Click here to download the report

One of the Most Underrated Players in the Chemical Industry

Camlin Fine Sciences Limited (“the Company” or “CFS”) operates within the consumer durables and chemicals sector and has established a global foothold, with operations in several countries, such as India, Brazil, China, Mexico, United States as well as Europe. Over three decades, since the Company’s inception to the present, it has been able to cement its position as one of the leading manufacturers of traditional antioxidants such as Tertiary butylhydroquinone (TBHQ) & Butylated hydroxyanisole (BHA) , and the world’s 3rd largest producer of Vanillin (a key aroma ingredient ). Over the past few years, the Company has seen tremendous growth, from globalizing its operations and reach, to significant developments in its vertically integrated supply chains.

The Company primarily indulges in four key business verticals:

- Shelf Life Solutions

- Aroma Ingredients

- Health and Wellness

- Performance Chemicals

CFS products are used in a various array of sectors, some of which are listed below:

- Food, feed, animal and pet nutrition

- Flavors & Fragrance

- Pharmaceuticals

- Agro Chemicals

- Petrochemicals

- Dyes and Pigments

- Polymers

- Bio Diesel

Major Clients of CFS

The Journey

D.P. Dandekar and G.P. Dandekar, proprietors of Dandekar & Co., had just started selling inks and ink powders in the early days of 1931. Having left his government job in search of a start-up, D.P. Dandekar realized that stationery products were mostly imported from countries such as Germany and the UK. The Dandekar brothers, thus, decided to open up a business in the stationery line. Desiring to expand into the fountain pens business, the two proprietors looked for an easy to pronounce and familiar brand name, and thus, the Camel brand came to be. The idea was that once you fill a pen with ink, it can run for miles, somewhat like a camel. The Company began its operations in 1931 in Mumbai, India, as a supplier of ink powders and tablets. Combining the words in its previous name, ‘Camel Ink’, the business was soon renamed to ‘Camlin’. By 1947, Camlin was a household name, offering a variety of art material and stationery products, including chalks, rubber stamps, pencils, and geometry boxes and various other items. Capitalizing on their tremendous growth and popularity, in 1984, the Company entered the chemical sector with an ultramodern plant at Tarapur, India, to produce antioxidants for a global market. In 2006, the chemical and pharmaceutical division was demerged from the parent Company, and an entirely new identity, Camlin Fine Sciences Limited was formed. Within a year, in 2007, the stock was listed on the BSE, and the Company has upheld its dedication to technology and constant innovation under the guidance of Mr. Dilip D. Dandekar, who was appointed as the Chairman and Executive Director of Kokuyo Camlin Ltd. in 2006.

Indian Chemical Industry

- As per the statement published by the Federation of Indian Chambers of Commerce & Industry (FICCI) , the minister of Chemicals and Fertilisers D.V. Sadananda Gowda claims that the Indian chemicals and petrochemicals industry is estimated to reach a total valuation of $304 bn by 2025 . This will mostly be driven by the essential nature of the commodity, as well as India’s constant developments and investments into holistic growth. The Country is an emerging economy and has a large potential for sustainable growth in the coming years. The Chemical Industry currently employs more than 2 million people in the Country, thus forming an integral part of the Country’s large workforce.

- According to the Mckinsey & Company Report, for more than a decade, from 2006 to 2019, the CAGR of TRS (Total Returns to Shareholders) for Indian chemical industries was 15%. The figure is much higher than the global chemical-industry returns that has a CAGR of 8%. During 2016-2019, though the Indian economy was in the doldrums, the Indian Chemical Industry registered an impressive CAGR of 17%.

- The chemical industry also secures a valuable position when it comes to India’s overall trade flow. According to data provided by the Department of Chemicals and Petrochemicals, India ranks 17th in the world in terms of the export of chemicals and ranks 7th in the world for imports of chemicals .

- The Country is the 6th largest producer of chemicals globally and the third-largest producer in Asia in terms of output. According to the India Brand Equity Foundation (IBEF), the Country also ranks 3rd globally in the agrochemical output.

