Click here to download the report

Asia’s Biggest and Leading CRO*; Towards Global Standing

Syngene International Limited (“the Company” or “SIL”) is an integrated manufacturing, research and development (R&D) organisation, providing scientific services – from early discovery to commercial supply. The Company’s development of Novel Molecular Entities (NMEs) which are active compounds, complex, molecules [not yet approved by the Food and Drug Administration (FDA) of the United States (U.S.)/European Medicines Agency (EMA)], cater to a broad range of industrial sectors including pharmaceuticals, animal health, nutrition, cosmetics, consumer goods, specialty chemical companies, and biotechnology. The Company comprises of a team of 5,000 qualified employees as of FY20 and is supported by state-of-the-art infrastructure and market-leading technology.

The Company is headquartered in Bengaluru, India and works with clients from around the world. SIL wholly owns a subsidiary in the U.S. namely Syngene USA Inc. Providing solutions to manufacturing and R&D challenges for small and large molecules while improving productivity, reducing the cost of innovation, and speeding up time-to-market. The Company has established collaborations with the market leaders to increase its reach. SIL has also partnered with small and virtual companies, non-profit organisations, start-ups, and academic centres.

How was SIL Born?

An Indian billionaire entrepreneur, Kiran Mazumdar Shaw, studied fermentation science but could not become a master brewer in India. While she was relocating to Scotland, she met Leslie Auchincloss, the founder of Biocon Biochemicals Ltd. of Cork, Ireland. Leslie’s company was into the production of enzymes used in brewing, food packaging, and textile industries. He was finding an Indian entrepreneur for the establishment of a subsidiary in India and Kiran was a perfect match. After a brief period of training in Ireland, Shaw started Biocon India in 1978, in the garage of her rented Bengaluru house. With the seed capital of Rs.10000, Shaw owned 70% of the Company because the government restricted foreign ownership to only 30%.

Biocon’s initial products were Papain and Isinglass and within a year it became the first Indian company to manufacture enzymes and export them to the U.S. and Europe. Shaw established 2 subsidiaries: Syngene back in 1994 and Clingene in 2000. Seeing the synergy between the two, Clinigene was merged with Syngene. Syngene was then listed on BSE/NSE in 2015 and has a market cap of Rs.256 billion as of 31 December 2020.

The Backdrop of the CRO Industry

- The increasing pressure of regulatory compliance, higher costs, and faster innovation has forced Pharmaceutical companies and medical organizations to outsource their R&D to help lower their costs. Contract Research Organisations (CRO) Industry offers outsourced services to provide support and development to the R&D driven organisations. These organisations range across industrial sectors like pharmaceuticals, biotechnology, agrochemicals, cosmetics, nutraceuticals, animal health, electronics, and biopharmaceuticals. CRO covers the activities of R&D from NME’s development, manufacturing, and discovery.

- Historically, the growth in the CRO industry has been driven by growth in R&D spending and the increased outsourcing of R&D activities.

- The major share of the CRO market is constituted by Southern and Western India. However, recently it is seen that the CRO market is shifting to the North. This is mainly because of the shift in the concentration of the offices of the regulatory authorities like the Indian Council of Medical Research (ICMR), the lower cost, and the diversity of the genetic pool in that region.

- The Indian CRO market is expected to grow at a CAGR of 7.6% between CY19 and CY25 and touch a $61 billion market by the end of this period.

- For an industry that barely existed a decade ago, the CRO sector is performing very well compared to other industries. Many CROs have been acquired while others have gone out of business. IQVIA which dominates the CRO market, focused on mergers and acquisitions to enhance and strengthen its position in the global market.

- Owing to a constantly changing pharmaceutical landscape, the industry is expected to witness a moderate 4.0% to 5.0% growth in the next 5 to 7 years, to surpass $1500 billion by CY25. Market participants in coordination with the industry growth are investing 8.0% to 10.0% of their revenues in drug discovery and development. With an overall R&D investment of approximately $186 billion in 2019, the industry is working toward developing new and innovative curative therapies as per a study by Frost & Sullivan.

