Click here to download the report

Midcap Company in the Telecom Service Sector

TATA Communications (“the Company” or “TATACOMM”), with a market cap of around Rs.30,250 crores, is a leading Digital Infrastructure Provider that drives the digital transformation of multinational enterprises and communications service providers. The Company provides integrated services and solutions including connectivity, security, mobility, and the Internet of Things (IoT).

The enterprises that the Company serves include more than 5,000 Enterprise customers globally along with corporate clients who are seeking value-added services. The Company also serves more than 2,000 communication service providers globally including Airtel, Skype, etc.

The data business is mainly driving the Company’s revenues with voice business riding as a pillion. The Company offers international data and voice transmission service, internet services, bandwidth on the undersea cable system, and various other services. In addition to this, the Company has 2 ‘core’ subsidiaries and 58 other subsidiaries spread out across various counties. Its 2 core subsidiaries are:

a) TATA communications Payment Solutions is an ATM network subsidiary

b) TATA communications Transformation Services support global service providers

The Company claims to connect businesses to 60% cloud giants globally and has the largest wholly-owned subsea cable network across the globe.

The company offers two core services namely Data and Voice. The details about the data business include:

How it all started?

Videsh Sanchar Nigam Limited (VSNL) was formed in 1986 as a public sector enterprise to provide overseas communication services. Between 1999 and 2004, major disinvestment steps were taken by the Government to raise capital, to minimize the fiscal deficit. So the Government made strategic disinvestment by selling a 25% stake in VSNL to the TATAs. In 2002, TATA acquired a controlling stake in the Company, and on 13th Feb 2008, VSNL was completely acquired by the TATAs and was renamed as TATA Communications.

Information and Communications Technology Industry

- The Indian economy is gradually shifting towards a digital-based economy. As per the National Association of Software and Services Companies, the technology sector is expected to be valued at around $191 billion as of FY20. With the increasing adoption of digital technologies and the creation of digital infrastructure, this value will increase over time. It is also predicted that the Digital India plan will boost GDP by creating significant value in areas like government services and the job market, by up to $1 trillion by 2025.

- Organizations are adopting the latest technologies like IoT, cloud, Artificial Intelligence (AI), advanced data analytics which helps them to reduce cost and increase operational efficiency. Most of the organizations have shifted their IT system to the cloud as a part of their digital strategy.

- As per McKinsey report 2018, after Indonesia, India is digitizing faster among all the mature and emerging economies in the world and there remains room for plenty of growth. Businesses are adopting platform business models and digital strategies in order to remain relevant and competitive in their respective businesses. Platform models are the models in which professional activities are carried out using online platforms like Uber, Airbnb. If telecommunication companies (telcos) want to stay relevant in the ‘platform era’ then API (Application Programming Interface) has become a necessity. API is generally defined as the interaction between software intermediaries. One prominent example of API usage is the ‘login using Facebook/Google’ that is present on many websites. Without actually logging-in to users’ accounts, this function authenticates the user through APIs of these platforms for using their app.

- Internet of Things- In simple words, it is the interaction among internet-connected objects to collect and exchange data. IoT connections are expected to reach almost 25 billion connections globally by 2025, according to a report by Global System for Mobile Communications (GSMA) whereas, in India, IoT market size is expected to reach 20 billion by 2024.

- Data is the new oil. One of the key concerns of any organization is to protect and secure the data that they access. As a result, there’s an emergence of new technologies like Blockchain. Telecom Regulatory Authority of India (TRAI) has directed telcos to use blockchain technology. This will ensure that only registered telemarketers have access to the phone databases and this would reduce the number of spam calls and unwanted messages.

- As of 2019, the global telecom market stood at $1.74 trillion. Due to the large population, India is the 2nd largest telecom market after China having a subscriber base of 1.2 billion. The subscriber base is widening due to tariff reductions and increased mobile network coverage.

- As per the India Brand Equity Foundation (IBEF), Government initiatives like Digital India and Smart Cities’ mission will give a push to the digital sector. National Digital Communications Policy 2018 will help in strengthening the fibre infrastructure to support new technologies like 5G, IoT, etc.