- Domestic consumption is expected to drive the demand as it is estimated to be around $111 bn by 2023.

- The recognition the chemical industry receives from the government has also been a key driver of growth in the sector. 100% Foreign Direct Investment (FDI) is permissible within the chemicals sector in India.

Business Model

Camlin Fine Sciences has developed an all-inclusive vertically integrated business model for over thirty years, which enables it to manufacture raw materials within the purview of the Company itself. The Company has curated a well-diversified range of products, which caters specifically to customer requirements, and can be mainly categorized into four verticals.

- Shelf-Life Solutions are products that help increase the durability of the product, as well as preserve color, freshness, safety, and the quality of the product. These products include antioxidants, blends, and other food and feed additives. This product makes up for more than half of the revenue share percentage, and the Company is one of the leading global manufacturers of antioxidants.

- Performance Chemicals are unique and customer requirements are based on chemicals that are developed and sold based on their performance for unique applications. Such chemicals lead the way for innovative solutions to customer requirements.

- Aroma ingredients are used in food, flavors and fragrance industries, and the Company is the world’s third-largest producer of a key aroma ingredient, Vanillin. CFS produces the aroma ingredients using a completely traceable vertically integrated production. The finished products are made using environmentally friendly methods, from Catechol. All key ingredients are made in-house, and the Company has gained traction as a quality global Vanillin supplier.

- Health & Wellness business vertical was launched in FY20 which offers nutraceutical products from fermentation and green extraction sources. The division is formed to cater to the needs of baby boomers and millennials.

The Company has been able to incorporate 5 manufacturing facilities, 2 R&D labs, and 5 Application Labs under its purview. Due to its worldwide presence and strategic partnerships, CFS can market its products globally, especially in consumer hotspots such as Europe, Asia Pacific, South, Central, and North America, as well as the Middle East . Strategic partnerships with specific companies in different geographies within the same industry enables the Company to capitalize on distribution networks and increase Company presence across different geographies.

Impact of the Unprecedented COVID-19

COVID-19 has disrupted financial markets, raised uncertainty to unseen levels, and has tested the financial resilience of top companies around the world. The virus has caused disruptions in global supply chains, along with lockdowns in countries around the world. CFS’s international exposure has been particularly detrimental in such an unprecedented scenario. The Company faces shrinking demand and consumption levels as most industries had to be brought to an immediate halt due to government-imposed lockdowns.

However, there exists a silver lining. Given the essential nature of the chemical sector, operations had been resumed shortly after the initial quarantine period. The current financial performance of companies will be impacted due to the virus. However, with strong fundamentals, in the long run, resilient companies can see this out.

Differentiating Strategies

- Vertical Integration

Over 30 years, CFS has developed an extensive vertically integrated supply chain unlike that of its competitors. The Company’s plant in Ravenna, Italy, produces the basic raw materials like hydroquinone and Catechol for many of its further production uses. The vertical integration ability then transforms the raw materials into products that cater to a large variety of sectors, such as food, fragrance, pet food, petrochemicals, pharmaceuticals, and agrochemicals, etc. It ensures a stable line of products, maintaining quality and transparency. Furthermore, it allows the Company to ensure its products reach the markets at competitive prices and are traceable with ease.

- Marked International Presence

CFS has a well linked and comprehensive international network that enables the Company to make its impact on many countries around the world. The Company currently serves in more than 80 countries with over 100 products. The Company began its operations in India in 1984, and in the past few years, has become one of the leading manufacturers in antioxidants and aroma ingredients around the world. With R&D labs in India and Italy and several Application Labs in countries around the world, the Company remains confident of making a global impact and impacting lives around the world.

