Click here to download the report

A Market Disruptor in the Indian Innerwear Industry

Lux Industries Ltd. (‘the Company’ or ‘LUXIND’) is one of the leading companies in the Indian Innerwear Industry involved in the manufacturing of both men and women’s hosiery products with a dominant share in the domestic market and a growing export presence. The Company provides its customers a diversified product portfolio of more than 100 products spread under 15 brands for men, women, and children ensuring relevance across ages, geographies, genders, and seasons. A testimony to the consumer’s preferences, Lux provides more than 5000 SKUs (Stock Keeping Units) across a varied range and sells 2000 pieces every minute to its customers. It is India’s 1st ranked Company in terms of volume and is also the innerwear export leader in our Country.

How did Lux Industries Emerge as a Domestic Leader?

Lux was founded in the year 1957 by Mr. Girdhari Lal Todi by establishing the Biswanath Hosiery Mills to make innerwear comfort a reality for Indians. The Company was managed by the second generation of entrepreneurs who laid down a vision of being recognized as the best Indian Hosiery Company globally, by ensuring superior customer satisfaction, developing top-notch products by delivering innovation, and adhering to the highest ethical standards in its business dealings. Since then, the Company has embarked upon significant milestones. In 1993, Lux began to export its products to the Middle East, Africa, and Europe. It also launched its IPO in the year 2003 and got its shares listed on the Calcutta and Ahmedabad Stock Exchanges. The shares were massively oversubscribed by the public . The undergarments

manufacturer offered 2 million shares of Rs.10 each at a premium of Rs. 40. The Company’s shares got listed on NSE on Dec 1, 2015, and on BSE on Jan 5, 2016. Lux has been one of the most aggressive brand builders in India’s Hosiery Sector and has always invested a significant proportion of its revenues on branding .

Lux has based its business model on the principles of

- Rich Experience

- Competitiveness

- Diversified Product Bouquet

- Extensive Scale

- Robust Balance Sheet

About the Indian Innerwear Industry

- From a basic requirement of a commodity product to a fashion product with an emphasis on comfort and styling, the innerwear industry has broadened its horizons over time.

- Earlier, the innerwear industry was a fragmented space and was dominated by local and unorganized players. The entire industry was highly price-sensitive and people exercised caution in spending on innerwear. However, with rising incomes, higher discretionary spending, and growing fashion consciousness, the market witnessed a change in the trend with the introduction of organized and branded players in the industry .

- The current size of the innerwear industry of India is Rs.27,931 crore (which accounts for 10% of the total apparel market) and is expected to grow with a CAGR of 10% to Rs.74,258 crore by 2027 .

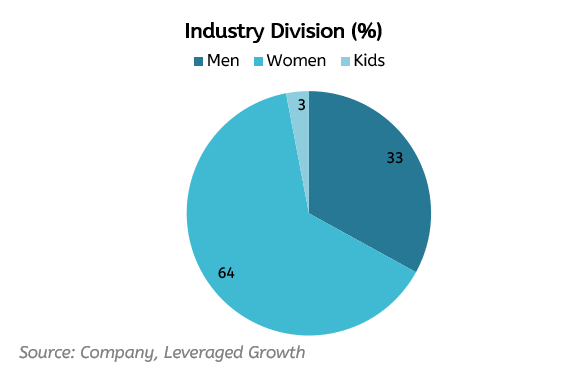

- The men’s innerwear market is expected to grow with a CAGR of 7% whereas the women’s innerwear market is expected to grow with a CAGR of 12%.

- The increase in per capita income implies a rise in the purchasing power of the people . With massive economic growth, rising disposable incomes, and higher discretionary spending, there has been an emergence of a middle class that has become more brand conscious and is ready to experiment with fashion and style. Consequently, the per capita expenditure on innerwear is expected to double to Rs.300.

- There has been a recent rise of occasion-specific products in the industry for different purposes such as sports, fashion, comfort, casual, etc. Moreover, there has also been a recent uptake of the online retail channels which has led to an increase in sales by targeting fashionable youth without access to retail outlets.

Business Model

The key dimensions of Lux Industries are:

- Product: It deals in the hosiery sector and has a diversified product line for both men and women ranging from vests, briefs, trunks, boxers, thermal wear, panties, camisoles, leggings, loungewear, t-shirts, and socks .

