Connecting Aspirations

Click here to download the report

Key Highlights

- Tata Motors Limited (TML) experienced growth in volume by 67% as compared to industry growth of 13%

- It agreed with the TPG rise climate to invest ₹7500cr in the passenger car segment

- It has outstripped the regulatory compliances of BS VI regulations for the enhancement of customer value addition

- Its distribution network is spread over 16000 workshops to provide the best-in-class service for its vehicles

- It is still struggling to develop a concrete hold in the luxury car segment

Automobile Industry

- The Indian automobile industry is worth $222bn

- The industry is currently the 4th largest automobile manufacturer in the world

- Maruti Suzuki leads the industry with a market share of 41.63%, followed by Hyundai 13.87%

- Tata Motors ranks 3rd with a market share of 13.15%

Business Overview

TML is a global leader in the automobile industry with a diversified portfolio of commercial, passenger, and luxury vehicles. The Company has been a part of the $113bn Tata Group, founded by Jamshedji Tata in 1868. It is one of India’s leading automobile manufacturing companies with a wide range of integrated, innovative, and e-mobility solutions in its portfolio. TML introduced new passenger cars and utility vehicles that offer a superior blend of performance, drivability, and connectivity.

The Company believes in ‘Connecting aspirations’ by offering innovative mobility solutions that align with the customer’s aspirations. TML is in the business of operating, designing, and manufacturing automobiles, including sports utility vehicles, trucks, buses, and defense vehicles, with creativity and innovation.

Journey – Tata Motors Limited

Industry Analysis

The automobile industry, which currently accounts for 3% of the economy’s output, is undergoing an epochal change. The pandemic opened up the mind of automobile manufacturers to a broader level. The consequences they had to face during the pandemic, given their heavy dependence on exports in the form of raw materials, made them suffer severely as all the cross-border flow of goods was on hold for almost a year. To end this dependency, automobile manufacturers now want control over the raw materials required for their production units. The key industry players have started moving up the supply chain and are seen to add value through their business model.

Besides taking a step to move up the value chain, the industry saw a shift from the compression-ignition engine to the Electric Vehicle (EV) segment. The EV segment was a comprehensive solution to the COVID-related plant shutdowns and logistical problems. These problems led to the underutilization of the industry’s manufacturing capacity, resulting in manufacturers building 7.7bn fewer vehicles than they could produce. TML was the first automobile manufacturer in India that come up with this concept and is currently the only player in the country offering EVs.

The Indian automotive industry is worth $222bn. The 4th largest automobile manufacturing industry currently manufactures 23mn vehicles, including passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycles. Two-wheeler vehicles, followed by passenger vehicles, account for the largest share in terms of unit sales. India has a bright outlook for the automobile industry, given the driving growth from the EV segment.

Business Model

TML scaled up its market coverage and increased its presence to 75 cities and 143 dealerships in FY22. The Company came up with exciting new products to cater to consumer demand in the form of Tigor EV and Nexon EV for the fleet segment. It also endeavors to achieve its transition phase from conversion to the multi-energy modular platform to a pure EV platform in the next few years. The Company is working to enhance its capacities to meet the increased demand and deeper into the localization of Tier 1 and 2 components.

- Stakeholder engagement forms the heart of the company’s business model. TML continuously engages with its investor, employees, customers, regulators, and other stakeholders to resolve their concerns using a practical stakeholder management framework.

- TML increased its focus on digital campaigns, which facilitated its customers to access their product information quickly and enabled them to book a vehicle in the comfort of their home/workplace.

- The company undertook other digital initiatives, including the connected vehicle platform and fleet edge. These actions were underpinned by data analytics. The motive behind the undertaking of these initiatives was the company’s aim to improve customers’ business operations through trip management, expense management, maintenance planning, and spare vehicle management.

- For better management of demand volatility during the COVID and post-COVID scenario, TML activated its business agility plans and switched back to fortnightly production planning, enhancing its operating efficiency.

- The rise in the prices of inputs involved in the manufacturing process, especially steel and metals, initially forced the Company to pass on the price to its customers through increased product prices. The Company further strived to absorb the increase in price by absorbing the increase in costs at various manufacturing levels.

- The business model of TML strives to create value by innovating sustainable mobility solutions to enhance the quality of life.