- Research and Development Initiatives

The Company remains at the forefront of technological progress because of its investments in R&D labs. CFS has two states of the art ultra-modern R&D Centres, located in Tarapur, India, and Ravenna, Italy. The 8600 square foot Indian Centre consists of a synthetic and process development lab and an independent pilot plant that supports scale-up activities and helps process engineering studies. The R&D facilities in Europe are a mix of in-house and collaborated efforts with external research units and universities. The Ravenna facility focuses on improving existing technology as well as the development of new products and processes. These initiatives allow the Company to stay ahead of technological developments in the industry and take advantage of opportunities as and when they arise, giving the Company competitive advantages.

SWOT Analysis

Strengths

- Cost Advantage – The Company owns manufacturing facilities that are involved in producing key raw materials i.e., Hydroquinone and Catechol. The Company’s well backwardly integrated value chain gives them an added advantage in terms of procuring raw materials at a lower rate than its peers and helps in increasing their profitability margins. As per the Company, its new manufacturing plant at Dahej, Gujrat will make CFS the 2nd largest producer of Hydroquinone and Catechol in the world.

- Global Presence – The Company has diversified its revenue stream across geographies as it serves more than 100 products in more than 80 countries.

Weaknesses

- Significant Rising Debt – The Company invests heavily in Research and Development, and also funds its capital requirements to stay ahead of the competition. These advantages, however, come at the cost of rising debt. Over a decade, the Company has mounted a large amount of debt, and the benefits from these investments have not yet given proportionate returns to the Company. The nature of these investments has been predominantly long-term; however, a large portion of the debt is short-term in nature. This spread may affect the financials of the Company, as well as the rising interest costs accompanied by rising debt. Since FY18, the Company has also seen a large spike in its long-term borrowings as the number has more than tripled as of FY20.

- Dependence on Customers

Being a supplier firm, which functions in B2B space, the Company had a fallout with its customers in FY17 due to which there was a large drop in its revenue. The Company has also got low bargaining power, which is reflected in its low margins as the Company is unable to pass on the cost to its customers. Since then, Company has taken steps to expand in other geographies to reduce its dependence on few customers.

Opportunities

- Growing Demand – In emerging markets, such as India and Mexico, the demand for chemicals continue to grow as a result of their large working-age population. The chemical industries in such markets are perceived as drivers enabling elongated product life cycles. The rush to commoditize such products has led to improved innovation avenues as well as accelerated globalization.

- Blends – The demand for blends has increased during the lockdown. Since the Company has sufficient capacity to produce 50% or more, there is an opportunity for the Company to tap into this growth.

- Increase in Foreign Institutional Investor Shareholding – Foreign Institutional Investors (FIIs) have increased their shareholding of the stock since FY19. In December of 2019, FIIs held almost 0.9% in the Company, which increased to 1.2% in March in 2020. This indicates growing foreign confidence in the stock and its fundamentals.

Threats

- Significant International Exposure – The Company, with operations in more than 80 countries, is significantly exposed to changes in foreign trade sanctions and government policies. Changes in policies in different countries can affect the operations of the entire Company and may even raise costs, thereby affecting profitability. Since the Company is vertically integrated, a negative change in countries that manufacture raw materials used for further processes can entail high overall costs.

Michael Porter’s 5 Forces Analysis

Barriers to Entry

- Large Capital Investment Requirements – Entering the chemical industry has large capital requirements for the setting up of modern and efficient plants. Investment is also required when setting up R&D labs to capitalize on competitive advantages constantly arising within the chemical industry.

- Complexity – The chemical industry requires a certain level of sectoral knowledge. When entering the industry, new firms have to incorporate individuals who are experienced and possess sector-specific knowledge to succeed in the market.

- Regulatory Barriers – Companies operating in the chemical sector, especially pertaining to the food and nutrition industry, need regulatory approvals, which can be extremely difficult to obtain. The process can be extremely time-consuming and hold a certain level of uncertainty, which can lead to further time delays.

Bargaining Power of Buyers

- Buyers had high bargaining power initially which could be observed from declining margins and a fall out with customers in FY17. Although, over past few years, successful implementation of strategies by CFS like geographic diversification which has considerably reduced the bargaining power of buyers to medium.