- Value Chain: The Company has a total of 6 plants spread across 3 states namely West Bengal, Punjab and Tamil Nadu. It has strong control over its value chain, having its 100% in-house manufacturing plant with no outsourcing for any of its products. Along with that, it targets its customers through various third-party distributors and retailers . It also operates via self-owned exclusive retail outlets and large format stores. The Company has over 950+ distributors, 160 large format stores and 9 exclusive brand outlets across India.

- Geographies: It has a Pan-India presence with major sales from states such as Madhya Pradesh, UP, and Uttarakhand. Moreover, it also has a strong export market and serves more than 47 countries, having generated a revenue of Rs.133 crore from exports in FY20 (~11% of the total revenue).

Impact of COVID-19 on the Company

The entire hosiery industry had a huge hit due to a complete closure of the various retail marketplaces throughout the Country. India went for a complete lockdown on the 23rd of March, 2020 shutting the Company’s operations globally. However, it resumed its operations from May 2020 at lower capacities due to logistics and labor constraints. Despite the ongoing crisis, the Company has been able to reduce its overall working capital cycle. The revenue of the Company has declined by 12% YoY in Q1FY21, however, the domestic market has seen good traction in terms of sales for the Company since May and June, 2020. The Company’s exports experienced a huge hit due to the various global restrictions being imposed. Currently, the Company has been able to resume its operations in full capacity.

Differentiating Strategies

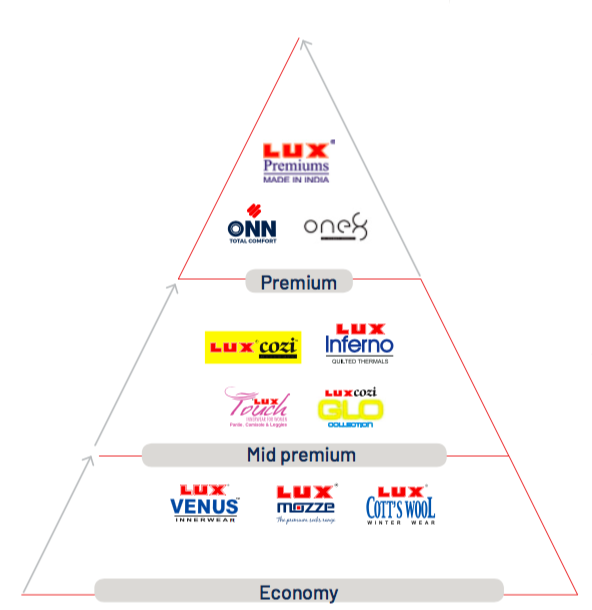

- Diversified Product Portfolio with the Widest Price Range throughout the Industry

LUX Industries has ensured to cater to a wide audience across the distinct mass, semi-premium, and premium segment by launching its products for all the consumer segments. It offers more than 100 products across 15 brands and are available at a price range of Rs.35 to Rs.1,350, widest throughout the industry. Consequently, Lux also deals across all categories in the innerwear industry and produces products in Men’s and Women’s Innerwear and Outerwear segment and also other complementary products such as socks and children’s wear. In the mid-premium and economy segment, Lux Cozi has emerged as the strongest and fastest-growing men’s innerwear brand and additionally, Lux Cozi Bigshot is one of the most preferred brands in the boxer/brief segment.

- Continued Momentum of Innovative Product Introduction

LUXIND has kept a vision of launching brands in every product category. In 2005, LUXIND introduced two products in the thermal category since this segment was under represented by branded players. While the competitors viewed “2” products in the same category as a foolish move, LUXIND ensured to position them distinctly at varied prices and hence, won over the market while capturing a larger market share in this segment and reporting revenue growth of more than 50% in FY19. In 2012, the Company came up with Lyra as a leggings brand, a strategy to capture the unorganized market by introducing a differentiated category. Simultaneously in 2017, it planned to extend Lyra from leggings to lingerie, a segment where the Company possessed no experience at all, however, the rapidly growing women’s innerwear segment enabled LUXIND to target its product towards the class audience and not the mass by pricing it mid-level and hence, winning over this product segment as well. Traditionally, vests are always appreciated for their softness, smoothness, and whiteness, however, recently, in April 2019, LUXIND came up with a unique dimension of a scented vest in order to address a long-standing need by introducing a pre-scented product in order to cater to the problem of sweat and odour in the body which witnessed a successful response with a 20% volume growth in Q1FY20.

