Click here to download the report

A Pioneer of Education Content Provider

S Chand & Co. (“the Company” or “SCHAND”) is involved in the business of providing Indian education content, solutions, and services across the education lifecycle. Being an organization serving for 8 decades now, SCHAND is India’s leading content provider among private publishers to Central Board of Secondary Education (CBSE), Indian Certificate of Secondary Education (ICSE), state board affiliated schools as well as unaffiliated private schools across 29 states & 7 union territories of India. Total printing capacity has enhanced from 15 tons of paper per day in FY14 to 90 tons of paper per day in FY20. The Company has been maintaining humble relationships with its authors that enabled it to grow its network of authors from 1,958 in March’16 to around 2400 in March’20.

How was SCHAND Born?

The roots of SCHAND go back to the British Raj days of the 1930s. When British Raj dominated publishing in India, books were mainly imported from England and Indian authors had little chance to see their work in print. Driven by patriotism & nationalistic fervor, a man named Shyam Lal Gupta revolutionized the Swadeshi sentiment by giving Indian authors a voice. In 1939, he published two books written by Indian authors and offered them for sale at lower than prevailing costs. This sowed the seed for Shyam Lal’s company & he set up its first printing press in 1960. Shyam Lal Gupta was awarded the “Padma Shri” in 1969. He also became a founder member-cum-the first President of the Federation of Indian Publishers, and the driving force behind the establishment of federations and associations for the Indian education industry. In 1970, Shyam Lal named the company as “S Chand and Co. Private Limited”.

Next year, the Company agreed with Maneckji Cooper Trust in Mumbai to become the exclusive publisher of the Wren & Martin titles. It then entered the school textbook market in 1976. The Company was renamed to “S Chand and Company Limited” in Sept’16 and got publicly listed on the Indian Stock Exchanges in May’17. Today, the Company is run by Shyam Lal’s grandson, Mr. Himanshu Gupta (MD). He joined SCHAND in early 2000, taking on the leadership role in 2006 after his father’s (Ravindra Kumar Gupta) retirement.

Indian Education Industry

- As per Indian Brand Equity Foundation (IBEF), the education sector in India is estimated to be around $0.144 trillion in 2020, i.e. nearly 5% of the GDP of India. According to IBISWorld market research data, it is found that the US Educational Services industry is valued at $1.4 trillion in 2021, i.e. nearly 7% of its GDP. Hence, there lies a huge scope of growth for this market in India. The global education industry is estimated to become a $10 trillion market by 2030, thereby making up over 6% of global GDP.

- The Indian education system flowchart is given below.

- As per the National Education Policy (NEP) 2020, the current public expenditure on education in India has increased to 4.43% of GDP in FY20 from 3.1% in FY10. The Centre and the States had asssured to increase the public investment in the Education sector to 6% of Indian GDP at the earliest.

- According to Union Budget FY21, the Government allocated Rs.993 billion towards the education sector – Rs.598.5 billion for the Department of School Education and Literacy & Rs.394.7 billion for higher education. It would also include Rs.30 billion towards Revitalising Infrastructure and Systems in higher education (RISE) scheme for skill development programs.

• NEP 2020 proposes to achieve a 100% Gross Enrolment Ratio (GER) in preschool to secondary level by 2030. It also aims to increase the GER in higher education from 26.3% in 2018 to 50% by 2035.

• The global online education market is projected to witness a CAGR of 9.23% during the period 2020-2025 to reach a total market size of $319.2 billion by 2025. With increasing internet penetration & lockdown across the nation, digital learning has become the need of the hour. - Pradhan Mantri Gramin Digital Saksharta Abhiyaan (PMGDISHA) scheme, that aims to provide digital literacy to 60 million rural households was approved in Feb’17. As per Union Budget FY21, Rs.4 billion has been allocated for the scheme for the FY21.

- There are over 250 million school going students in India, more than any other country in the world. An additional requirement of 200,000 schools, 35,000 colleges, 700 universities, and 40 million seats in vocational training centres, will create major opportunities for the future growth of the education sector. There is a bright future for content players & SCHAND is well-poised to ride this wave as a leader in this space.