Bargaining Power of Suppliers

- The chemical industry is notorious for changes in the prices of raw chemicals that are used in further production processes. CFS has partially reduced its exposure in such a circumstance by vertically integrating its production processes. The Company produces most of its raw material in plants owned by them.

- CFS has well-established supply chains, and switching suppliers could do more harm to the suppliers than the Company. Keeping this in mind, suppliers have very little bargaining power as CFS has impressive supply chains that enable the Company to keep a hold of prices. To gain a cost advantage, CFS has to maintain its efficient supply chains and not be exposed to supplier demands .

Rivalry among Competitors

- The chemical industry is highly competitive as the companies in the writing industry are ‘price takers’.

Threat of Substitutes

- Chemicals are a highly customizable product. It is often seen that the companies experiment with their products in order to improve their characteristics or to come up with a brand-new product that can serve different clients as well as end-customers’ requirements. Hence, the threat to substitutes remains high.

Branding and Other Initiatives

- The Company has had a competitive advantage since it began its operations in 1984, which was the household goodwill that Camlin Ltd. had built as a quality supplier of stationery, ink powders, and tablets. The name Camlin Ltd. was well versed and known name throughout the Country, and this helped act as a boost for the chemical venture partake of CFS.

- Company participated in past in international exhibitions like Food Ingredients Europe, Gulfood manufacturing (Dubai), 12º Simpósio Brasil Sul de Suinocultura (Brazil), etc to exhibit their products.

Financial Analysis

- Segmental Analysis

- The Shelf-life solutions portfolio majorly consists of antioxidants and additives. Blends (antioxidants and additives) have grown at 24.89% over last year (FY19) whereas straight additives registered a growth of 7.20%. Overall, it’s a high growth segment.

- The Performance chemical segment contributed Rs.246.85 crore in FY20 to the Company. The commercial production of Dahej plant will further increase the revenue from the segment.

- Turnover from Aroma chemicals was Rs.201.55 crore in FY20. The Company has proposed for construction of a plant with a capacity of 1200 Metric Tonnes for producing Ethyl Vanillin in Dahej with a target to start production from it in 2022.

- Health and Wellness is a new division, launched in FY20, which uses third party manufacturing for green extraction products.

- Rising Revenue

Over the past ten years, the Company has seen increasing revenues YoY. The CAGR of net sales over a decade from FY10 to FY20 stood at 16.7%. The trend line indicates a continual of the same in the near future. Rising revenue is helping the Company form strategic relationships with more clients across the globe and serve more customers. The Company saw a sharp dip in its revenue in FY17 due to fallout with its customers as the Company had changed its business strategy. The Company regained its trend since FY18 and is on track for higher overall revenue in the coming years. The net sales figure for FY20 stood at Rs 579.78 crores, up 0.0 6% from the last financial year.

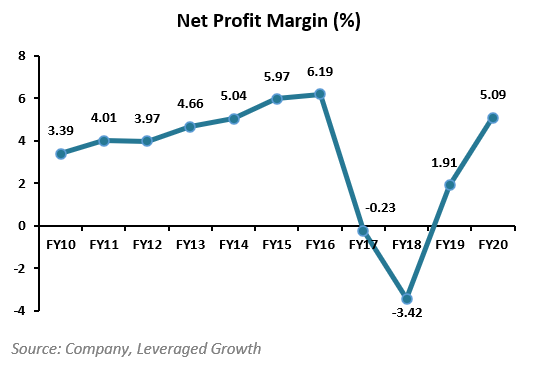

- Profitability on the Rise

In FY20, the Company posted its highest ever net profit number, standing at a whopping Rs.30.72 crores . Further emphasis can be shed on this quantitative when we take into consideration that the Company had suffered a detrimental net loss of Rs.14.18 crores just a few years ago in FY18. The Company’s heavy investments in capital expenditures and a diligent attempt to remain at the peak of technological progress have enabled it to reap the benefits of costly seeds sown in the past. These benefits will continue to compound in the near future, providing the Company with a strong base to work with, along with added efficiency and cost-effectiveness. With improving profits, the Company can repay significant debt and erode the possibility of interest costs impacting profitability.