- India has become one of the top destinations for clinical trials because of its large heterogeneous patient population, English-speaking western-educated physicians, and mindset of providing high-end services at low cost. All these factors have resulted in companies from western countries to put their money towards Indian CROs. Over and above, in the recent past, this has made India an outsourced destination for good quality at a competitive cost.

Business Model

A subsidiary of Biocon, SIL was incorporated in 1993 and is headquartered in Bengaluru, India. The Company has more than 360 active clients, 8 collaborations with the top 10 pharmaceutical companies, and 4,200+ scientists as of FY20. The Company generated a revenue of $0.29 billion and a PAT of $0.05 billion in FY20.

SIL offers R&D research to its clients in various fields, they also have three flexible models to offer to its clients.

- First, being the dedicated R&D labs which offer dedicated scientific and support personnel, customized and managed to partner requirements with long-term contractual commitment.

- The second model being, Full-Time Equivalent (FTE) with dedicated scientific resources selected from partner-specific disciplines, typically a ~3-year contract term ensures team continuity, adjustable with specified notice period.

- Third model being Fee For Service (FFS) which is flexible, on-demand resources with targeted skill sets which are an effective way to manage fluctuating demand, ad-hoc requests or uncertain quantity of work.

SIL offers the facility to combine any of the business models to suit the requirements. SIL focuses on being a “one-stop-shop” with integrated services to offer to its clients, and expanding their client base to animal health, agrochemicals, cosmetics, and electronics has helped the company to cross the 20,000 million benchmark in FY20. The Company’s main focus is to now shift from a CRO to Contact Research and Manufacturing Services (CRAMS).

Impact of COVID-19

The cases started appearing in the western countries way before the cases started appearing in India. This made clients fast-track their projects before the shutdown. During the first few weeks of April, certain critical services within the Development and Manufacturing areas had been operating with below 10% staff as per government mandate. There was a complete operational shutdown in the first three weeks of April. The Company gradually resumed operations from April 20, 2020. SIL was working with 70% capacity in Apri and at 90% capacity, i.e. near-normal levels since mid-May. The Company has adopted a 4-pronged strategy to battle COVID-19 which is given alongside.

The management expected a marked impact on Q1FY21 due to the Covid-19 related shutdown, which could be seen with the 19% drop in net profits and flat revenue, but the situation is better than what was expected by the Company in March.

As per management, it is expected that return to growth will take place in the second quarter, the Company has also decided not to pay any dividends for this year, to maintain its liquidity position. The pandemic had a small positive impact on the Q4FY20 because some clients accelerated work ahead of their lockdowns. However, a direct impact from complete/partial suspension of operations during May and April will be reflected in the coming quarters.

Profitability for full-year FY21 is expected to be at a similar level as in FY2020 because the management is experiencing growth in lower double-digit revenues. This growth is witnessed due to the continuous addition of clients, an extension of existing contracts, an increase in manufacturing, and biological contributions besides currency growth.

The Company’s long-term rating has been upgraded from CRISIL AA to CRISIL AA+ with a stable outlook. The short-term rating is retained at CRISIL A1+. This indicates SIL’s sound business model, strong fundamentals, and a robust liquidity position.

Differentiating Strategies

- High Recall Value

SIL has enjoyed high recall value because of the integrated services it provides and also because of its consistent performance and high data integrity ethos. This is reflected by the fact that 8 out of the top 10 clients have been engaged with the Company for the past 8 Years. The Company has also set up centres for its three major clients Bristol-Myers Squibb Co (BMS), Abbott, and Baxter. The main reason for such high recall value which is present in the industry itself is because CROs tend to have a broad range of integrated capabilities enabling clients to deepen and strengthen their engagement across multiple services. Over the years, it has also been observed that SIL has been using the foot-in-the-door (or FITD) technique to its advantage, and has also been able to attract new clients using the same. This technique aims at getting a person to agree to a large request by initially having them agree to a small/ modest request. The contract with Baxter which started as an FFS has now been upgraded to a dedicated R&D lab. The focus on targeted client engagement including personalized project managers along with the opportunities to establish dedicated centres to meet clients’ long-term development and manufacturing requirements has done well to the Company.