- Since 100% FDI is allowed in the Indian education sector, the fast-growing education sector including vocational and supplementary training witnessed significant investments. In private equity (PE) and venture capital (VC) funding, companies in the education sector attracted $1.19 billion between January 2020 to August 2020 as against $409 million during the same period in the previous year. Byju’s raised $25 million, Unacademy received PE investment of $50 million & $110-million from Facebook and General Atlantic respectively. An EdTech platform Univariety raised $1.1 million from Info Edge and Classplus, a B2B EdTech start-up, raised $9 million from RTP Global are just a few examples. Reliance Industries Ltd (RIL) will be investing $210 million in two years in its allocated university, Jio Institute.

Business Model

The Company’s business model provides the entire lifecycle education spectrum for an individual. SCHAND is primarily engaged in 4 types of business segments.

As discussed above, it majorly caters to 3 categories: Early Learning, K-12 & Higher Education. The 4th segment is the digital form of content of the preceding three with new-age user-friendly technology.

- Early Learning business caters to the youngest students (0-4 years).

- K-12 segment provides content to the CBSE, ICSE & state-affiliated schools. K-12 segment is the highest revenue-generating segment for the company accounting for about 80% of the sales.

- Higher Education segment provides material for competitive exams & professional courses for colleges and universities.

The Company is associated with more than 2400 authors providing 10000+ active book titles as its raw publishing content & 5000+ pan-India based distributors and dealers. Some of the renowned authors under its brand include R.S. Aggarwal, O.P. Malhotra, Lakhmir Singh, B.L. Thereja, etc. The Company has integrated its printing needs and capabilities by setting up their factories located in Sahibabad and Rudrapur. The Company considers schools, teachers, and student customers to be the “touchpoints” or point-of-contact across all business verticals. SCHAND markets its content to educators and schools to place its products on prescribed and recommended reading lists. The number of schools in this target market is growing by 8% to 10% annually and currently covers over 40,000 schools as of Q2FY21. The business of SCHAND is very seasonal where Q4 accounts for around 80% of total revenues wherein the month of March itself accounts for 30%-40% of the annual revenues.

Subsidiaries

To expand its business, the Company has acquired 11 subsidiaries & 2 associate companies as on March’20, that function under its parent brand.

Impact of COVID-19

The Company witnessed a slowdown in school orders from early March due to the COVID-19 pandemic which impacted its FY20 revenues. Due to nationwide lockdown & schools remaining closed, the publishing book segment witnessed a washout of sales in April-May’20. The Company still has a strong order book that is yet to be fulfilled. March quarter being the peak season of sales, the management anticipates upcoming Q4FY21 sales season to be normalized and the overall FY21 revenues should benefit from the shift of Q4FY20 sales to H1FY21. To stabilize the business with online content solutions, the Company received a strong response in its digital products which offered online teaching enabled platform with live classes, e-books, teaching tools, etc. Learnflix, Mylestone & Chhaya Learning apps saw a strong subscriber addition & positive feedback during the lockdown phase.

Differentiating Strategies

- Strategic Acquisitions

For the past 5-6 years, the Company had been in a spree of acquisitions to spread its business arms across the length & breadth of the industry. As of March’20, the Company has acquired 11 subsidiaries & 2 associate company (listed above). The Company’s hallmark acquisition had been Chhaya Prakashani; a dominant player of eastern India, which itself added 771 distributors and dealers. The Company made investments in digital content makers like Safari, DS Digital, Mylestone, Edutor, etc. - Language Bank of Curriculums

The Company covers a wide foray of local language-based books. By acquiring brands like Madhubun and Vikas in FY13, the company bolstered its knowledge products in its K-12 business in Hindi language titles. In FY15, it acquired the Saraswati brand for its K-12 content strength in regional languages, art, and craft titles. - A Strong Network of Affiliated Schools

Most schools in India are affiliated to one of three main governing bodies for K-12 school: State board, CBSE and ICSE. SCHAND has its presence in around 38,000 schools across India. It is the leading education content provider in India with over 6,500 pan-India based distributors. With an increasing number of schools getting developed to accommodate new enrolment of students, SCHAND enjoys a sweet spot to expand its presence across such areas in the back of its brand image.

- Full Lifecycle Education Content Provider for an Individual

The Company has grown from providing K-12 market content & solutions to higher education as well as early learning materials. Early learning stretches over the Early Childhood Care and Education (ECCE) phase- the building blocks of a child from 0-4 years; K-12 portfolio comprises of the primary school education content between 4-18 years, and higher education content constitutes of materials for competitive & professional courses. Hence, the Company has strategically expanded to address the overall education lifecycle of a consumer. - Strong Pipeline of Online Education Market Products

SCHAND has been venturing into the digital content providing segment given online education demand since the lockdown. Focused on being a comprehensive online education content provider, it recently launched Learnflix, Smart-K & My Study Gear. Other products include Destination Success, Test Coach, Risekids, Ignitor, etc. have created a niche segment in the markets. It is also planning the rollout of ‘Educate-360’, a K-12 blended learning solution for enabling schools to conduct online classes, student assessments & e-book support during Q2FY20. This will help the Company to spread its revenue and de-risk the present business model.