- There is an accelerated consolidation in the telecom industry due to the rapid decline in profitability. This has resulted in the consolidation of fibre assets and disinvestments across network space.

Business Model

TATACOMM helps businesses to harness the power of digital transformation via its platform and services including IoT, cloud, mobility, collaboration, security, networking, etc. The 2 key customer segments are Enterprises and Carriers (Service Providers). As margins in the enterprise segment are higher, the Company offers customized and industry-specific services to the enterprises, thus commanding premium pricing. Things working in favor of TATACOMM are support from the parent Company and Tata Consultancy Services (TCS), which helps the Company to build a wide variety of products & services and readily provides access to its customer base. The Company’s product segments include – International Private Line, Ethernet Services, Virtual Private Network, International Leased Line, Rentals, Growth and Innovation Services, Traditional Services and many more. Also, as the Company operates the largest wholly-owned subsea fibre network (underwater fibre optic cable network), it helps the Company in cost savings by providing low-cost efficient offerings to its clients in a highly commoditized market, where a large quantity of holding is through a consortium. To sustain its margins, the Company continues to diversify revenue by capitalizing on emerging opportunities without being over-dependent on one portfolio or single geography. The Company is growing its customer base and building services both organically as well as through acquisitions. Also, during the year the company has reclassified its revenue from real estate from ‘Other Income’ to ‘Revenue from Operations’. During FY20, revenue from the real estate was 168.25 crores. The company earns its revenues through lease rentals from premises given on lease.

COVID-19 Impact

‘Necessity is the mother of invention’ seems apt in today’s world where COVID-19 has forced organizations all across the globe to shift and adapt their business models to new levels of efficiency, productivity, and secure customer connectivity. As per International Data Corporation’s COVID-19 impact on IT spending survey, 64% of the organizations are estimated to increase the demand for cloud computing, and 56% for cloud software. Needless to say, cloud services are among the few technologies which have been benefitted due to the pandemic. There is a complete shift in the ecosystem engagement over the past few months. More and more organizations are embracing work from home policy and to do so organizations need to augment employee and customer outreach methods with more digital tools. Cloud usage and remote collaboration have increased over the past few months i.e. from March onwards. IoT is possibly one of the most effective and viable solutions that can help in ensuring business continuity and employee safety. The Company is expected to benefit from this situation in the long run.

Differentiating Strategies

- Customized offering: One of the Company’s differentiating strategies is providing customized solutions to the enterprises which have led to sticky clientele growth.

- Investing in high return services: The Company invests in a high return on invested capital (ROIC) services which leverages its existing network infrastructure and is software-oriented so that it can transform into an asset-light model.

- Plan globally, act locally: TATACOMM hires the best talent worldwide and not region-wise which encourages collaboration, teamwork, and interdependency. Significant emphasis is placed on the reskilling of the employees in new technology fields due to which it has been able to maintain its employee engagement ranking amongst the top 10 percentile globally as per the Company’s Annual Report.

- Selective expansion: The Company focuses on expanding in selected international markets where data consumption is increasing, thus allowing the Company to record high traffic growth and revenue.

- Diversification: Over the years the Company has evolved and diversified its portfolio from being a traditional connectivity service provider to offering a wide range of IT infrastructure services. Therefore, the Company is no longer only a provider of bandwidth but also a provider of technologies.

- Developing new models: The Company constantly focuses on developing new commercial models to accommodate the changing enterprise IT landscape while optimizing operating costs.

SWOT Analysis

Strengths

- The only owner of the optic fibre cabling: In the data segment, TATACOMM’s key strength is that it owns and operates the world’s largest wholly-owned fibre optic subsea network across the globe. The Company’s global network consists of 710,000 km of optic fibre cabling (around 200,000 km is terrestrial and around 500,000 km is subsea). The Company holds a large portion of cable independently which gives it pricing and cost benefits.

- Diversified Business: TATACOMM has the largest global market share in International Long Distance voice traffic, thus making it a dominant player in the global market. However, with the advent of low-price Voice over Internet Protocol (VoIP) calling services, international voice calling is moving in favor of Internet Protocol (IP) based calling by Over the Top (OTT) companies. As TATACOMM also caters to OTT and VoIP providers like Skype, Vonage, there is no impact on its revenue as such but only shifting from one segment to another. This highlights the ability of the Company to adapt to the changing scenario and diversify into new areas of growth.

