has a lower realization than closed footwear, which has a higher realization. Additionally, the company typically sees an increase in the business in the third and fourth quarters due to the festive period.

4) Labour Contracts:

Campus relies heavily on contract labor for their manufacturing process. They engage with independent contractors through whom they hire contract labor for their manufacturing facilities and warehouses. They typically utilize three to four labor sub-contractors for each facility. The company explained that an inability of these independent contractors to procure laborers for facilities or any other shortage in contract laborers might require it to employ laborers directly at its facilities, resulting in higher costs and reduced margins.

5) Attrition Rates:

The turnover rate of the retail industry is high. The company’s attrition rates are as follows:

2019- 16.8%

2020- 10.2%

2021- 16.9%

6) Returns from our Online Space (E-tailing):

Almost all marketplaces offer a standard feature of returns and cancellations across the footwear category.

The returns from marketplaces on account of such customer cancellations and returns are typically 25% to 30% of all sales made through the online channels in a fiscal year.

The sale of goods generated from online sales was

2020- ₹57.2 crores, which accounted for 7.8% of the sale of goods.

2021- ₹150 crores, which accounted for 21.2% of the sale of goods. Online sales are a growing component of the sale of goods and are the fastest-growing sales channel for athleisure products in India. These online sales were undertaken through third-party market places

C. Opportunities

1) Country-wise GDP:

As of now, India is at 2.651 trillion dollar GDP, the 5th largest economy globally.

Moreover, it took India over 60 years to reach its 1st trillion and just five years to double its economy to more than 2 trillion dollars which would double again by 2025 if it grows at a CAGR of 10.1%.

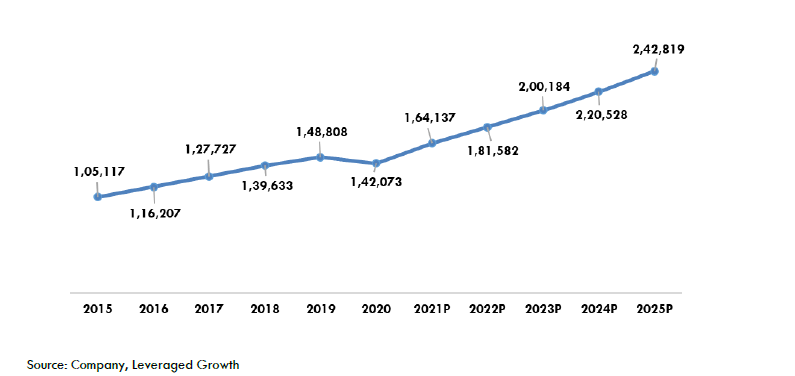

2) India’s GDP Per Capital:

India’s per capita income has been showing an increasing trend since 2012, increasing at a healthy CAGR of around 10%. In FY 2019, the per capita income reached ₹1,48,808, which decreased to ₹1,42,073 in CY 2020 due to Covid. However, it is expected to bounce back and continue its growth journey at a CAGR of 10.3% between FY 2021 and FY 2025

3) Young Population:

The median age of India’s population is 28.1 years which is way younger than the peer countries and is expected to remain under 30 years until 2030.

4) Increasing Urbanization:

Currently, only 34.5% of India’s population is classified as urban contributing 63% of India’s GDP. It is estimated that 37% (541 million) of India’s population will be living in urban centers by FY 2025. The urban population is anticipated to contribute 65% of India’s GDP by FY 2025 and 70% by FY 2030. This is expected to continue with ~50% of India’s population living in urban centers by 2050 and contributing ~80% of India’s GDP.

D. Threats

1) Stagnant Sales due to future covid waves- Although the company has rebounded quickly after its manufacturing resumed, there’s still fear of future covid waves. As the company is in a labor-intensive industry and is highly reliant on efficient supply chain management, any surge in cases among its employees or partial lockdowns can hurt its top line.

2) Increased competition in this segment- As a thumb rule, competition can sniff the opportunity and enter the industry wherever there are supernormal profits. If it’s a massive player with ample cash to burn, it can be a disrupting factor for Campus.

3) Economic slowdown– As the retail segment is highly dependent on the county’s economic growth, any counter growth cycles can hamper the company’s revenues.

Michael Porter’s 5 force analysis

A. Barriers to Entry:

- Distribution or Supply chain efficiency- Any FMCG or Retail business depends on its distribution channels and efficiency. The CEO has claimed to crack the Supply Chain code.

- High Capex for economies of scale- Without economies of scale, the cost of manufacturing shoes would exceed the competitive selling price. Creating economies of scale would require a considerable CAPEX which is not feasible for several companies.

B. Bargaining Power of Suppliers:

- Increasing vertical integration- The company produces ~ 85% of its raw materials in-house and assembles them entirely in its two facilities.

- Diversified Portfolio of suppliers- Having 10-40 active suppliers spread across several south Asian countries protects them against shortages or abrupt price increases.

C. Bargaining Power of Buyers

- A Large number of designs- There are more than 2000 designs available across various price points for the end customers. It’s a large number for the customers to choose from a single segment brand.

- Inflation protection- The average selling price of Campus has grown 7-8% in the past three years, and it hasn’t just protected the margins, but there is 25-30 bps of margin expansion year on year. The nine-month sales ending FY 2022 do not indicate the company is losing customers to competitors.

D. Rivalry among competitors

- The sports and athleisure market is around 12000 crores which is ~ 55% dominated by brands, and of that, 17-18% is of Campus. There is a 45% unorganized market, which can be a competition as they provide retailers with higher margins than the organized ones. Also, other domestic or MNCs can enter this niche segment and take away market share.