SWOT Analysis

Strengths

- SCHAND has a long operating history of over eight decades. It is the leading Indian education content company in terms of revenue, titles & author relationships. Employees possess decades of rich experience in the industry, thereby giving a strong advantage of brand recall to its customers.

- The Company is the leading player in the K-12 market. It has developed multiple connections across K-12 schools. Through these, a range of brands and contents are featured on the recommended school reading lists, which allows it to sell multiple brands, titles, and subject matters. The Company also leverages its K-12 school relationships to increase revenue through cross-selling products like curriculum services, classroom management software, personalized learning tablets, and assessments.

- SCHAND has a vast network reach with national & international presence. With over 50 branches, 6,500+ distributors and dealers & 42 warehouses in India, its content reaches across the country to all the states and union territories from where it reaches out to K-12 and higher education institutions. The Company also exports its printed content to over 15 countries and digital content to countries in Asia, the Middle East, Africa, and other parts of the world.

- The Company prides itself on its library of over 2,400+ authors in the past few years. Some of the renowned authors/titles under its umbrella are – R S Aggarwal, S N Maheshwari, Lakhmir Singh, H L Ahuja, B.L. Thereja, etc. that are common household names, thereby maintaining a strong relationship with authors.

Weaknesses

- SCHAND is having a consolidated debt obligation of Rs.1.72 billion as of 31st March’20. Due to the COVID-19 pandemic, the revenues saw a sharp fall, thereby having a severe impact on its credit profile. Given the Company’s significant operating costs, profitability taken a hit and has been negative over the past 2 years.

- The Company has a very seasonal business with 80-85% of the annual revenues being generated in the fourth quarter of the financial year alone.

- K-12 is the largest business segment for SCHAND, contributing almost 80% of consolidated operating revenue. Any change in this business will impact the financials severely, thereby posing to be a weakness for the Company.

- A significant portion of revenues is derived from the titles of the top authors. The top twenty authors contributed approximately 50% of the top line. The loss of any of the top authors could adversely affect the business operations, cash flows, and financial condition posing an issue of concentration.

Opportunities

- The Government is encouraging private participation in the K-12 segment. Growth due to the shift in focus towards private schools has helped in the rise of enrolment of students. Private sector players assert on quality and hence there lies a silver lining for the private publishers to flourish.

- The Government’s goal to achieve 100% GER in preschool to secondary level by 2030 & 50% GER in higher education by 2035 means a huge number of students getting enrolled in schools. This would be a prime opportunity for the company to grow its market share & its presence in a much faster way. The Department of School Education and Literacy launched the Samagra Shiksha program with effect from 2018-19 for schools from pre-school to class 12th, aiming to provide quality education at all levels.

- The Digital Education segment is in a very nascent stage. Hence, it creates a good opportunity for players regarding the transformation of the education content industry.

- A mandate for regional variations means new content opportunities from customization with ‘local flavours’ in regional languages for adoption in schools.

- India has the world’s largest population with about 500 million people in the age bracket of 5-24 years and this provides a great opportunity for the education sector. As per Union Budget FY21, the Government proposed Ind-SAT (a standardised online proctored test) for students seeking scholarship under Study in India (SII). This will allow foreign students to arrive & study in selected Indian universities.

Threats

- The Indian market is regulated by multiple boards, including the state education boards, the CBSE and the ICSE, each of which has a separate syllabus. In the past few years, CBSE has issued a circular advising CBSE schools to use only National Council of Educational Research and Training (NCERT) print content for all classes and may issue similar advisory circulars in the future. These circulars may reduce demand for the Company’s educational content amongst the CBSE affiliated schools and, accordingly, may adversely affect the business, posing a threat of disruption.

- The Indian market for educational content is highly-competitive and fragmented with enormous content providers. Facing competition from the NCERT & State Council of Educational Research and Training (SCERT), which publishes books for the K-12 market at subsidized costs, would require SCHAND to reduce & price the products competitively and provide purchasing incentives to the customers. Failure to do so may result in the reduction of the Company’s market share and sales.