- Increased Focus towards Premiumisation

Over the last few years, the Company has altered its product portfolio through a continuous increase in the number of premium products. Catering to the changing demands of the innerwear industry and serving the increasing consumer aspirations and spending on fashion, lifestyle, and comfort, the Company increased its brand spending and launched GenX and ONN for the mid-premium consumer segment. Currently, ONN is growing at of 20% YoY. The Company recently acquired the manufacturing and marketing right of One8, a premium brand owned by Indian Cricket player, Virat Kohli, to grow its share in the segment. When the entire population is evolving with greater product aspirations, this opportunity will help the Company capitalize more easily. The Company’s mid-premium portfolio in proportion to its overall portfolio has also increased and is growing at twice the rate of the overall growth rate along with a greater profit margin, further expanding the scope for prolonged profit growth in the near future.

- Maintaining Cost Leadership through State-of-the-Art Technology

LUXIND has emerged the cost leaders by operating at one of the lowest costs throughout the industry, hence driving operational excellence. The Company has focused on superior cost management through significant investment in manufacturing integration having 100% in-house facility and hence, scaling with an objective to reduce costs, enhance product quality, and strengthen trade terms. The Company has an integrated unit across knitting, processing, and cutting functions which strengthen the overall efficiency, productivity, and profitability. At LUXIND, they also recognize the need for having State-of-the-Art Technology by emphasizing technology upgradation and hence, have imported advanced equipment from multiple places over the years which includes 400+ stitching/sewing machines from Singapore, 50+ high-speed knitting machines from Germany, and 11 cutting machines from Italy. The Company has a manufacturing capacity of 20 crore garment pieces per year.

The Company’s Dankuni factory (having an area of 12 lakh sq. ft.) has a capacity to manufacture 5 lakh pieces of knitted products a day thereby having the largest manufacturing capacity in India’s Hosiery Sector. It has six manufacturing facilities located across 3 states. It also employs over 1496 workers, the largest in this sector, and has complete control over its workforce.

- Strong Distribution Network with Growing Global Presence

LUXIND has always ensured customer fulfilment and satisfaction through adequate capacity, timely delivery, and superior product quality. It has an extensive network of 950+ distributors with a Pan-India footprint, having a strong presence in western and central India, with over 35 years of engagement and a less than 1% attrition rate. LUXIND is also among the first innerwear company to hold conferences for distributors and owners, both within and outside India. The Company also possesses 9 exclusive brand outlets and over 160 large format stores to provide a one-stop platform for all its products. It is the export leader in the hosiery industry and experienced a 28% YoY revenue increase from exports in FY19 contributing to 11.2% of its total revenues. It has increased the number of its export countries from 22 to 47 over the last 5 years. The Company is also creating an online presence through various e-commerce websites such as Amazon, Flipkart, Myntra, etc. to tap a wider audience.

Swot Analysis

Strengths

- Cost Leadership: LUXIND have been able to reduce their operational costs and are producing at one of the lowest costs throughout the industry by taking advantage of its economies of scale. It has one of the highest supply capacities in the industry and has been continuously adapting to newer technologies to reduce its cost.

- Relationship with outside stakeholders: LUXIND maintains a strong relationship with its stakeholders which includes its distributors as well as its customers. It has maintained a relationship of over 35 years with its 950+ distributors with an attrition rate of less than 1% attrition rate.

Weaknesses

- Lower Margins compared to competitors: LUXIND has been able to grow its revenue at a rate of 10-12% and achieve an EBITDA margin of 14-15% in the recent years whereas one of its biggest competitor, Page Industries (owning the brand Jockey) revenue has been growing at the rate of 18-19% and achieve an EBITDA margin of 21-22% in the last 2-3 years. This has been primarily due to LUXIND’s major revenue contribution from the mid-premium and economy segment whereas Page focuses only on the premium segment which has contributed to a higher growth rate.

- Lack of Uniform Pan India Presence: The Company has maintained a strong presence in western and central India with a major proportion of its sales coming from Madhya Pradesh, U.P, and Uttarakhand and has not been able to position its product efficiently in the southern part of the Country.