- Increasing Clients; Reducing Revenue Concentration from Top 10

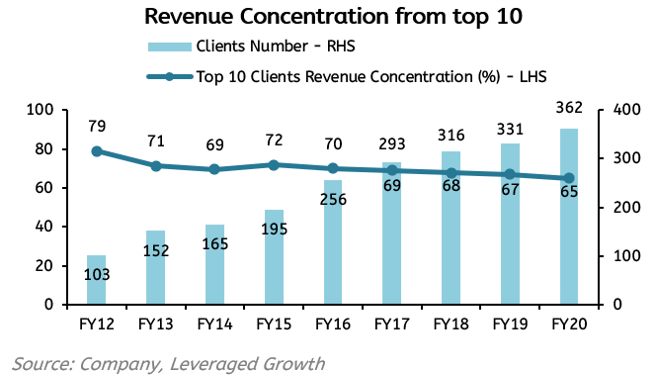

SIL’s clients have increased from 256 to 362 in 5 years, which is an absolute increase of 41%, and it has also been successful in decreasing the revenue concentration from the top 10 clients from 70% to 65%. This is because of the commercial approach to target new clients. SIL has also introduced an “Instatour” virtual feature for its prospective clients to visit their state-of-the-art facility virtually.

- The Varied Business Model with Cost Advantage

The Company has always believed in offering world-class facilities to its clients, with the help of its state-of-the-art facilities, best scientists, and ensures completion of existing contracts with the help of dedicated R&D labs, FTE, FFS and the flexibility to combine any of the above to tailor the specific requirement of the clients. SIL’s billing rate of cost per scientist is around $60000-80000, which is much lower than all the other global peers, whereas it is close to $90000-100000 in China and $200000-240000 in the US. This proves to be a direct advantage for its customers in terms of costs. - SIL’s Employees are the Backbone of the Company

SIL harnesses the power of science and serves its clients because of the Company’s knowledge, scientific skills, and innovative capabilities. During the year, 475 new employees joined the workforce, taking the total headcount to 5000 as on March 31, 2020. To ensure that the workforce is aligned to the corporate goals, ethos and culture while matching the pace of change and scale of expanding operations, the Company invests extensively in staff training and development programs across all levels of the organization.

- Excellent Compliance Record

Over the past four years, SIL has successfully cleared seven USFDA audits of their facility and has an excellent track record in terms of compliance. It has also cleared The Pharmaceuticals and Medical Agency (PMDA) audit which was conducted in response to a regulatory filing by one of their clients to support the planned launch of a new product in the Japanese market. PMDA is considered by many to be one of the most stringent regulatory bodies in the world. This has helped the brand to maintain a credible rating in the global market and get worldwide recognition. As per a survey by Pharma IQ, 65% of voters considered lack of quality as a reason to discontinue their partnership with CROs, a popular method is to check the number of inspections passed without any observations. SIL has had an excellent track record in this regard.

SWOT Analysis

Strengths

- World-Class Infrastructure and Processes: The Company has world-class infrastructure and processes which is in compliance with the quality standards to serve international markets. The Company’s audits are successful by regulatory authorities such as FDA and EMA. This provides the Company with a sustainable competitive advantage. The Company ensures operations of laboratories and manufacturing facilities to high standards in order to reassure consistency with global clients.

- Talented and a qualified pool of scientists along with an experienced management: The Company possesses a qualified pool of more than 4200 scientists. SIL recruits scientists from India as well as overseas. Significantly Indians studying outside and gaining experience are the major recruits.

The management is very experienced, having a median of 20 years of experience across global clinical research, pharmaceutical, and life sciences industries. A significant increase in the Company’s revenue and earnings is because of the management team leveraging their deep knowledge and wide network of industrial relations. - Integrated Service Offering Across Multiple Domains: A proven track record of successful delivery, reliability, cost-efficiency, and client satisfaction is because of the integrated service offering by the Company. SIL has built significant credibility and a regulatory track record in various therapeutic platforms and service models. The Company’s operational track record is the successful delivery of projects, process innovation, turnaround times, responsiveness, and productivity which has caused the strengthening of the client base.

- Attractive and Diversified Client Base: The Company has a diverse client base and several top client collaborations. SIL has extensive and longstanding relationships with multinational companies like Baxter, Merck & Co., and BMS. The Company also collaborated with mid-size companies like Achillion Pharmaceuticals, Inc., Aquinox Pharmaceuticals Inc., and Saniona AB. SIL strives to strengthen relations by providing services that are at the pace with the Company’s clients.