Michael Porter’s 5 – Force Analysis

Barriers to Entry

- The big players in the industry have a strong relationship with a large network of authors with 10,000+ titles published & sold every year. Any new entrant would possibly have to bear higher royalty costs with authors, thereby facing a major challenge in the industry.

- The Central Advisory Board of Education (CABE) is the apex advisory body responsible for Central (CBSE) & State governments while the Council for the Indian School Certificate Examination (CISCE) regulates the private board of secondary education in India. As per guidance, the school authorities assign the reading list of books to trusted publishers, thereby creating a barrier itself to new entrants.

- Printing & publishing requires land acquisitions & machinery setup involving significant capital infusion. Manufacturing capacity optimization is also required to maintain robust inventory levels. With the advent of digital age education, sufficient investments are also required to provide online content & solutions.

Bargaining Power of Suppliers

- The printing & publishing business is highly dependent on its authors. The companies might negotiate with the authors, but the final decision is upon the authors whether to stick to its predecessor or move into new deals with other publishers. Hence, the Company has a low bargaining power on its authors.

- The industry remains vulnerable to paper price fluctuations due to volatility in wood & fibre prices as well. The Company has been entering into digital content solutions to reduce its dependence on paper-based products.

Bargaining Power of Buyers

- CBSE board has been instructing to use only NCERT print content, thereby making parents & children choose the same over other publishers. Such instructions in future would reduce demand for the Company’s educational content amongst the CBSE affiliated schools, thereby giving higher bargaining power to buyers.

Rivalry among Competitors

- NCERT & SCERT publish books for the K-12 market at subsidized costs. This would require SCHAND to reduce & price the products competitively and provide purchasing incentives to its customers, taking a hit at profitability.

- Rising upstarts like Byju’s, Unacademy, Vedantu, etc. in digital education content had been growing at a rapid pace in the industry. With lockdown in India since March’20, digital platforms have been the only source of media for education, thereby making the market highly competitive.

Threat of Substitutes

- The unorganized & independent second-hand book market with recycled books being sold at a reduced price poses a challenge for the Company. The second-hand markets in India had been capturing prime locations to sell its products like College Street (Kolkata), Avenue Road (Bengaluru), Nai Sadak (Delhi), etc. to take away major potential customers, thereby posing a threat of substitution.

- Self-publishing of books in E-book format has been showing an increasing trend. The traditional problems in print publishing like getting the contract, distribution uncertainties, promotions, etc. are very time consuming, which can be overcome by self-publishing. Moreover, the royalty benefits are higher & it also gives an entrepreneurial feel to the authors. The biggest players in the market are Amazon (Kindle) and Flipkart (Kobo), while there are also Indian start-ups like Pratilipi, Matrubharti, Juggernaut, etc. providing a platform for self-publishing. The authors moving towards self-publishing mode would prove to be a threat of disruption for SCHAND & its products.

Branding and Other Initiatives

- Brand of authors

The Company holds strong & deep relationships with renowned authors under its brands. This has helped SCHAND in becoming the leading Indian education content company in terms of revenue, titles & author relationships. - Learnflix launch with Sourav Ganguly

The Company has transitioned from print into digital content and services to cater to the growing demand. It launched the Learnflix app, the all-in-one learning platform for the students in Jan’20 with a full-page advertisement in the leading journal of Times of India, & released commercials with Mr. Sourav Ganguly, as its brand ambassador. - Brand connect with learners & educators

The Company has established an imposing brand connect with learners and educators through programs like Live Tour demonstration of book-making at their printing destinations, connecting digitally through its own ‘My Study Gear’ app, Teacher Conclave Meet with Teaching Excellence Awards for recognizing distinguished teaching performance of individuals, 2000+ workshops, magazine publications, and global education tours. - Sampark – Monthly mailer

The Company also maintains a robust connection with channel partners through dealer meets, events, and awards along with the monthly mailer “Sampark”.

Financial Analysis

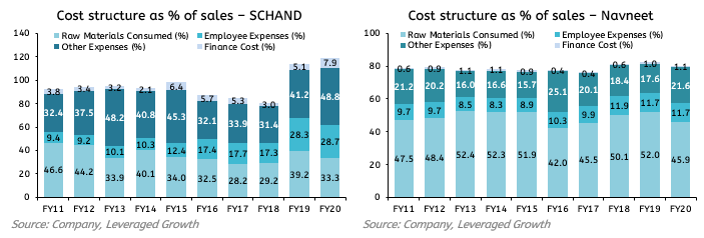

- Profitability showing De-growth

The profit margin of SCHAND is found to be very volatile as compared to its peer, Navneet Education. For SCHAND, it has been swinging from +13.3 to -25.4%, while for Navneet it has been stable around +10% to +15%.