Opportunities

- Huge Untapped Premium Innerwear Industry: The premium and super-premium segment of the innerwear industry is expected to grow at a CAGR of 17-18% in the next few years. However, currently, Page Industries, i.e. Jockey has already grabbed 55% of the premium innerwear segment whereas LUXIND currently holds only 1% share in this segment. Although LUXIND has been trying to change its product portfolio, it needs to radically tap this niche segment which offers a higher profit margin as well.

- Greater Consumer Demand and Emerging Export Markets: The Indian Middle Class is expected to grow at the rate of 1.4% outpacing China, Brazil, and Mexico. Moreover, the rising disposable income is making the Indian consumers more aspirational and fashion-conscious leading to greater demands for modern styles and more sophisticated products leading to a growing market for Innerwear and Maternity-wear. Moreover, the rising youth population is becoming more brand sensitive coupled with a desire to look good leading to a rise in premium brands. This offers a niche to the Company to offer newer products at pocket-friendly prices to capture the growing market. Additionally, apart from the abundant availability of raw material in our Country, India also has an advantage in terms of skilled manpower and lower cost of production as compared to major textile producing countries, hence, providing a greater opportunity for exports to countries at lower costs.

- Policy Initiatives to Promote the Textile Sector: The Government of India has increased the customs duty on imports from 10% to 20% in several textile products in 2018 to boost Make-in-India campaign, promote employment and increase the production of several Indian products. Such initiatives from the Government will enable the Company to follow its growth trajectory.

Threats

- Growing Competition in the Industry: The innerwear market is dominated by a large number of unorganized players which constitute around 60-65% of the market. Hence, this industry is witnessing an increasing entry of global brands with a higher level of domestic partnerships, thus, evolving into a more organized industry. LUXIND has been primarily competing with Rupa Industries, Dollar Industries, Page Industries, and VIP Industries to grab a greater market share in this segment. Companies such as Rupa and Dollar are also adapting their business models with the dynamically changing industry at an increasing rate by establishing strategic partnerships with global brands to obtain a greater pie in this industry. Thus, giving a great competition to LUXIND.

- The Rapid Shift in Consumer Trends: The innerwear products have now become a fashionable commodity than a necessary commodity. Being a fashion good, the Company needs to adapt to the rapidly changing fashion trends among the mass audience to survive in the industry.

- Economic Slowdown: Due to any slowdown, the fashion industry is severely hit due to the decreasing income of the consumers. Hence, any economic downfall is likely to affect the textiles industry and hence, LUXIND.

Michael Porter’s 5-Forces Analysis

Barriers to Entry

- Economies of Scale: The innerwear industry has been dominated by a number of big players who are operating at significantly lower costs, enjoying huge economies of scale. Hence, for an organized player to enter the industry, it will be required to manufacture at a huge scale in order to maintain a competitive price in the market particularly for the economy and semi-premium segment.

- Huge Marketing Cost: The existing competitors in the industry have established a strong brand presence by onboarding various popular brand ambassadors and hence, established a strong image of their brands.

- Strong Supply Chain Network: The hosiery sector particularly in the economy and mid-premium segment requires a strong network of distributors, multi-brand outlets, large format stores, and exclusive retail outlets apart from the online medium in order to cater to a wider audience.

Bargaining Power of Suppliers

- The Company has maximum of its operations, along the manufacturing chain, as in-house which reduces its dependency on suppliers. However, the Company does depend on 3rd party suppliers for few raw materials, and the dependency on them is reduced by getting into long-term contracts.

Bargaining Power of Buyers

- Being in a rapidly evolving fashion industry with a number of competitors, the customers in the mid-premium and premium segment are becoming highly fashion conscious and can easily shift to other substitutes if they are better in terms of comfort, design, and quality, provided they are at competitive prices. Thus, such a market provides higher bargaining power to the buyers.

- In the economy segment, the customers are highly sensitive to prices and might shift to a different brand if available at a lower price, however, LUXIND has been able to maintain a cost leadership and offer its products at the lowest possible rates in the economy segment.

Rivalry among Competitors

- Earlier, the innerwear industry was a highly fragmented one but has now evolved into a more organized space with intense competition among the major domestic players. With a rapid pace of growth in the industry in the foreseeable future, the competitors are trying to maintain similar prices and enter into every product segment possible to capture a share in the market.