- Affiliations with TATA group: TATACOMM is a part of the TATA group, which is one of the largest corporate houses in India. TATACOMM’s association with the TATA group helps it to access the already existing customer bases which result in a competitive advantage for the Company.

- Strong IT partner: The largest IT Company in India, TCS, is TATACOMM’s strategic IT partner which helps the Company to build new products and services thereby increasing its operational efficiency.

Weaknesses

- High Debt: Telecom Industry is a capital-intensive industry. TATACOMM requires an extensive network infrastructure to provide fixed-line and wireless services. To fund its requirements, the Company takes heavy debt. Also, the Company requires leverage to upgrade its network to increase the capacity as the traffic increases.

Opportunities

- Increasing demand for cloud-based services: The demand for cloud computing services worldwide is increasing and the pandemic has given it an extra push. As per Deloitte, the cloud industry has grown at a CAGR of 24% from 2017-2019 and this figure is likely to be surpassed during 2020. Demand for cloud-based services has surged recently on account of the lockdowns which has increased dependency on apps like Zoom, Skype for videoconferencing, virtual schooling, etc.

- Poised to benefit from the growing telecom market: India is currently the world’s second-largest telecom market having a large subscriber base. Tariff reductions and increased smartphone penetration have driven the demand for the same.

- National Digital Communications Policy 2018: It will help in driving the growth in the sector by strengthening fibre infrastructure and supporting emerging technologies like 5G, IoT to improve the connectivity, establish a comprehensive data protection regime for digital communications and to address the security issues relating to encryption, etc.

Threats

- Growing Competition: OTTs like Amazon, Microsoft, Google, etc. are entering and growing in the conventional telecom space with cloud and network offerings. These tech giants are competing with operators for business and customer relationships. System integrators are companies that build a computing system by bringing together various component subsystems. The Company is also competing with conventional telecommunication players for overseeing customer relationship, as the Company continues to expand its managed services portfolio.

- Risk of losing customers: With the market restructuring and consolidations of carriers and service providers taking place, there’s a risk of losing key customers.

Michael Porter’s 5 Force-Analysis

Barriers to Entry

- The barrier to entry is high due to stringent government and legal regulations that the firms need to follow.

- A huge amount of licensing fees is charged which can deter new players from entering unless they have deep pockets.

- The cost of setting up the infrastructure is too high discouraging new players from entering.

- Rapidly changing trends and technologies in the telecom industry mean companies have to cope with the trends by spending a hefty amount which might be difficult.

Bargaining Power of Suppliers

- TATACOMM suppliers are mainly initial device producers and network equipment suppliers. They can affect the Company’s supply chain cost, efficiency, etc. Increasing standardization and commoditization of network components has led to increased competition among the suppliers. Overall, the bargaining power of suppliers is low to moderate. For example, an individual hardware supplier moderately influences the strategies of the Company.

Bargaining Power of Buyers

- Buyers have access to high-quality information about products in the market. This makes the bargaining power of buyers high based on variables like the client’s ability to evaluate and compare the services.

Rivalry among Competitors

- There is not much product differentiation because the products of rival firms are similar in certain ways, especially regarding their cloud services. Earlier, TATACOMM (VSNL) was a monopoly in India in the international long-distance market but now it operates in a monopolistic market where product differentiation plays a key role.

- High exit barrier, which includes high setup cost of infrastructure, discourage established players from leaving the market, making competition high.

Threat of Substitutes

- Due to the exposure to intense competition in the voice segment, income has declined as a result of lower demand and realization. It was further aggravated due to consolidation in the telecommunication industry which has led to the exit of small players.

- The low differentiation between the services provided by the telecom industries has resulted in the services being treated as a commodity. Customers can easily switch to the substitutes which offer the same products. Hence, the threat of substitutes is high.

Branding and Other Initiatives

- TATACOMM was certified as a great place to work in Canada, Hong-Kong, India, and the United States. Its inclusive workplace policies and high-performance culture makes it an excellent employer.