E. Threat of Substitutes:

- Campus shoes and sandals are comfortable, making the switching cost a significant factor in decision-making. The Sparx brand of Relaxo can be a good example; once people start wearing it, they buy a different design from the same brand every year when they change their footwear. Campus, targeting a little premium segment than Sparx, offers more comfort to the customers. Once the customers get attuned to it, they will ask for the same brand every year with a different design. So, unless the company or quality changes massively, the threat of substitutes will be relatively less.

Branding & Other Initiatives

The perception of a brand influences a customer’s purchasing decision. To stay ahead of the competition and cement its position in the market, Campus focuses on brand awareness and acceptance and the culture, lifestyle, and visuals associated with its brand. To effectively promote its brand, the company emphasizes various promotional and marketing activities to raise brand recognition and brand visibility.

Also, the company relies on social media influencers for brand growth and advertising. These influencers’ reputations and actions have a direct impact on their brand.

These types of quizzes and activities on Social Media are a very effective way to engage with the audience and also a way to check their brand awareness.

The “Ab Waqt Hai Hamara” campaign, where several athletes practice their respective sports wearing Campus shoes, gives an inspirational factor or value.

Financial Analysis

The company registered a revenue of ₹8439.5 million in the first nine months of FY 2022, surpassing the revenue of FY 2021(₹7150.8 million). The EBITDA margin declined ~13% from FY 2020 to FY 2021.

- Gross Margins are stable and increasing at 46%, 48.1%, 47.4%, and 50.6% for the respective years.

- EBITDA margins are stable and increasing at 16.8%, 18.7%, 16.3%, and 19.4% for the respective years.

- PAT Margin touched a substantial low of 3.8% in FY 21, down by 57% from the past year due to one-time hit of regular change as the Government of India disallowed any tax break on Goodwill. But it has crossed 10.1% in 9 months ending FY22.

- The inventory days have increased from 72.5 days to 103.9 days in FY21 due to covid.

- The Debtor days have reduced from 99.4 days to 50.4 days in FY21.

- The Creditor days have increased from 49.5 days to 87.7 days in FY21.

- The Debt to Equity ratio of the company has reduced from 0.9 to 0.4, showing a healthy and less risky balance sheet

Risk Analysis

1) Increased domination by MNCs: India being a free economy, there can be foreign established companies scaling immensely right now in India. If they enter this segment, it can threaten the company’s market share.

2) Change in Consumer preferences: Customers’ preferences fluctuate as fashion trends and styles change, necessitating the company constantly innovate and produce new designs. The company witnessed a trend of flip-flops that are now slowly declining. The designs and styles the company introduces should be relevant, or else the consumers can shift to some other brand.

3) Brand Irrelevance: India is a very competitive market. To hold the customer’s attention is the most important thing right now. Brands spend enormous amounts of money in advertising to remember the brand in the consumer’s mind. Any decline in the promotions of the brand can hurt significantly. In addition, negative publicity or disputes regarding our brand, products, company, or management could materially and adversely affect public perception of the brand.

COVID 19 Impact

As opposed to massive de-growth in the industry, the company’s top line fell by a mere 2.9% with only seven months of operations in the FY 2021, which is remarkably resilient. Sales have already surpassed 1100 crores in the nine months ended FY 2022, indicating that demand has returned. The ROCE has returned to 31-32% in the last twelve months. The 57% drop in PAT in 2021 had nothing to do with Covid. It was a one-time impact due to a regulation shift in which the Indian government prohibited any tax credit on goodwill.

Corporate Governance

The “Backstory” section introduces promoter groups and their history.

The Articles of Association require that the board consist of not less than three Directors and not more than 15 Directors. As per the Red Herring Prospectus, the company had 8 Directors, of whom 4 were Independent Directors, including 1 woman Director. The company is in compliance with the corporate governance norms prescribed under the SEBI Listing Regulations and the Companies Act, 2013. None of the Non-Independent Non-Executive Directors are entitled to receive any sitting fees or commission. Further, the Independent Directors may be reimbursed for expenses permitted under the Companies Act and the SEBI Listing Regulations

ENDNOTE

Some of the biggest wealth creator companies in India have a focused strategy on a specific niche rather than putting their legs in 50 different things. We find Campus Activewear in the same category. Founder Hari Krishan Agarwal has four decades of experience in the footwear industry in India. His son, CEO Nikhil Agarwal, has repeatedly conveyed to stay this way. He assures there will be no unnecessary ventures or, in his words, “We live and breathe Campus every day.” If the company keeps this pace and captures more market share while not compromising on the quality and comfort they are known for, we feel this can be an interesting story to follow.

Disclaimer: The report and information contained herein are strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied, or distributed, in part or whole, to any other person or the media or reproduced in any form, without prior written consent. This report and information herein are solely for informational purposes and may not be used or considered as an offer document or solicitation of an offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting, and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their investment objectives, financial positions, and the needs of a specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, other derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness, or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document are provided solely to enhance the transparency and should not be treated as an endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors, and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any Company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared based on information that is already available in publicly accessible media or developed through an analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed, or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, where such distribution, publication, availability, or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to a certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the firm nor its directors, employees, agents, or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

.

Contributor: Team Leveraged Growth

Co-Contributor: Dhruv Bhanushali, Madan Gopal Sharma, Shivangi Deora

Research Desk | Leveraged Growth