The major reason SCHAND experienced such a slump in profits after FY18 was the cost structure of the Company as compared to Navneet. SCHAND had over-expensed beyond its revenue collection in FY19 (108.76% of sales) & FY20 (110.79% of sales). This was majorly because of high levels of sales-return (40%) on a YoY basis from the distribution channel and higher provisioning on revenues on the back of NEP 2020. As NEP 2020 was expected to lead to a change in syllabus. It was also because of higher employee costs & advertising-cum-publication expenses due to the launch of Learnflix with Saurav Ganguly as their brand ambassador. Navneet, on the other hand, had never experienced cost structure beyond 82% of sales in any year, thereby considerably making itself more efficient than SCHAND.

- Questionable Interest Coverage

The debt-to-equity ratio of SCHAND has been falling from 0.9 in FY11 to 0.23 in FY20, showing positivity on lowering leverage. The sudden drop in leverage in FY18 was due to the high proceeds of the IPO. Meanwhile, interest coverage ratio had remained benign but dropped to -2.5 in FY19 as the Company’s profits turned negative on account of higher provisioning of revenues and higher expenses. With sales & profitability being badly hurt in the past 2 years, the Company is at critical risk of defaulting with interest coverage in a negative regime.

- Low RoE

SCHAND has been majorly showing single-digit RoE over the past 10 years, with negative returns in FY19 & FY20. While its peer, Navneet has remained stable during the same tenure. This can be attributed to the same reasons that led to unstable profits generated by SCHAND, as explained above.

- Free Cash flow to Firm (FCFF) vs Cash & Cash Equivalents (C&CE)

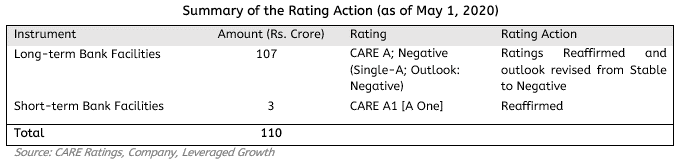

Due to its aggressive acquisition strategies to pursue inorganic growth, the Company has been incurring high capital expenditures. This has kept its FCFF in the negative territory for a major part in the last 10 years. Additionally, the Company also saw a rating cut from Stable to Negative by CARE Ratings on the back of concerns that it might face an immediate liquidity crunch, thereby leading to a default on its debt repayments in the near term.

- Segmental Analysis

The K-12 segment is the largest revenue contributor (~80% of the total revenues) followed by Higher education, early learning, and digital. The Company’s revenue distribution comprises the Indian domestic market contributing around 98% of its overall sales and overseas markets generating the rest 2%.

Risk Analysis

- Regulatory risk: For the past few years, CBSE circulated notices advising CBSE schools to use only NCERT print content for all classes and may issue similar advisory circulars in the future. These circulars may reduce demand amongst the CBSE affiliated schools. The Company also remains vulnerable to changes in the educational procurement process and changes to the syllabus and curriculum standard. Schools may also prefer to choose other curriculums offered by competitors that would impact the Company sales.

- Digital segment disruptions: Digital business where management has invested Rs.100 Crore is currently loss-making. The digital business takes longer than expected to breakeven. The business may be impacted by the rate of and state of technological change, including the digital evolution and other disruptive technologies, which could adversely affect the revenue of the Company.

- Audit Report: The audit report in FY19 states the following: “Estimates of expected future sales-returns are required to be made at the time of sale. When determining the appropriate allowance, management considers historical trends as a basis for the estimate as well as all other known factors, which could significantly influence the level of future sales returns. Significant judgment is required in assessing the appropriate level of the provision for sales return”.