Threat of Substitutes

- LUXIND has always ensured to bring in innovative products for its customers and has emerged as a leader in particular segments such as thermal wear. However, this industry has been recently focusing on product differentiation through the creation of different brands while providing similar product utility to customers. In recent times, every company has been trying to introduce newer brands and products in the mid-premium and premium segments. Thus, due to the high intensity of competition present in the industry, there is a higher threat of substitutes.

Branding & Other Initiatives

- Focus towards Creation of a Brand

LUXIND has always believed in building a brand and has spent significantly over the years for the same. Capturing the innerwear industry required LUXIND to turn into an organized, branded player and mark its presence in the earlier fragmented market space. The Company has increased its brand spending from Rs.31 crore in FY12 to Rs.89 crore in FY20 and investing an overall amount of Rs.566 crore in the last 8 years to build its brand. It has ensured a continued investment of 7-8% of its turnover towards building its own brand. From having ambassadors like Sunny Deol, Shahrukh Khan, Amitabh Bachhan, Varun Dhawan, and Karthik Aaryan, the Company has created a strong image and visibility. The Company ensured a rejuvenation of its brand and shifted to a younger brand ambassador, Varun Dhawan in 2017 to connect with the rapidly growing millennial consumers. The Company also sponsored the KKR Team in the Indian Premier League, gained an international presence and created a strong recall for the Indian millennial audience. The Company’s revenues from every rupee invested in brand spending increased from 5.74% in FY13 to 7.39% in FY20.

- Rapid Brand Transformation

The Company has ensured to rejuvenate its brand architecture in every 2-3 years by adopting newer promotion outlays and messages, hence, preventing its brand to grow old. In the last few years, LUXIND has primarily focused on improving and changing its brand by targeting the premium segment. A brand that earlier targeted mainly the mass segment now focused more on premiumization. LUXIND strongly believed in transforming its products, from merely being recognized as innerwear products to become an integral part of the aspiring Indian’s wardrobe. The Company is also witnessing a shift from being merely players in the innerwear industry to introducing products like casual wear for the large mid-income segment hence, entering into a different space.

- Dynamic Brand Positioning

LUXIND has tried to position its brands through popular ambassadors, the selection of which always had a particular strategy assigned to it. Firstly, when Varun Dhawan was made the brand ambassador of Lux Cozi, which has the largest market share in the mid-premium and economy segment, the Company made a shift from Sunny Deol to target the youth population and resonate with the aspirational style quotient of India. Similarly, Amitabh Bachhan was made the brand ambassador for LUX Venus as his personality is liked by people of all demographics. This was also the time when the entire economy was trying to escape from the negative effects of GST and demonetization, and the only way to ensure growth was not only scaling production but leveraging its own brand through relevant celebrity endorsements. Moreover, the Company also invested in its tagline “Yeh Andar Ki Baat Hai”, hence retaining audience recall. Moreover, when LUXIND launched Inferno, its thermal wear, the Company onboarded Karthik Aaryan along with Amitabh Bachhan to target both the growing youngsters and the adult population hence, recording a significant revenue growth in Q2FY20.

- Distributor Loyalty Programs and Conferences: LUXIND has organized numerous conferences in regions like Varanasi and other adjoining areas with regional sub-distributors and retailers which helped them build trust and also generate orders for the Company. Moreover, Lux Corporate Club is a program started in the year 2014-15 for the distributors in which membership is provided after reaching a particular sales benchmark. The membership is divided into categories- Platinum, Diamond, Gold, and Silver under which the distributors get a host of rewards and privileges. A leisure tour to London was conducted for the first-year Platinum and Diamond members and a Bali leisure tour was conducted for the Gold members

- Corporate Social Responsibility (CSR) Initiatives: The Company has been responsible for ensuring community development through an investment of Rs.2.02 crore in CSR activities in FY18-19. It undertook an initiative under the Swachh Bharat Abhiyan through the installation of bins in West Bengal to keep areas safe and clean. In order to provide quality education to local children, LUXIND built up the Saraswati Sishu Mandir School at Bali, Murshidabad. The Company carried out these projects through Lux Foundation (its own CSR Trust) in collaboration with registered trusts, NGOs, Section 8 companies and hence, implemented its CSR goals. The Company has also set up Solar Panels in its Dankuni manufacturing plant, its largest manufacturing unit, which will serve more than 40-50% of the energy requirement.

