Click here to download the full Report

Executive Summary: The scale and seriousness of quarantines introduced during March 2020 effectively brought economic activity to a global standstill. Italy seems ready to enter into a painful cycle of excruciating debt and aging population, France is marginally better placed. Germany has twin problems of stagnating exports and deflation, it seemingly also has the resources to fight them for now. UK seems lost between dealing with Brexit or the health crisis looming at its doorstep. USA, after embroiling itself in a historic trade war, now finds itself in a different war altogether – one that it will need ‘unlimited’ resources to fight and win.

Stating the obvious, there has never been a bear market quite like this. What’s incredibly intriguing are the occurrences across asset classes, considered unprecedented even for crises. The US bond market warrants deep analysis given the unnatural and abysmal performance of Investment Grade Bond ETFs to that of Junk Bond ETFs. Moreover, US Treasury Bond ETFs were in chaos as flight to safety clashed with illiquidity causing severe market imbalance, dwindling investor confidence. Globally, currency markets faced a similar chaotic brunt as foreign investor withdrawals put pressure on respective central bank’s dollar reserves; who to stabilize their local currency in turn amplified the global selling spree by liquidating their dollar asset holdings. Yen’s status as the crisis currency is being put to the test, with Japanese policy makers enhancing downward pressure on Yen by successfully encouraging foreign asset buying for protection during the crisis. Commodities are a strange asset class too. While gold is following a similar trajectory to the previous financial crisis of 2008-10, the global demand for the commodity has fallen over the years dwindling investor hopes of bumper crisis returns. Similar fundamentals follow silver that is maintaining twice the positive correlation to the S&P500 than it did through 2008-10. The oil market is facing its own crisis since the OPEC+ ended; Saudi Arabia has been flooding the market in a domination war, threatening near or complete bankruptcy of other suppliers.

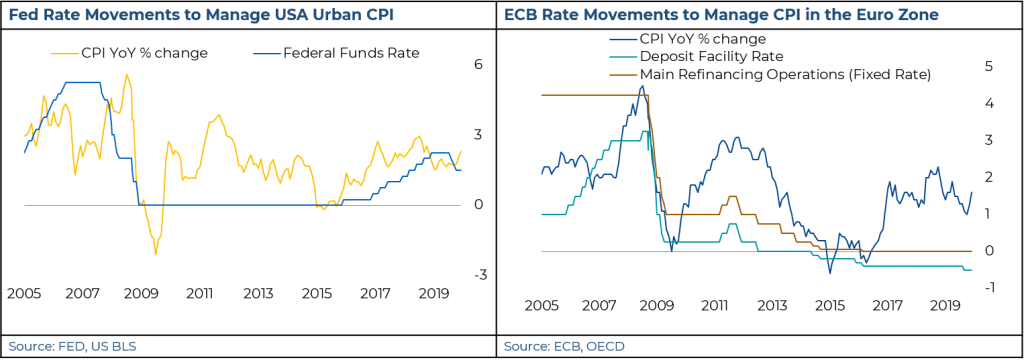

Global policy responses have come to end chaotic market behavior by providing liquidity and tackling recessionary fears while also raising cautionary eyebrows along the way. On one hand, the high economic output losses from global efforts to contain the COVID-19 pandemic are unprecedented. On the other hand, it is unclear if the opposite scenario would be less costly – an uncontrolled pandemic such as the 1918 Great Influenza resulted in substantial and persistent damages to human life. Governments across the world are thus caught in a Catch-22, and policy decisions taken today will have long lasting and deep effects for generations to come. Take for example FED’s ‘whatever-it-takes’ policy to provide endless liquidity and to inject trillions of dollars into the financial system; or ECB’s decision to boost its asset purchase programs to provide temporary relief to the hard hit Euro Zone. Both these central banks have spent a decade in fighting crises and reviving their respective economies, the jury is still out on their success; and are only continuing their quantitative easing programs in hopes to one day normalize their balance sheets having no chartered route to do so. The last time Fed announced a withdrawal of its QE plans, 2013, it spurred massive asset selling across developing economies, especially the Fragile Five which then included India. The effects of developed economy central bank policies on developing economies at half the balance sheet size than that of today should spark concern among any investor. India, fortunately, has since evolved to a favored investment decision given the rising foreign assets in RBI’s balance sheet and declining government deficit, further encouraged by positive policies from both the central bank and GoI.

The flow of events in India have a different story to tell altogether. Economic growth in the country was already fraught with challenges as the entire financial system was reeling from the multiple shocks in terms of GST implementation, NPA crisis, NBFC defaults and other reformative measures undertaken by the government. In this backdrop, an unprecedented hit on cash flows due to lock-downs might be the trigger to push the corporate sector into the default zone. The government is yet to announce significant relief measures as it faces tough choices regarding its finances. The reforms in the first place were aimed at helping India climb the ranks as the favored destination to manufacture and export. However, we seem to be missing that bus as exporters are largely left to fend for themselves amidst the crisis.

– By Team Leveraged Growth