- Improving RoE and RoCE

The Company has seen rising RoE after registering losses in two consecutive periods i.e., in FY17 and FY18 as the revenues dipped due to fallout with customers. RoE has turned positive after FY19. This happened as the Company diversified its revenue stream by entering into new geographies and launching different products . The Company’s heavy capital expenditures have also started bearing fruit as their RoCE has risen significantly and consistently for the past three years. These are good positive indications regarding additional future cash flows accruing from capital expenditures done in the past.

- High Debt to Equity Ratio

The Company’s debt to equity ratio is high when compared to industry peers such as Fairchem Speciality Limited (HKFINL). The high level of debt is a result of the Company’s constant expenditure on R&D to stay ahead of new market innovations. Nonetheless, the Company boasts an impressive interest coverage ratio, which stands at 1.6 for FY20, more than double of that of FY19 at 0.7. This ensures that interest payments do not corrode profitability and the increased debt can be repaid over time.

Risk Analysis

- Global Economic Slowdown

With global economies completely shutting down to tackle the onset of the deadly virus Covid-19, one can expect the future global economic outlook to be very bleak. CFS is particularly exposed to this issue, as its raw material producing plant is located in Ravenna, Italy which was one of the most affected countries in Europe due to the pandemic. The economic stagnation due to resurgence of virus will also cause a loss in demand in the Company’s products as it resulted in subdued demand during initial outbreak. However, being essential, the impact will be very restricted.

- Exposure to Monetary Policy Changes

The Company has a significant amount of debt, and the issue lies with the exposure to changing market interest rates. The Company’s borrowings are at floating rates and changes in market rates will cause fluctuations in future cash flows. Coupled with rising debt over the past few years, it can begin to take a severe toll on the Company’s profitability.

- Capex with Inadequate Returns

The Company has streamlined a large cash flow towards capital expenditures, and these investments may not turn out to be as beneficial as expected. Advanced technology can quickly become non-existent as more and more companies fight for a larger share in the market. Thus, the Company cannot depend highly on its capital investments, even with significant expenditures in the segment.

Corporate Governance

- The Company has strong ethical business values and aims to maximize its value to all stakeholders. Since its inception, the Company has upheld its culture of transparency, accountability, and integrity.

- The Company’s board consists of 11 directors out of which 2 are Executive directors and 9 non-executive directors. There are 6 independent directors, including 2 women directors. The composition of the Board is in line with the requirements of Regulation 17 of the Securities and Exchange Board of India (LODR).

- The Company has an experienced individual, Mr. Dilip D Dandekar as their Chairman, who has been with the firm since 2006.

- During the year, the Company held 4 board meetings with an average attendance of 10 members.

- Mr. Dilip D Dandekar (Managing Director of the Company) is the paternal uncle of Mr Ashish S Dandekar as well as Ms Anagha Dandekar . Also, Ms Anagha Dandekar and Mr Ashish Dandekar are siblings. None of the other members of the Board of Directors are related to each other.

- Promoter’s total holding remains constant at 22.74%, out of which 10.88% of the shares are being pledged.

The End-Note

- The Company boasts a strong strategic mindset, with a no-compromise policy on holistic and ethical values. CFS’s global presence allows the Company to offset potential losses in disturbed geographical locations, and their extensively developed vertically integrated supply chains helps to ensure that the Company remains competitive and cost-effective.

- The Company’s investments into R&D bear consistent fruit especially when one takes into consideration the nature of the industry they work in, highly customizable, and essential.

- Growing demand, although marginally impacted by COVID-19 lockdowns, and effective management with a diversified Board of Directors will ensure that the Company can continue its successful venture and become a global leader of a wide array of products within the chemical industry.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Vikas Tiwari

Research Desk | Leveraged Growth