Weaknesses

- Terminable Contracts: The Company’s contracts are generally terminable without cause upon 60-90 days’ notice by the client. Any delay in the renewal or the termination of a large services contract could adversely affect the Company’s revenue and profitability.

- Dependence on Outsourcing: The Company will be affected by the fluctuations in industries like pharmaceutical, biotechnology, agro-chemistry, consumer health, animal health, and cosmetic companies because of SIL’s dependence on the outsourcing of R&D.

- Dependence on Clients: The Company depends on a limited number of clients, and a loss of or significant decrease in business from them could affect the Company’s business and have a material impact on SIL’s profitability. However, the Company is working on this weakness and widening their client base.

- Increase in Employee Benefit Expenses: The Company expects its employee benefit expenses to increase with time and if they do not cap it, they will lose significant revenue as they may not be able to pass such costs on to the Company’s clients.

Opportunities

- Increasing Role of CROs in the R&D Value Chain: Healthcare CROs are playing an increasingly valuable role in the industry value chain, contributing at different stages throughout the drug discovery and development process. With the industry maturing, the R&D service providers have also tasted the scientific experience, newer technological capabilities, and the expertise to navigate regulatory capabilities. CROs are serving as partners in innovation because of their exposure to the scientific expertise and therefore, the CROs are serving as partners in innovation while delivering a broad spectrum of their clients’ early-stage research needs, promoting cost-efficiency, and reducing time to market for a drug.

- New Therapeutic Approaches: New opportunities have come up in the CRO industry because of advancements in drug R&D. This is resulting in a surge in biologics and other complex therapies such as cell and gene therapies (CAR-T therapy), growth in therapy areas like immuno-oncology, rare diseases, neurology and increasing demand for personalized medicines and treatments for specific diseases.

- Strategic Partnering: Due to the rise in the CRO engagement in different stages of discovery and development, strategic partnerships with clients are becoming more common. Both the parties invest in projects and with the profitability of the project they gain long-term relationships as well.

- Cost Saving with Outsourcing: R&D service providers (CROs) can help innovator companies minimise investments in capital-intensive in-house facilities and convert fixed R&D expenditures into variable costs, thereby enabling them to balance investment risk.

Threats

- Government Policies: The Government policies are subject to change at any point in time which may act in favour of or against the Company. Government policies for the CRO industry are developed in consultation with the CRO industry, over time. Approval for clinical studies is being provided by the Drugs Controller General of India (DCGI).

- Competition in the Industry: Entry of small companies have created tough competition for the already existing firms. However, venture capitalists are providing funding to the firms and there are many mergers and acquisitions taking place in the industry thus making it more challenging.

- Training of New Entrants: The new graduates and post-graduates of pharma, medical and life science need to be provided with training according to Good Clinical Practice (GCP) and other regulatory guidelines to keep them updated about the industry. This can cause additional costs for the Company and to stay in the competition, the Company needs to cut its costs.

Michael Porter’s 5-Force Analysis

Barriers to Entry

- The CRO business is highly regulated in terms of the compliances in the form of audits by health agencies. To understand how some pharma companies struggle to meet the required USFDA requirements, let’s take a look at the example of Wockhardt where the FDA added Wockhardt’s bulk manufacturing plant in Ankleshwar, India, to its import alert list, joining plants in Waluj and Chikalthana that the FDA banned in 2013. This led to the fall in exports to the US which resulted in the loss of around 50% of its revenues to the US. Seeing how a popular name in the pharmaceutical sector struggles to clear the inspections, it’s not only commendable on the part of other companies clearing the inspections but a challenge for new companies willing to enter the business. Therefore, the barrier to entry is high.

- The investment that is required in terms of having the latest infrastructure comes with a huge Capex requirement, hiring the best talent in the industry comes with a huge cost, as the HR is the real asset for the company. Therefore, it is expensive for the new players to enter this capital intensive industry.

- To fund Capex requirements companies can raise money from banks and other financial sectors, which increases the debt component on the company and further increases the pressure on its profitability margins. It is a big challenge for the company to continue its Capex operations and ensure profitability at the same time.