- The company’s business model is built based on strong and sustainable growth, which continuously focuses on operational excellence, benchmark performance, continuous innovation, and improvement of existing performance.

Product Profile and Market Share

With new architectural platforms and efficient engine options, TML continuously strives to improve its product portfolio across all segments of vehicles the Company offers. The Company is working towards connecting aspirations by bringing dreams to life complemented with affordability using their engineering efforts, offering the customers the best in design, connectivity, and safety.

- Commercial Vehicles: The Company came up with the launching of 80 new products and 120 variants across segments. The Company gained domestic market share in all the sub-segments under this segment.

- Passenger Vehicles: Tata Motors Ltd. introduced over 25 new products and variants to become a leader in this fastest-growing market with the segment’s market share of the company being 12%.

- Electronic Vehicle: Tata Motors agreed with TPG Rise Climate to invest ₹7500 crores in the passenger EV business to secure 11-15% shareholding.

- Jaguar Land Rover (JLR): This segment of the business saw great demand with the launch of the new Range Rover.

Subsidiaries

- Jaguar Land Rover, known for shaping the future of luxury four-wheel vehicles globally, has been a wholly-owned subsidiary of TML since 2008.

- Tata Daewoo Commercial Vehicle (TDCV), Korea’s largest truck exporter – exporting to more than 60 countries, is a crucial subsidiary of TATA motors.

- Tata Technologies Limited – a leader in energy services outsourcing and product development IT services is also a key subsidiary of TML that provides a competitive edge to the Company over other global manufacturers.

- Tata Motors Finance Holdings Limited – a 100% subsidiary of TML, is a core investment company that undertakes the dealer/vendor financing, and the used vehicle refinance/repurchase business.

Differentiating Strategies

- TML has extended its product portfolio after studying the consumer’s changing interests to differentiate itself from the other brands in the industry. This differentiation, in addition to a cost leadership strategy, has helped Tata Motors to build a solid and loyal customer base

- TML, being an experienced industry player, has made heavy investments in marketing, advertisement, and celebrity endorsements to differentiate itself from other brands

- The brand logo for the Company itself forms a differential basis. This is because despite going through several revisions, the essence of its service and quality remains the same, which makes it a global leader in the industry

Michael Porter’s 5 Forces Analysis

Barriers to Entry

- Capital-Intensive Industry- Designing, manufacturing, and selling vehicles is capital-intensive and requires substantial investments in tangible and intangible assets such as R&D, product design, and engineering technology

- Distributor Network- The sales of products are performed through a network of authorized dealers, service centers diversified all over India, and a network of distributors and local dealers. The creation of a distribution network like this is a time-consuming process and requires a significant amount to be invested

- Technology and Innovation- The dynamic preferences of customers buying vehicles and the evolution in technology requires automobile companies to make considerable investments in R&D and technology to serve better than their peers in the industry

- Regulatory requirements- According to the regulatory restrictions and policies brought in by the government, a legal trade licensing formality needs to be fulfilled before a company can start selling, which makes it difficult for new entrants to get into this industry

Bargaining Power of Suppliers

- Since the automobile industry forms a significant chunk of its suppliers’ customer base. This means that the industry profits are closely tied to the suppliers. These suppliers, therefore, have to provide reasonable pricing and hence weaken the bargaining power of suppliers

- The products these suppliers offer is relatively standardized, less differentiated, and have minimal switching costs. This makes it an easy call for Tata Motors to switch suppliers

Bargaining Power of Buyers

- The entire automobile industry is pumped up with competing players fighting to capture a more extensive customer base. Besides, customers’ accessibility to various online resources has enabled them to perform comprehensive cost and quality analysis at the time of purchase. This leads to high bargaining power of buyers in the industry

Rivalry Among Competitors

- The automobile industry is highly competitive, and the industry participants are striving to develop better innovations and enhanced quality products at relatively lower costs than what other brands are offering

- Tata creates a competitive edge against its competitors by being one of the few brands in the country to develop the latest technology in their products.