Financial Analysis

- Bottomline Growing Faster than the Top-Line

The Company’s revenue over the years has been growing at a CAGR of 9% from FY13 to FY19, however, the profit after tax has grown with a CAGR of 31% from FY13 to FY19. The Company has been able to achieve this constant revenue growth through its continuous product introduction and branding initiatives which constitutes 7-8% of its revenues. However, this greater growth in the bottom line can be attributed to the Company’s continuous ability to reduce its cost and hence, achieving a higher profit margin every year. From FY13 to FY19, LUXIND has increased its EBITDA margin from 5.98% to 15.68%. The main driver behind this feat is its ability to constantly increase its production capacity and adapt to newer technologies which allows it to reduce its cost and maintain leadership. Moreover, the Company’s focus on changing its product portfolio to a greater number of premium products has also provided such an increase in the Company’s EBITDA margin. Lux’s high-end brands like ONN and Lyra gives the Company with 16-17% operating margin as compared to its economy brands providing a meagre 8% margin.

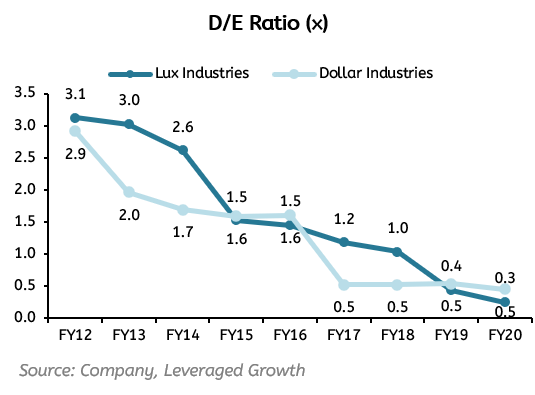

- Reduction in Debt-Equity Ratio

Over the years, LUXIND has also been able to reduce the Debt-Equity Ratio (D/E) substantially, through constant debt repayments over the last few years. The Company has lowered its long-term borrowings from Rs.4,410 crore in FY12 to Rs.638 crore in FY20. However, ifLUXIND undertake expansion projects in the near future and take debt for the same, the ratio will again start showing an up-trend, although if the same is done through internal accruals, the Company can maintain the ratio at current levels. The Company has successfully reduced the D/E ratio from 3.13 in FY12 to 0.25 in FY20.

- Negative to Positive Cash Flows

LUXIND adopted a change in its policy and shifted from sales maximisation to focusing on quality of sales in FY19. In FY18, the Company focused on sales maximisation through increased brand spending, working with business partners and selling as much as possible due to the adverse effects of the GST policy. The Company adopted a change in FY19 after having achieved a creditable growth momentum and started focusing on sales premiumisation rather than sales generalisation. Lux primarily focused on improving its relationship with its trade partners by timely recovery of its receivables rather than extended receivables. Any company experiences greater respect when it reflects it profits in its cash & bank than hiding in its debtors, achieves greater business appraisal clarity, becomes more sustainable and acquires greater credit ratings. This decision in turn helped the Company to achieve a greater cash flow of Rs.192 crore in FY19. Due to such increase in its cash flows, the Company has also been able to reduce its debt significantly in FY18. However, with the focus of the Company shifting from sales maximisation to sales premiumisation in FY19, the cash flow of the Company dipped from Rs.192 crore in FY19 to Rs.106 crore in FY20.

Risk Analysis

- Global Economic Slowdown: The Company generates 10% of its revenues from exports and has established its presence in more than 47 countries. A slowdown in the global economy might affect the purchasing powers of the consumers thereby reducing the demand for its products hence, affecting its revenues.

- Commodity Price Risk: There is a risk of price fluctuation of raw materials like cotton, yarn, and chemicals used in the process of manufacturing. However, through backward integration at a few plants and long contracts, the Company has managed to reduce this risk.