Bargaining Power of Suppliers

SIL has a dedicated team of Supply Chain Management (SCM) professionals who have the expertise and experience to work closely with their global supplier base to ensure timely delivery of supplies while making sure that there is strict adherence to quality and regulatory compliances. This SCM team works on 4 fronts- Procurement, Logistics, Commercial and Inventory Management. This allows the Company to drive operational efficiencies and have an upper hand over its suppliers. Therefore, the bargaining power of suppliers is low.

Bargaining Power of Buyers

The bargaining power of the buyers is moderate, as the majority of the clients are in the west, and the clients in the west are only used to a 2-3% inflation. Therefore, a sudden increase in the price is not feasible. But because SIL has placed itself competitively on the cost front at the global level, it has a little headroom to pass the increase in rates or other expenses to its clients.

Rivalry among Competitors

With few CROs in India and a major concentration of CROs in the US, the competition is more global than domestic. The competition in the industry is fragmented but a global innovator only chooses 2-3 top vendors for the research, this leads to molecule consolidation in only the hands of a few players. Also, the CRO marketplace is becoming competitive day by day. There is a trend of mergers and acquisitions which is intensifying larger companies’ full-service capabilities and international reach. Other CROs which are mid-sized and small are giving a more personalised approach to their sponsors by focusing on the niche sectors. IQVIA, currently the largest CRO in the world, has a revenue of more than $10.4 billion and is further acquiring smaller specialist companies. This is strengthening IQVIA even further.

Wuxi Apptec, a Chinese peer of SIL has managed an exponential growth in the last few years. Wuxi has slowly evolved from a CRO to a CRAMS organization. This has allowed them to provide an integrated solution. For example, if a global innovator gets into molecular research discovery; it is highly probable that the contract is further extended to the same company for the manufacturing of the molecule, as it also helps in reducing the lead time to the market for the innovator and saves them the cost of shifting. Therefore, it can be concluded that there is a tough rivalry among competitors.

Threat of Substitutes

According to a survey by Pharma IQ, it was reported that 65% of the voters considered lack of quality as the main reason a company decides to end a partnership with a CRO. Therefore, when selecting a CRO to outsource its operations to, the quality of service plays a crucial role, along with the reputation and level of expertise. Therefore, a client is more likely to end a partnership with a CRO over lack of quality than the costs involved, because the company is already saving the higher costs by outsourcing its R&D operations. Hence, there exists a moderate threat of substitution.

Branding & Other Initiatives

- ‘One-stop-shop’

SIL offers flexibility in terms of its revenue model, dedicated R&D centres, FTE and FFS and the option of combining any of the above just to tailor the requirements of its clients. Therefore, branding itself as a ‘one-stop-shop’ for its global clients. - International Recognition

SIL has been recognized at the international front for its best practices and scientific capability. The Company was considered one of the top 25 fast-growing business in India, received the runner up award for the Best CRO at the international front, recognition at the CMO Leadership Awards 2019, received the Utthama Suraksha Puraskar 2019 by the National Safety Council of India (NSCI) and a lot more. - ‘Kavach, Safety Initiative’

Kavach is a safety initiative adopted by the Company, and its focus on safety and sustainability has helped it win the ‘Safe Workplace Champion Award’ at the 8th Manufacturing Supply Chain Summit and Awards organized at Mumbai. The Manufacturing Supply Chain Awards recognizes individuals and companies who have excelled in manufacturing, technology, innovation, safety and logistics. The Company was also presented with the FICCI CSR Award. This award was given for environmental sustainability for the Company’s efforts to rejuvenate the Hebbagodi Lake in Bengaluru and for making it an oasis for the local community.