Threat of Substitutes

- The substitutes available in the industry are pretty significant in numbers. Still, the amount of investment involved in buying a vehicle comprises a substantial portion of consumers’ income, making it difficult for them to switch frequently. This lowers the threat of substitutes in the industry

- TML offers its products at a price lower than what its competitors are offering, thereby creating a moat around its customer base

Branding and Other Initiatives

- TML introduced “Anubhav,” showroom on wheels, a doorstep car buying experience for rural customers to expand its reach in Tehsils and Taluka, which have a high potential in terms of the rural population, and economy

- The Company took every regulatory change as an opportunity to enhance customer value and increase competitiveness. Its BS-VI range of Tata Motors goes beyond mere regulatory compliance and delivers enhanced value propositions for its customers

- Tata Motors Limited, in association with WAT Consult, launched a digital campaign, “Atmanirbharta by Tata Motors,” that highlighted the existence of localization in everything it does

- TML launched E-Dukaan, a digital storefront for vehicle spare parts, and they were able to expand its customer base by reaching customers who were unable to locate physical outlets

Awards and Recognitions

- Tata Motors CV Pune and Pantnagar won the “National Energy Leader” and “Excellent Energy Efficient Unit” for Excellence in Energy Management 2021

- The Jamshedpur, PV Pune, Sanand, and Dharwad units were recognized with the “Excellent Energy Efficient Unit” award at the CII National Award for Excellence in Energy Management 2021

- Lucknow unit was recognized with the “Energy Effective Unit” award at the CII National Award for Excellence in Energy Management 2021

- The Lucknow unit won the “2nd Prize” at the Uttar Pradesh State Energy Convention Award 2021

Financial Analysis

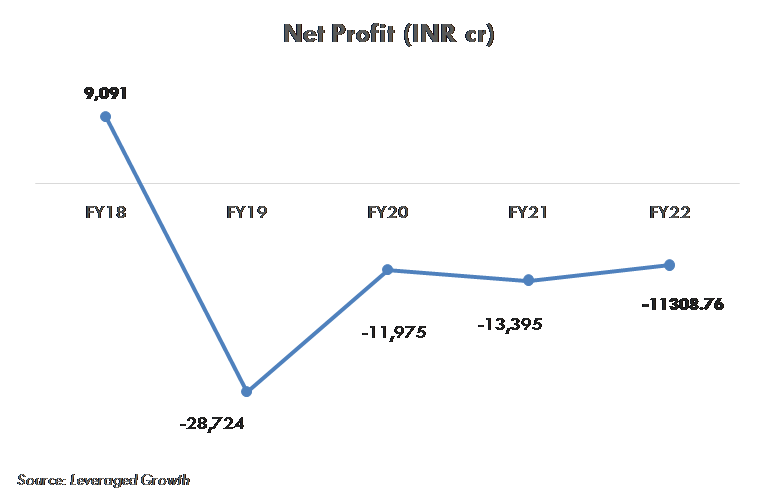

- Revenue from Operations: The company’s revenue from operations in FY18 was mainly driven by its most credible PV segment growing by 13.8% against the industry growth of 2.8%. TML saw a 2.9% increase in its consolidated revenue from operations in the next year, FY19, which could be remarked as the most revenue-generating year for the company in over a decade. The year after that saw a significant fall of 13.4% in the company’s revenue which was due to the pandemic during the time frame. TML, post FY20, undertook several initiatives to return to its previous level. The company somehow was unable to recover and again experienced a fall in its revenue. The magnitude of this fall in revenue was reduced to 4.4% in FY21. The company then saw a rise in its revenue in FY22 at a rate of 10.3%.

2. Net Loss Minimization: TML reported a consolidated net loss of 315.96% in FY19. This tremendous transmission from a net profit reporting company to a net loss company was mainly because of the impairment loss recognized in view of the changing market conditions, especially in China, and technological disruptions. The company recovered its losses heavily towards the end of FY20 on account of the unlocking of the economy.

The second wave of the pandemic further negatively impacted TML resulting in an increased net profit/(loss) of (11.86%) in FY21 as compared to FY20. The economy revival, post the delta variant helped the company to recover its losses resulting in positive impact of 15.57% in net profit/(loss).

The reasons for the same were:

- The Company’s earnings before other income, finance costs, foreign exchange gain/losses, exceptional items, and tax for Jaguar Land Rover is a loss of ₹439 cr in FY22 as compared to a profit of ₹7,691 cr in FY21. The enormous change was brought by Jaguar Land Rover charging ₹15,350 cr as an exceptional item.