- The Company has branded itself as a best-in-class digital enablement service player. TATACOMM was the official connectivity provider of Formula 1 and Mercedes-AMG Petronas till the 2019 season end.

- TATACOMM being a technological service provider relies on online media marketing and social media for its promotional services. The Company also does Above the Line (ATL) and Below the Line (BTL) promotions. ATL advertising is done to target a wider audience by TATACOMM on Twitter etc. and BTL advertising is done to cater to a niche segment.

- As a part of its CSR activity, TATA Affirmative Action Program focuses on providing equal footing to Dalits and tribals through education, employment, etc.

- The Company has raised $135000 through employee contribution this year. The Company matched this amount and allocated the total amount to Tata Communications Initiatives Trust and local NGOs in India as well as to other countries around the world.

- The Company launched Tata Communications Learning Academy to make steady progress to empower their employees. It helps the employees build the necessary skills and to stay at pace with the technological changes taking place.

- In the lockdown period, the Company has worked with foundations like Parikrma Foundation and Collectives for Integrated Livelihood Initiatives (CInI) to support the migrant workers.

Financial Analysis

- Rise in the Revenue

After heavy Capex for the past few years, the Company’s data business has now reached a sizeable scale. The Company’s consolidated revenue growth for the year was 3.33% backed by robust performance in the data business and slower than expected decline in the voice business. This increase can be attributed to the fact that there has been a surge in the conferencing traffic due to lockdown in the last few days of the quarter. The Company’s EBITDA also expanded by 19.8% during FY20 due to profitable growth in the data segment, focus on cost efficiency, one time catch up billing in its real estate business of Rs.18 crore, and the application of IndAS 116, which reclassified rental expense to depreciation expenses and finance cost. The Company expects Work from Home to be an essential medium-term trigger to upgrade its digitization experience.

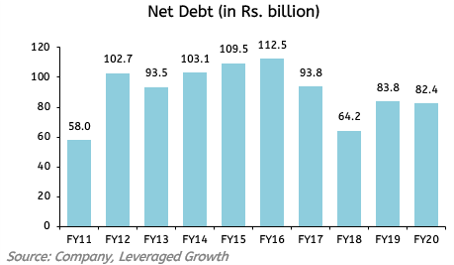

- Highly Leveraged Balance Sheet

TATACOMM’s telecom business requires huge capital involved in laying cables underneath the sea, innovation, and expansion. The Debt-to-Equity ratio for the Company is very high due to the low/negative net worth of the Company and heavy funding through debt. From 2010 till 2016, which was the peak Capex period for the Company for the asset expansion and infrastructure build-out completion, the Company’s debt increased substantially by almost 60% in six years. In the same period, its equity has continuously decreased, going negative in 2016, due to the losses. It again went negative in FY19 due to a high exceptional losses. The Company even had negative free cash flows during FY18 and FY19 due to the acquisition of an additional ownership stake in Teleena Holdings by TATACOMM (Netherlands) Besloten Vennootschap (BV). The ownership has been increased from 35.36% to 100%. This led to additional cash being spent and thus decreasing cash balances. One positive thing for the Company is that debt levels have significantly come down in FY18 mainly due to the Company selling off its stake in the South African subsidiary- Neotel and monetizing 2 of its data centres. Its interest coverage has also risen suggesting that the Company’s cash flow has improved. TATACOMM’s Net Debt/EBITDA has reduced YoY and stands at 2.8 times as of March 31, 2020, as compared to 3.1x the previous year. The long-pending land demerger has restricted TATACOMM to raise equity. The Govt. of India has apprised the Company that it is neither willing to invest in the equity nor would it want its stake to be diluted. This is the reason TATACOMM has not been able to avail any non-debt funding through the issue of equity. In August 2019, the demerger was approved by National Company Law Tribunal, which now allows the Company to raise additional equity.

