Emerging Markets are no longer a high-beta derivative of the S&P 500. A quiet, decade-long architectural overhaul in the Global South has produced an independent economic engine and the market is still pricing it like 1998.

For decades, the global financial markets followed a rhythm as predictable as the tides: when the West moved, the world followed. Emerging Markets (EM) were long viewed as the “high-beta” version of the Developed World, thriving in times of global abundance but among the first to be sacrificed when the Federal Reserve tightened its grip. The logic was simple: EM growth was a derivative of Western demand.

As we move through 2026, a fundamental shift is challenging this age-old correlation. The MSCI Emerging Markets Index has surged 33.6%, nearly double the return of the S&P 500. The historical correlation between the two, once above 0.80, has frayed to a five-year low of approximately 0.45. This is not a seasonal anomaly. It is the emergence of an independent economic engine.

[Note: Correlation figures as of February 2026]

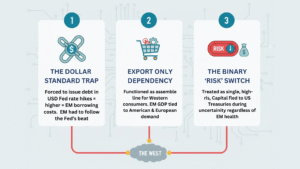

Three Anchors: Why the World Used to Move in Lockstep

To appreciate the current decoupling, one must first understand the gravity that kept Emerging Markets grounded for so long. For decades, EM economies were tethered to the West by three structural chains.

- The Dollar Standard Trap

Because most emerging nations lacked deep local bond markets, they were forced to issue debt in US Dollars. This created a brutal paradox: whenever the Fed raised rates to cool the American economy, it inadvertently throttled EM growth by inflating their borrowing costs. The Fed was the world’s drummer, and EM had no choice but to follow the beat.

- Export-Only Dependency

Emerging economies functioned as the back office and assembly line for Western consumers. EM GDP was a direct function of the American and European shopping cart. No Western demand meant empty factories in the East.

- The Binary “Risk” Switch

Global fund managers treated EM as a single, undifferentiated high-risk bucket. In times of uncertainty, capital retreated to the perceived sanctuary of US Treasuries instantaneously without examining local balance sheets in Jakarta or Mexico City leaving these markets starved of liquidity regardless of their underlying health.

The Engine Room: Why the Wedge Is Widening

The decoupling of 2026 is not a stroke of luck. It is the result of a quiet, decade-long architectural overhaul within the Global South, one that built three new engines of independence while Western economies were managing the fallout of prolonged restrictive monetary policy.

- The Era of Monetary Maturity

In the old world, EM central banks waited for the Federal Reserve to move before they dared adjust their own rates. That era is over. By acting aggressively and early to combat inflation in 2023–2024, many EM nations stabilised their currencies and built a meaningful policy buffer. Today, while Western economies remain in a restrictive cycle, many emerging markets are already deep into easing, injecting liquidity when their domestic conditions demand it, not when the Fed permits it.

- The Rise of South-South Trade

Perhaps the most consequential structural shift is the death of the Western Consumer as the sole arbiter of global growth. For the first time, trade volume between emerging markets has eclipsed their trade with developed nations. This South-South loop has created a self-sustaining ecosystem. ASEAN nations are benefiting from “China Plus One” manufacturing diversification; India and Brazil are leveraging large, tech-enabled domestic consumer bases. These economies are no longer waiting for a US stimulus check to find their next buyer.

- The Tech Sovereignty Pivot

The most misunderstood structural pillar is the shift from cheap labour to critical intellect. Select emerging and recently-developed markets have become the hardware backbone of the global AI revolution. Nations like Taiwan and South Korea, though frequently classified as Developed Markets by MSCI, underscore a broader regional dynamic: the Asia-Pacific corridor now provides the silicon infrastructure upon which the world’s most advanced AI systems run. This is not merely growth; it is an evolution into strategic indispensability, increasingly decoupled from Western consumer sentiment.

A note on classification: investors should be aware that Taiwan and South Korea are categorised as Developed Markets by MSCI, meaning their performance does not appear directly in the MSCI EM Index. The broader point about tech sovereignty as a regional tailwind for EM-adjacent economies remains valid, but index-level analysis requires this distinction.

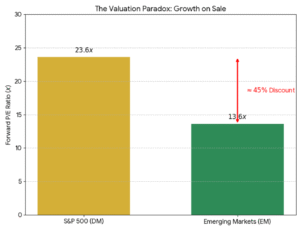

The Valuation Paradox: Growth on Sale

Despite these structural upgrades, investor sentiment suffers from what might be called a legacy lag. Most global allocators are still pricing Emerging Markets as if they were the volatile, externally-indebted asset class of the late 1990s.

The S&P 500 currently trades at a Forward P/E of approximately 23.6x, a premium that reflects decades of perceived safety and deep capital markets. The MSCI EM Index, by contrast, trades at roughly 13.6x, a discount of approximately 45%. It is worth noting that a valuation gap between developed and emerging markets is historically persistent and not unusual in isolation. What makes the current spread notable is its combination with improving EM fundamentals, monetary independence, and reduced external debt vulnerability — factors that the legacy discount does not adequately reflect.

Structural Shift or Seasonal Fluke?

The 2026 data confirms that the Great Decoupling is no longer a theoretical debate it is a market reality. However, the only question that matters for long-term capital allocation is sustainability.

History cautions against linear extrapolation. While the New EM has built a more robust immune system, it is not fully insulated from global shocks. A sharp reversal in Western inflation, a geopolitical rupture in key trade corridors, or a sudden dollar strength episode could still send tremors across these markets. The decoupling thesis does not require EM to become invulnerable only that it has become meaningfully less dependent on Western cyclicality than at any point in the past three decades. The evidence for that, at least, is compelling.

What This Means for Investors

The lesson here is not to abandon Developed Markets entirely, but to recognise that the old safe playbook has been quietly rewritten. The 45% valuation discount currently embedded in Emerging Markets provides a significant cushion but realising it requires a discerning approach that distinguishes between the Old EM (vulnerable, export-led, dollar-indebted) and the New EM (domestically driven, monetarily sovereign, tech-integrated).

The correlation that once made EM a simple high-beta trade on the S&P 500 has structurally weakened. Whether it stays weak will depend on how deeply the South-South trade architecture holds, how EM central banks manage the next global shock, and whether Western capital continues to price these markets with the ghost of a crisis that is now nearly thirty years old.

The divorce may not yet be final. But the Global South has definitely changed the locks.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice. All valuation and correlation figures should be independently verified. Past market behaviour is not indicative of future results.

Contributor: Team Leveraged Growth