- Loss before other income, finance costs, foreign exchange gains/losses, and exceptional items, for Tata Passenger Vehicles was ₹660cr in FY22 compared to ₹1,564 cr in FY21

3. Debt-to-Equity ratio: The Debt-to-Equity ratio of TML saw an upward trend experiencing an increase of 3.6 times over the last five years. There was a 21% change in the debt-to-equity ratio given the increase in debt in FY22 compared with FY21, and an increase in losses which has led to a fall in the equity resulting in a higher debt-to-equity ratio of 2.9 as compared to 2.4 in FY 21.

4. Return on Equity: The Return on Equity movement of Tata Motors over the last five financial years was an outcome of the company’s net profit/(loss). The ROE experienced a significant downfall of 408% in FY19 on account of the net loss that contributed a lower weightage to both the ROE variables. In FY20, the company reported an improvement in its ROE by 48.65%. The company had severely been affected by the pandemic which further propelled the ROE to fall to -22% in FY21. The Russian invasion of Ukraine restricted the global growth of the automobile industry towards the end of FY22 and TML reported a nominal improvement of 4.55%.

Risk Analysis

- Shortage of semiconductors impacting production levels: The shortage of semiconductors in the automobile industry will impact TML more pronouncedly than it affects the entire automotive industry. This is because all other players in the industry have bargaining power with suppliers, which is more prominent for the production of vehicles that are dependent on semiconductors. The company’s capacity to ensure a sufficient supply of semiconductors is limited by the uncertainty caused by the pandemic and the sudden shutdown of factories. The most important raw material crunch will continue in the near future as no such alternative for semiconductors is readily available in the industry.

- Concentration of customers in key market areas: The company relies significantly on countries, including the United Kingdom, China, North America, India, and continental Europe, where it derives a significant chunk of its revenues. A fall in demand for a company’s vehicles in any of these countries may impact the company’s business operations and financial condition. This was evident in November 2020 when the UK government announced a ban on selling new conventional petrol and diesel cars from 2030 onwards.

- Operational risk in connection with the use of Information Technology: The company is exposed to the risk of losses that could result from the failure of internal processes, violation of internal policies by employees, and interference of information technology and computer systems. The advancement of technology and connection to the internet in vehicles has exposed the company to various operational risks. The protection measures deployed in place, given this risk exposure, if proved insufficient, the company’s results of operations would be materially impacted. This could further lead to negative impacts on reputation and material financial loss in extreme cases.

- Exchange rate fluctuations: TML’s operations rely on risks arising from the movements in exchange rates of the countries where the company operates. The company imports raw materials and equipment and sells vehicles to various countries. Hence its cost and revenues are exposed to the movements of the GBP, the USD, and the respective currencies of Singapore, Japan, Australia, South Africa, Korea, and India.

SWOT Analysis

Strengths

- Global brand recognition: TML has expanded the company’s market and increased the company’s market and brand value by selling vehicles under various brands like Jaguar Land Rover, Tata Hitachi, Tata Daewoo, Tata Marcopolo, etc.

- Established Distribution System: The company’s global distribution network is spread over 1600 workshops which cover 90% of the company’s district. This also gives Tata Motors a competitive edge and helps in market penetration.

Weakness

- Higher operational costs leading to lower profit rates: The acquisition of brands like Jaguar and Land rover by TML was wasteful in the initial years and resulted in the company being independent of its subsidiaries. This led to a decrease in the overall sales and profits of the company.

- Limited Presence: Despite operating globally in 125 countries, the company failed to create a substantial impact on its competitive brands like Ford, Toyota, Honda, and Volkswagen.

- Negligible hold in the luxury segment: The luxury car segment is considered more profitable, but Tata Motors is still struggling to find a concrete hold.

Opportunities

- Growth in purchasing power of Indians: A growing trend in the income and spending capacity of Indian consumers is a massive opportunity for TML. If it produces technically advanced cars at reasonable costs, the company may observe a significant growth in revenue in the coming years.

- Expansion in the car market: The reliance on transportation in today’s world is a massive opportunity for the company as it will boost automobile companies’ sales.