- Change in Fashion Trends: Being in the fashion industry, the trends among the growing aspirational class keep on changing rapidly and an inability to adapt to these changes might lead to loss of customers and hence, reduced sales. However, the Company has kept a specialized design team to cater to such risks. Moreover, LUXIND has always been ahead in introducing newer, innovative products in the market, hence, becoming the trendsetter.

- Human Resources: It is the ability of the organization to attract and retain employees while delivering value to its employees. Lack of availability of human resources and increased employee turnover might affect the overall performance of the Company. In the FY18-19, LUXIND was able to maintain a retention rate of 96% in the organization.

- The Risk from Competition: The innerwear industry being a highly fragmented one intensive competition from domestic players both organized and unorganized, and also from countries such as Sri Lanka, China, Taiwan, and some African countries. Such increased competition can create pressure on margins, market share, etc. However, LUXIND has tried to differentiate itself through its enormous brand presence and low manufacturing costs in order to set itself apart from its competitors.

Corporate Governance

- The Company’s board consisted of 7 Directors out of which 4 were Independent Directors and the total directors include one woman Executive Director and one woman Non-Executive Independent Director. The composition is in compliance with the SEBI (LODR) Regulations.

- Mr. Ashok Kumar Todi, Mr. Pradip Kumar Todi, and Mrs. Prabha Devi Todi belong to the same family and are related to each other. Mr. Ashok Kumar Todi and Mr. Pradip Kumar Todi are brothers and Mrs. Prabha Devi Todi is the wife of the elder brother. Besides this relationship, there are no other inter-se relationships amongst the Board Members.

- Mr. Ashok Kumar Todi holds 15 other directorships, Mr. Pradip Kumar Todi holds 15 other directorships and Independent Directors Mr. Nandanandan Mishra holds directorships in 3 other companies, Mr. Snehasish Ganguly holds directorships in 9 other companies and Mr. Kamal Kishore Agarwal holds directorships in 1 other Company. However, none of the directors of the Company hold directorships in more than 20 companies or more than 10 public companies, whether listed or not.

- Besides the six board meetings that were held in FY2019, one separate meeting was held among the independent directors on February 12, 2019.

- Promoters have not increased their shareholdings which remained constant at 69.51% of the total shareholdings as of June 2020.

- The shareholding pattern of Lux Industries has witnessed a change in the last 3 years. Of the total share, the promoters have maintained a constant shareholding of around 69.51% while there has been a change in the public shareholding pattern of the Company.

The EndNote

- In the short term, LUXIND aims to moderate its working capital cycle from four months to two months across 5000 SKUs, implement its merger deal with J.M. Hosiery and Ebell Fashions, moderate the receivables cycle from around 90 days to 70 days, lower down its short term debt, increase the proportion of premium products in its portfolio and increase its EBITDA margin.

- LUXIND currently aspires to achieve a revenue growth from Rs.1206.90 crore to Rs.5000 crore (~314.28% increase) by 2025 and in the process create Lux Cozi as 1500 crore brand, Lux Venus as Rs.700 crore brand, Lyra as Rs.50 crore brand, multiple brands of Rs.300 crore and reach an export revenue of Rs.500 crore.

- The Company currently has been able to achieve constant growth to date, however, the competition among the organized players in the industry has been increasing with every passing year. Players like Rupa, Dollar, Page are also constantly achieving greater heights, improving their business models and the industry is shaping into a more organized segment.

- Currently, the innerwear industry provides an attractive opportunity in the premium segment with consumers becoming more fashionable and brand conscious. However, LUXIND currently holds a very small portion of this segment, while Jockey (owned by Page Industries) holds the majority chunk in the market. In order to achieve an even higher bottom-line growth, the Company needs to lay down a greater focus on developing a premium brand for the consumers which can compete with the existing players in the premium segment of the industry.

- Overall, the Company seems to be achieving a constant growth in revenues and profits with a continued focus on brand strengthening and improving its cash flows and financial profile. With its merger being implemented, LUXIND shall also be able to enter into newer segments of the textile industry.

Note: Lux Industries Limited went for a share split from Rs.10 to Rs 2 on the 6th of June, 2016. The share has been quoting on an ex-split basis since June 06, 2016. As a result, the Company’s share price plummeted from Rs.3,496 on the 6th of June 2016 to Rs.693.05 on the 7th of June 2016.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Yash Raj Sureka

Research Desk | Leveraged Growth