Financial Analysis

- RoE and RoCE

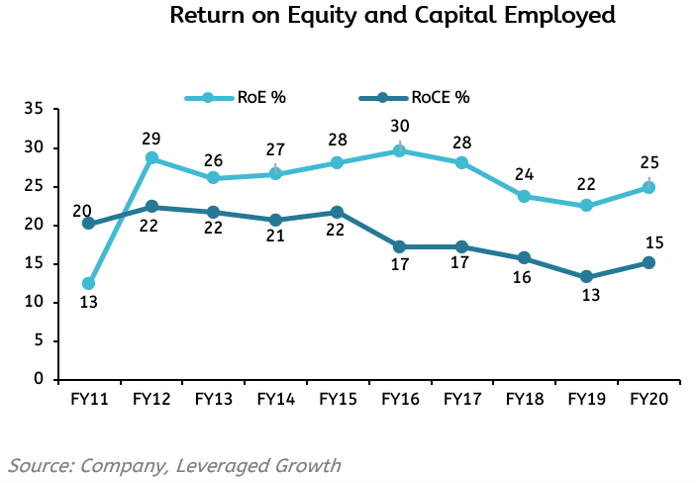

A gradual decline in RoE between FY15-19 was mainly due to higher interest costs, lower other income and a higher tax rate. RoE and RoCE seem to be improving in FY20 due to increasing income from other sources, and a marginal dip in total expenses which has led to better returns and henceforth an improvement of 1.9% from FY19-FY20. The figure of RoCE for FY20 is depressed because of the upcoming API facility in Mangalore. As the CapEx of the business model is front-ended, utilization of the $0.1 billion facility will take place after 24-36 months of operation. The facility is set to start by the end of FY21.

- EBITDA and PAT

SIL has been doing a steady business over the last few years; it has ensured a positive increase in revenues, PAT, and EBITDA. SIL’s EBITDA grew by 14% in FY20 to reach $0.09 billion as compared to $0.08 billion in FY19. This increase in EBITDA in FY20 is driven by lower material costs, foreign exchange fluctuations which were favourable, and lower growth in other expenses arising out of ongoing efforts to minimise cost which were partially offset by an increase in employee cost. EBITDA margins had improved and reached 33.6% in FY15. This was mainly due to an increase in productivity and orders. A decrease in the margins from FY17-19 was on account of a fire that took place in FY17, this affected ~10% of the total revenues for the Company, that ended up hurting the profits of the Company too. However, SIL remains a cash-rich and fundamentally strong Company, with increasing global traction. Despite all the challenges, the Company was able to maintain 30%+ EBITDA and decent PAT in the upper 10s over the last few years. The Company’s PAT for FY20 was $0.04 billion. The EBITDA and PAT margins also improved during the FY20 by 1.22% and 0.1% respectively.

- Tax Rate: SEZ benefits Soon

SIL has establishments in SEZs. SEZs are places of business interest which have different rules and laws to attract businesses and promote the local economy. SEZs have a 5-year tax holiday benefit, however, the facilities which were established earlier in these areas started witnessing the unwinding of such benefits, which resulted in the increased tax rate, and impacted PAT.

The Mangalore Facility which is to be commenced in FY21 is established in an SEZ area, it comes with a 5-year tax-holiday benefit, which will help in the relaxation of the tax rate for the Company, which is going to be profitable for the company in the future.

The Company’s export services are now exempt from GST because of the law that came out in September 2019 which states that there is a provision of exemption on the export of Toxicology, Analytical, Stability, and Clinical Services. This has benefitted 10% of SIL’s business.

- Debt: Actively Reducing

SIL had zero debt back in FY13, but the company had a 0.85 Debt- Equity ratio in FY18, this was because of an External Commercial Borrowing (ECB) loan of 0.1 billion dollars raised by the company to fund its Capex targets. The Company has actively reduced its debt since then, bringing it to 0.14 in FY20 as compared to 0.28 in FY19. The Company is ensuring a low Debt-Equity ratio whilst meeting the desired CapEx targets.