Corporate Governance

- As on March’20, the Company’s Board consisted of 8 Directors: A Non-Executive Chairman, two

Executive directors, two Non-Executive directors & three Independent directors. This composition complies with the SEBI Listing Obligations and Disclosure Requirements (LODR) Regulations, 2015. - One of the executive directors, Mr. Himanshu Gupta is the son of Mrs. Savita Gupta (Non-Executive

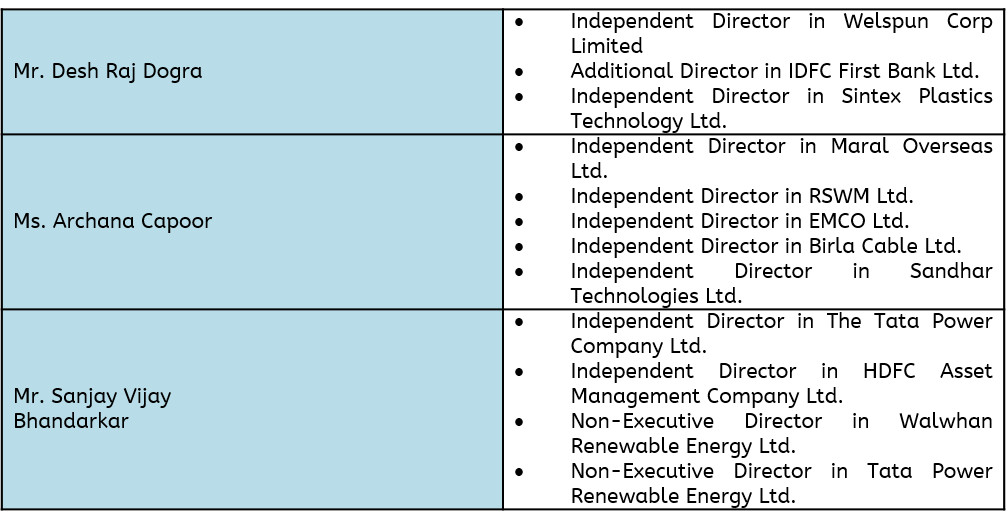

Director of Board); one of the non-executive directors, Mr. Gaurav Kumar Jhunjhnuwala is the son of Mr. Dinesh Kumar Jhunjhnuwala (Executive Director of Board). Apart from these two, there are no other inter-relationships amongst the Board members. - Directorship of Independent directors of SCHAND in other companies.

- The Board members held five board meetings during FY20.

- There is no pledging of shares by the promoters of the Company. Following chart shows the shareholding breakup of Hawkins as of June 2020.

The End-Note

- The Company saw a significant rise in its expenses in the past 2 years, i.e., FY19 & FY20, where the distributors have been returning its inventory due to potential change in the syllabus with NEP 2020 soon to come into force. High sales-returns coupled with the disruption of supply chain due to COVID-19 lockdown led to de-growth & negative margins for the Company.

- The Company’s consolidated debt stands at Rs.1.72 billion as on 31st March 2020, while it is having negative interest coverage ratio & struggling to generate cash flow from operations. Although the Company faces a huge challenge on its road to profitability under such dire circumstances, the management aims to become debt-free in 3 years.

- SCHAND’s major part of sales is attributed to trade receivables, accounting for almost 78% in FY20. With sales being washed out in early FY21 due to lockdown, it would be challenging for its distributors & dealers to pay back the same, resulting in higher write-offs & sales-returns.

- Over the past 4-5 years, SCHAND has been making a spree of acquisitions in publications as well as digital content platforms. The Company started with SCHAND 3.0 program, aiming to lower operating costs by reducing inventory and receivable levels, consolidating offices and warehouses, right-sizing of the employee base, and renegotiating royalty agreements with authors in coming years. The management anticipates that this measure will lead to improved cash flow metrics & profitability margin levels.

- During COVID-19 lockdown, Learnflix saw a very strong response with over 80,000 downloads from Google App-store & over 18,000 paying subscribers. Other digital offerings include Mylestone (around 400 schools signed up to cater to almost 1.5 lakh students) & Chhaya App (Bengali & English online learning with over 500,000+ downloads). The management is targeting to increase the share of the Digital & Services segment to 20- 25% over the next 3 years.

- Rising income of households, rising internet penetration and demand for quality education coupled with a large young population and low GER offer promising growth opportunities in the education sector in India. New Education Policy 2020, adopting changes in the present curriculum, would be greatly beneficial to the Company and the sector as it removes piracy and used book circulation. Following this, the Ministry of Education is expected to roll out the new National Curriculum Framework (NCF) by April-May 2021. Hence, schools would likely adopt the new framework books from the academic year 2022-23 onwards, thereby providing an opportunity of bright growth for SCHAND.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Debayan Saha

Research Desk | Leveraged Growth