- Unimpressive RoE

The Return on Equity (RoE) has not been very impressive as it has largely remained negative for most of the period. With its strategy to shift into an asset-light model by investing more in software-oriented services and with increased revenues in the data segment, this ratio will improve further. The Company’s net profit margin has been wandering in the negative region for a considerable period as the Company has not been able to clock in profits due to high expenses. TATACOMM has mainly funded its operations/expansions and refinanced its debt by taking additional leverage; no doubt it has a high leverage ratio. The Company reported a loss of Rs.85 crores on a consolidated basis during FY20 due to an exceptional charge of Rs.378.1 crore (that includes, provision towards additional license fees liability and staff cost optimization). However, EBITDA has remained positive and is on an increasing trend due to profitable growth across its data portfolio.

- Segmental analysis of FY20

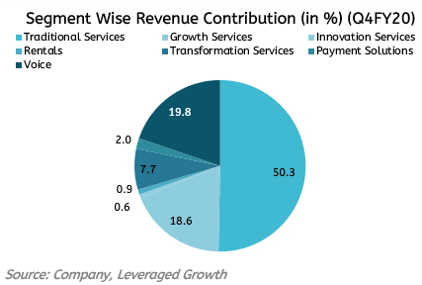

- The Company’s revenue for voice business was down by 10.9% YoY, however, the decline was lower due to higher usage during the lockdown.

- In the data segment, the Company’s revenue from traditional services showed a growth of 5.3% YoY due to an increase in bandwidth usage and IP traffic.

- Growth services also grew by 9.8% YoY mainly due to surge in the conferencing traffic at the end of the quarter.

- Revenue from transformation services also showed a growth of 14.3% YoY but the EBITDA turned negative last quarter due to an onerous customer contract and simultaneous transition of 3 large deals.

- The Company’s payment solutions business witnessed a decline of 2.9% YoY due to a drop in the average daily transactions during the lockdown.

- The Company’s revenue from Real Estate has increased YoY by 19.24% to 168.25 crores during FY20.

Risk Analysis

- Cyberattack: Security breaches can pose a severe risk to the organization- from reputational damage to loss of trust. TATACOMM could be subject to distributed denial-of-service attack which can hamper its software, hardware, and operations.

- Volatile Markets: Emerging markets are an important source of its revenue; hence any volatility or instability in the economy can affect the revenue.

- Third-Party Risk: Many of the TATACOMM products and services are a combination of Company-owned, third party owned, and open-source softwares. The Company might face claims by the third parties concerning the fact that TATACOMM’s products and services infringe their intellectual property rights (IPRs), which can damage the brand of the Company.

- Natural Risk: Any natural calamity can harm the Company’s infrastructure and even subsea networks are prone to cable cuts due to anchoring activities by humans or earthquakes which can disrupt the traffic across the global network.

- Changes in Regulations: As each country where TATACOMM operates has its own unique rules and regulations; it becomes important to identify the regulatory obligations and costs and comply with it, lest they impact earnings in the future.

Corporate Governance

- As of March 31, 2020, the Company has six directors, 1 is an executive director and the other 5 are non-executive. 2 are independent directors and 2 are nominees of Government of India. There is 1 woman director as well. This composition complies with SEBI (LODR) Regulations.

- Neither of the directors holds any share in the Company nor are they related to each other.

- During the year, one separate meeting of Independent Directors was held where independent directors reviewed the performance of non-independent directors and the board.

- The Company has a program to familiarise independent directors about the functioning and operations of the Company.

- Shares pledged by the promoters are 3.9% and total promoter holding is 74.99%.

The End-Note

- The pandemic has affected several businesses but this is one of the industries that is going to be benefitted from it. Initially, there were some delays in the execution of new projects and orders due to delay in the procurement of equipment from Original Equipment Manufacturer. However, with an increase in work from home jobs and opening up of lockdowns, the Company is expecting to return to their normal business.

- The Company already has a huge amount of debt lying on its balance sheet. Hence, taking on more debt will be imprudent so the management needs to introspect and strategize to face the challenges. The Company’s interest coverage ratio has improved slightly which is a good sign for the Company.

- With new players entering in like Reliance Jio that has partnered with Microsoft to expand its digital operations and technology in the B2B segment, we have to wait and watch to see how the established players in the telecommunications industry will respond.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Mohnish Gujral

Research Desk | Leveraged Growth