Risk Analysis

- Foreign exchange risk

Major revenues of the Company are earned in U.S. dollars and there are certain costs that are also incurred in U.S. dollars. Hence, since the Company has exposure to foreign exchange risks, fluctuations in the exchange rate could cause a financial loss. This risk is hedged with the help of ‘Put options’. ‘Foreign exchange future’ risks are being managed by hedging between 50% and 100% of exposure over the coming 24 months and up to 100% of exposure for long-term fixed-price contracts. - Business development risk

The inability to add more clients and enhance business can cause opportunity loss, leading to business stagnation and a decline in return on investment from assets. The Company is increasing its investments in building a strong commercial organization to target new clients. The Company has even reduced the revenue concentration from the top 10 clients from 70% to 65%. - Information Technology risk

Contract research involves working on novel technologies, therefore, maintaining data confidentiality and security held in digital form is critical. This data is prone to cyber-attacks and security breaches. Moreover, the COVID-19 crisis has made work from home a compulsion for all the employees, which makes it necessary for the Company to adopt better and latest IT methods to safeguard its critical information. - Health and safety risks

The nature of the Company’s business may cause significant injury to employees or loss of infrastructure in case of lack of adherence to health and safety standards. In FY17, one of the facilities caught fire and this resulted in the damage of the facility, although no life was lost in the incident, approximately 10% of the entire revenue was affected. The company after the incident took health and safety risk measures seriously and decided to launch ‘Kavach’ – a corporate safety initiative that aims to institutionalize a culture that is strong and safe among all employees and making sure that it has the right safety systems and processes in place. - Political risk

The Company’s operations are vulnerable to change in policies due to protectionist measures, therefore, changes in government regulations and outsourcing policies may impact the client’s outsourcing plans. The majority of the revenue is generated from the clients in the US which results in reliance over a specific area.

Corporate Governance

- The SIL Board members possess qualities such as research and innovation, finance and risk management, compliance and governance, scientific knowledge, global healthcare services, and manufacturing to name a few.

- The Company has an appropriate mix of Executive, Non-Executive, and Independent Directors. As on Q4FY20, the Board comprised of 10 board members out of which 4 are women. There are 6 independent directors, 2 Non-Executive and 2 Executive Directors.

- There were 5 board meetings held during in FY20. The gap between any 2 board meetings did not exceed 120 days. There was one independent directors’ meeting in Q4FY20 on 22nd January.

- John Shaw and Kiran Mazumdar Shaw are husband and wife and Prof. Catherine Rosenberg is the sister-in-law of Kiran Mazumdar Shaw, except for the above; there are no Interrelationships among the other directors.

- None of the directors serve as a Director in more than 7 listed companies. Directorship of Independent Directors of SIL in other companies:

a) Vinita Bali is an independent director at Cognizant Technology solutions ltd

b) Sharmila Abhay Karve is an Independent Director at Vanaz Engineers ltd, Vessel Propack Ltd.

c) Vijay Kuchroo is an Independent Director at Biocon Ltd, Biocon Pharma ltd.

The End-Note

- The Company has seen an increase in the revenues at a CAGR of 20.55% from FY11-FY20, this is due to an increase in the total number of clients being served, and the signing of long term contracts with their existing clients.

- A temporary setback in earnings, margins, and RoE could be seen due to the fire in one of the facilities back in FY17. The Company after the fire, launched a safety initiative by the name of ‘Kavach’ to establish better safety norms and ensure business continuity, there was an improvement in the margins in FY19-20.

- SIL has also repurposed one of the labs to set up an RT-PCR based COVID-19 testing laboratory. This facility has been approved by the ICMR. They have also collaborated with Pune-based Mylab Discovery Solutions to supply reagents for use in their indigenously developed testing kits, with the help of their large-scale oligonucleotide facility and repurposed to support the manufacturing of these reagents. Gilead Sciences Inc and SIL have signed a pact for the manufacture and sale of its drug called Remedesivir. This drug is antiviral and has shown improvement in the Covid-19 trials.

- There is a lot of potential in the sector, as this entire sector is based on innovation and how a CRO can reinvent itself, and offer superior products to its clients. Wuxi Aptech, a leading name in the CRO sector in China has been able to grow at a rate of 30% in the last few years, thanks to their Biologics Division. SIL has been fast to adopt the same to offer the same service to its clients at affordable prices. Although SIL does not share its revenue details segment-wise, the Company claims the contribution from the biologics is decent and is set to grow in the future and be a major contributor in revenue. The CRO sector is closely related to the Pharma sector and other chemical sectors, seeing the current trend in these sectors, it has made everyone curious about their future performance.

- The Company intends to evolve from a CRO into a CRAMS organization with commercial-scale manufacturing capabilities.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Rashi Kajaria

Research Desk | Leveraged Growth