- Mergers and Acquisitions: The company regularly examines various corporate opportunities, including suitable mergers, joint ventures, acquisitions, and divestments, to determine opportunities to enhance its strategic and financial performance.

Threats

- The rising cost of production: Increased competition and low production levels in the semiconductor industry have led to companies paying increased prices for semiconductors. Tata Motors is struggling to find measures that could minimize the impact of the high price paid for its raw materials.

- Competition in the luxury car segment: The company faces intensifying competition in the premium passenger car segment, which is anticipated to continue further in the long term. A range of factors that affect this competitive environment are the quality and features of vehicles, ability to control cost, pricing, reliability, safety, fuel economy, and Research and Development.

- Increase in fuel cost: The price of fuel in the company’s operating segment is a variable that is directly related to the sales of an automobile company. The increase in energy price is a threat to the company and its competitors.

Environmental, Social, and Governance

Environmental

Water conservation

TML acknowledges the significance of water as a shared and scarce resource. The company is committed to efficiently utilizing water by maximizing effluent recycling and re-use at all our manufacturing plants and minimizing leakage and waste. In FY22, the company conserved 9.24L meter cubes of water through recycling, effluents, and rainwater harvesting, which is 19% of the total consumption.

Waste management

A critical part of the company’s operating efficiency is waste management. In FY22, Tata Motors made sustainable efforts across plants to divert hazardous waste from landfills/incineration and derive value from the same. The company plans to this initiative and achieve the ultimate goal of ‘Zero Waste to Landfill’ status for all its manufacturing operations.

Social

The company’s commitment to empowering its people and offering them safe and healthy workspaces to work and grow. Tata Motors has also taken several initiatives to ensure a healthy and conducive working environment for its women workforce. The company also undertook initiatives like Arogya (Health), Vasundhara (Environment), Vidhyadhanam (Education), and Kaushalya (Employability) for enhanced community engagement and development.

Governance

The Company’s board consists of 3 Non- Executive Directors, 5 Independent Directors, and 1 Executive Director. Tata Motor’s board consists of qualified board members that bring diversification of relevant skills, competence, and expertise. This helps the company guide and shape the company’s competitive position and strategic way forward.

Shareholding Pattern

COVID-19 Impact

The financial year FY22 has been a turnaround year for the company’s commercial vehicle segment after being significantly impacted in the past few years by the COVID-19 pandemic; changes brought in by regulation, liquidity crunch, and the slowdown of GDP growth. The growth was initially impacted by the second wave of the pandemic, which led to a significant demand recovery speed downturn in the post-lockdown period. However, the beginning of the second quarter witnessed a rise in the company’s demand leading to better gross margins. The semiconductors and chip shortage problem that arose after the pandemic remains an area of concern for Tata Motors Limited. The company is paying more to its semiconductor suppliers to meet its demand and be ahead of its competitors. Despite the higher prices and shortage of semiconductors problem which came as an output of the pandemic, the company’s implemented measures have helped improve margins to some extent.

End Note

The automobile industry is currently going through many changes. The hike in semiconductor prices, BS VI regulatory norms, and the recent entry of Electronic Vehicles (EVs) into the Indian markets comprise a significant part of those changes.

Will Tata Motors be able to sustain its EV customer base and continue to be the leader in the upcoming trend of EVs?

Disclaimer: The report and information contained herein are strictly confidential and meant solely for the selected recipient and maynot be altered in any way, transmitted to, copied, or distributed, in part or whole, to any other person or the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purposes and may not be used or considered as an offer document or solicitation of an offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting, and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed, and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions based on their investment objectives, financial positions, and the needs of a specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved) and should consult its advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products, and non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness, or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document are provided solely to enhance the transparency and should not be treated as an endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors, and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from; any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared based on information that is already available in publicly accessible media or developed through an analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the opinions expressed therein. This document is being supplied to you solely for your information. It may not be reproduced, redistributed, or passed on, directly or indirectly, to any other person or published, copied, or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country, or other jurisdiction, where such distribution, publication, availability, or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain categories of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm nor its directors, employees, agents, or representatives, shall be liable for any damages, whether direct or indirect, incidental, special or consequentially including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth