Click here to download the report

Sustainability Starts Here!

Praj Industries Limited (“the Company” or “PIL”), with a market cap of Rs.2115 crores is headquartered in Pune and is one of India’s most successful companies in the field of bio-energy. It is a leader in the engineering business, water, and wastewater treatment solutions with its presence all across India, Thailand, USA, South Africa, and the Philippines. The Company started as an entrepreneurial venture of Mr. Pramod Chaudhari in 1985, initiating its operations in the agriculture-based process industry as Praj Counsel Tech.

About the Founder, Mr. Pramod Chaudhari

Pramod Chaudhari, a techno-entrepreneur developed the Company into a world-class engineering firm specialized in agri-processing opportunities. With a strong belief in the principle of triple bottom line which focuses on People, Planet & Profit, he developed a business model that is inherently scalable, replicable, and sustainable.

He has been deeply passionate about bio-economy and the environment and has committed himself to develop clean and green technologies through PIL’s varied initiatives. As a champion of the powerful premise that “Innovation and Entrepreneurship can change the world for better”, he has been a tireless crusader in propagating the spirit of entrepreneurship and intrapreneurship.

Pramod is also an alumnus of Harvard Business School (AMP 1995) and a ‘Distinguished Alumnus of IIT Bombay’ (1971).

PIL’s Journey

PIL embarked upon its journey in 1985 and began its operations in the agro-based process industry as Praj Counsel Tech. After 2 years of operations, it received capital support from ICICI (now ICICI Ventures).

PIL launched its Initial Public Offering (IPO) in 1994 and parallelly forayed into international markets, specializing in South East Asian markets. The Company also entered the South American Markets in 1999. Currently, PIL has footprints in over 75 countries, across five major continents and remains India’s biggest biofuel technology company.

Indian Engineering Sector

- India’s engineering sector is split into heavy engineering and light engineering. The capital goods industry in India is expected to achieve a turnover of Rs 8.05 lakh crore by 2025.

- Production cost, market knowledge, technology, and creativity has been the comparative advantage of Indian engineering firms with regards to its peers and has been the thrust behind engineering export from India.

- According to a press release by Piyush Goyal, the govt. will make all efforts to confirm that the export of engineering goods reaches $200 billion by 2030.

- The Government has also announced to produce funding of ₹100 lakh crore in infrastructure over the next five years.

- An allocation of loans of up to ₹1 crore for MSMEs within 59 minutes through a committed online portal has also been proposed by the Government. A total of ₹350 crores has been disbursed to MSMEs under the Interest Subvention Scheme in FY20. The scheme provides for an interest relief of 2% per annum to eligible MSMEs on their outstanding fresh/ incremental term loan/ working capital during the period of its validity. The Government has introduced such schemes to incentivise and subsidise the major contributors to the growth of the economy.

- With 100 percent Foreign Direct Investment (FDI) allowed through the automated route and initiatives like Make in India, major international players have entered the Indian engineering sector, thanks to significant growth opportunities available. FDI inflow reported by the Department for Promotion of Industry and Internal Trade (DPIIT) stood at $3.64 billion cumulatively since April 2000 to March 2020 for miscellaneous mechanical and engineering industries in India.

- The Government of India has ambitious plans to set up 5,000 Compressed Bio-Gas (CBG) plants over the next five years.

Business Model

PIL is India’s most successful company in the field of bio-based technologies and engineering with its presence all over the world. The Company has 5 businesses in its portfolio namely:

- Bioenergy

- High Purity Systems

- Critical Process Equipment and Systems

- Brewery Plants

- Wastewater Treatment Systems

PIL is in the business of process design, engineering, fabrication and commissioning of all the above segments. The Company currently earns its major revenue from the sale of ethanol process technology, plants and equipment and brewery plant and equipment. It is even building a sizeable portfolio of business from water and wastewater treatment systems, high-purity systems, and critical process equipment. PIL has developed fermentation systems that can handle a variety of raw materials.

It even produces Ecomol Molecular Sieve Plants that provide consistent quality products through minimum consumption of energy and maximum alcohol recovery. The major raw material for PIL is steel, which it sources from domestic as well as international markets.

From its initial stages, PIL has maintained a great focus on R&D and set up an R&D plant dedicated to ethanol production in 1987. For further diversification, it expanded its focus on synergized fields like brewery engineering and water treatment plants.

During 2002-2004, PIL developed its spectacular R&D facility named Praj Matrix focusing on research in the field of biotechnology. Also, during this period it attained leadership in fuel ethanol plants with over 70% market share while achieving the ₹1 billion turnover mark. Several major contracts, several alliances, and small acquisitions were formed in the further years after the launch of the Praj Matrix.

PIL also entered the critical process systems and wastewater treatment solutions in 2009 and 2010 respectively. The R&D lab started proving its metal and Praj Matrix was awarded the “Green Innovation Award” and the “Bio-Excellence Award”. Further, it was in the list of “top 50 hottest companies in advanced bioeconomy” in 2017 and jumped to 8th rank from 34th in 2019.

PIL acquired Neela Systems Ltd and named it as Praj HiPurity Systems (PHS). It is involved in the niche business of serving high purity water segment. PHS became a wholly-owned subsidiary of PIL in 2015.

PIL has come up with Innovative integrated Sustainable Technologies to optimize energy and water consumptions in the distillery. Adoption of it will help reduce water and thermal energy requirement by 75% and thus making it more environment friendly.

Impact of COVID-19

A particular struggle within the engineering and construction sectors is forecasted as businesses in these sectors are in danger from the economic downturn. Therefore, their immediate priorities in the coming quarters will likely get focussed on business continuity instead of investing in new premises.

As the effects of COVID-19 were felt around the world, all manufacturing and engineering services came to a halt. However, business activity will likely pick up its pace as unlock begins in most parts of the country and firms start resuming their operations.

The various restrictions put on-site by the government to manage the consequences of the virus may trigger a shortage of staff and manpower and disrupted supply chains, further creating handicaps in meeting contractual obligations. Some elements in construction and engineering are imported from overseas, which has been badly affected as well, creating a bad impact on the whole sector.

The hardest-hit has been faced by the liquid biofuels sector, which is at the core of PIL’s engineering business and is also the largest revenue-generating segment. Low oil prices have made it tough for the biofuels to compete with them. A key challenge for the producers has been the procurement of feedstock as most of the industry depends on forestry harvesting and processing residues which are impacted because of strong national restrictions.

PIL has started producing essential commodities like hand sanitisers to help the nation in fighting off the pandemic while giving itself the opportunity of generating revenue.

Differentiating Strategies

- Expansion of Business Horizons

One of the main focuses of PIL has always been towards expanding its business operations every year. The Company already has its operations in over 75 countries, spanning across 5 continents. It is not easy for every company to expand at such a significant rate and this is what makes PIL different from others. If PIL continues to expand its business at this rate then we may see a global dominance by the Company soon. - Zero Liquid Discharge (ZLD)

Day by day proper usage of water has been increasingly becoming an area of attention. Given the challenges on the efficient utilization of water resources and tightening the use of input water discharge norms, the industrial wastewater management division of PIL offers ZLD solutions to its customers. In FY20, the Company received a multi-year contract from a leading steel manufacturer for the management of their wastewater treatment. - Capital Gearing Ratio of 0%

PIL has had a capital gearing ratio of 0% because it hasn’t taken any debt in a long time. This safeguards the returns of their shareholders and also safeguards its ability to continue as a going concern. This is a different strategy because most of the companies need debt to leverage their returns but PIL has been generating returns without taking any debt at all.

SWOT Analysis

Strengths

- The previous year, PIL was granted 7 Indian patents and 3 foreign patents. The Company filed a total of 13 international patents last year. The current patent tally for the Company stands at 27. This helps the Company in being the sole enjoyer of profits in the initial years and will continue to enjoy till the patent expires.

- PIL has remained a market leader in the bioenergy sector for some time now. It already has a global presence and has successfully expanded the same by entering into two new countries; Bolivia and Kazakhstan. This shows how the Company has successfully diversified its revenue generation and given the rising demand in the bioenergy, we can expect this to be one of the key strengths of PIL.

- As the Government has reduced GST on ethanol for blending in fuel from 18% to 5%, it will result in better post-tax income for the shareholders, which in turn will also increase the value of the Company.

Weaknesses

- The Company has failed to register any increase in revenue over the last 5 years and has not been able to control the cost of its raw materials, which has been increasing over the previous years, leading to lower profit margins. This is not a good sign as sustainable profits are one of the key factors in a company’s long-term survival in a market.

Opportunities

- As PIL continues to maintain its focus on innovation, global reference base, and strong brand equity, it is now at a much better footing to capture newer business opportunities worldwide. Newer opportunities might help PIL in generating revenues which in turn will lead to better growth of the Company.

- Favourable steps have been taken by the Central Government in terms of new policies to encourage the bioenergy industry in India. To boost ethanol production in India, the Central Government announced several policy interventions such as Ethanol Blended Programme (EBP) and National Policy on Biofuels-2018.

- Currently, the per capita beer consumption in India is only 2 litres compared to around 20 litres in South Asian countries. Owing to the increased adoption of western culture, an upward trend in consumption patterns of craft and flavoured beer is prompting beer manufacturers to increase their manufacturing capacities, creating huge opportunities for the Company’s brewery plants.

- PIL is also exploring opportunities in developing other renewable fuels. Gaseous renewable fuel technology has tremendous potential as it complements Compressed Natural Gas (CNG). If PIL can manage to come up with another renewable fuel, the Company might be able to enhance its revenue-generating capabilities in the future.

- Isobutanol is a high energy feedstock for Jet biofuels that presents emerging opportunities for the aviation and racing industry. PIL has partnered with Gevo Inc., USA, to develop and commercialize the technology for the production of Isobutanol using sugar-based feedstock.

Threats

- FY19 witnessed headwinds in the form of regulatory challenges affecting the PHS business. This even forced the companies to defer their capital expenditure plans, thus affecting the avenues of growth.

- Weakness in sectors related to industrial/ infrastructural would lead to a slowdown in the order intake for capital goods companies, thus affecting margins of the companies involved in this space.

Michael Porter’s 5-Force Analysis

Barriers to Entry (High)

- Huge capital investment: PIL offers a very wide variety of process equipment and solutions covering bioproducts, wastewater treatment, brewery plants, high purity solutions, and bioenergy plants and ethanol solutions. Catering to such a wide range and innovation of such products requires huge investment in terms of Capex and R&D to meet cash shortfalls during operations which is just not possible for every company to do.

- Access to Industry Channels: PIL has established a global presence from its initial years and is currently the market leader in India in the biofuels industry and has developed a wide customer base and gained access to industry channels over the years creating a barrier for new entrants.

Bargaining Power of Suppliers (Low)

- Easy availability of raw materials: Steel being the principal raw material of the Company is procured from domestic as well as overseas suppliers. Some of the other raw materials are also procured from the overseas markets. The Company has got the appropriate mechanism to deal with fluctuation in material prices.

Bargaining Power of Buyers (Moderate)

- Customized high-value products: PIL deals in highly valued process equipment and solutions that specifically cater to customers’ needs. So, if the buyer stops its activities, this will directly affect PIL because there won’t be many other buyers who could purchase the customised equipments and processes. The buyers, therefore, have a bit of an upper hand in terms of bargaining.

- Few Players in the Market: Buyers of these process equipments and solutions have certain limitations with respect to the number of available players in the market like, switching costs, and other logistical constraints. Also, as PIL is a market leader in certain segments, it might be able to offer attractive costing and value-added services which brings down the bargaining power of the customer significantly.

Rivalry among Competitors (Low)

- Few other small players: PIL deals across varied segments of engineering equipment which are provided by different small individual players. The industry in which PIL operates requires huge initial investment outlay, which acts as an effective entry barrier for new firms. This limits the number of firms under this industry. PIL generates the highest revenues in its highest revenue-generating segment, bioenergy. As there is a high degree of product differentiation and switching costs are high for the buyers, the intensity of rivalry among the competition is comparatively low.

Threat of Substitutes (Low)

- Specialized systems and equipment: As the Company caters to a niche segment which requires highly technical and specialized products like 2G and 3G ethanol plants, bio-mobility, wastewater treatment solutions like zero liquid discharge, solvent recovery systems, Hi-purity solutions, brewery plants, etc., there are very few alternatives to these systems and solutions.

Branding and Other Initiatives

- Praj Foundation

Praj Foundation was found in 2004. The objective of creating this foundation was to put all of PIL’s social activities under one roof. Mr. Parimal Chauhdhari is the managing Trustee of this foundation and aims to contribute towards sustainable development by creating and implementing innovative ideas. - Water Resources Development Program

This program aims to provide water in drought-affected areas of Maharashtra, where rainfall has been significantly low over the last years. One such area is known as Marathwada where this initiative has been taken. As of today, PIL has covered over 37 villages which have enabled improved food security, economic growth, and reduction of poverty. - Basic Technology Schools

In a partnership with the Vigyan Foundation, PIL has implemented a technology program in 13 schools in rural districts of Western Maharashtra. This program aims to develop basic skills among students and explore industrial career opportunities in the industrial sector for the students. Currently, more than 6000 students have benefited from this program. - Tree Plantation

Every year, employees of PIL along with their family members plant over 2000 plants in an area near the hills of Pune. This initiative shows their commitment towards the environment, to make it a better place of living for everybody. The planted trees are also checked regularly and maintained by them.

Financial Analysis

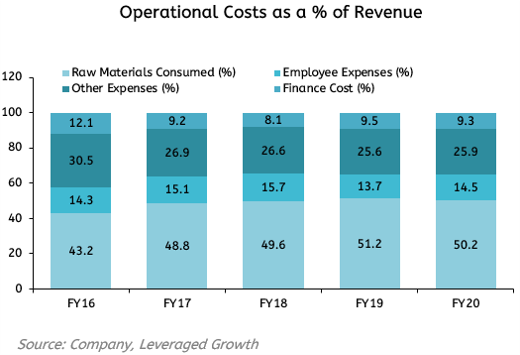

- Increasing Cost of Raw Materials

Since the FY16, the total expenses as a percentage of the revenue have increased. Raw materials consumed are over 50% of the total costs of the Company. This cost needs to be cut down significantly by the Company in order to have better margins in future. The Company’s major raw material is steel, and steel prices have been on a rally since FY16 thus increasing the cost of raw materials. This also raises a big question for the future profitability of the Company.

- A decrease in EBITDA Margin

The revenues of the Company have been on a decline since FY16 with an exception in FY19 during which a 23% increase was registered for the revenues of that year compared to FY18 as PIL had received projects under the Pradhan Mantri JI-VAN scheme and also due to order inflows related to Second Generation (2G) Ethanol. Before that, the cost of raw materials for the Company has been on the rise along with decreasing revenues, which led to lower EBITDA Margins. This highlights the need for cost management programs to have better sustainable profits in the future.

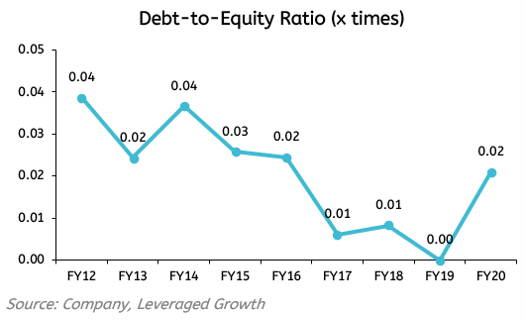

- Significant Spike in Long-Term Borrowings in FY20

PIL has been extremely careful in the use of leverage to buy assets and enhance ROE. This measure certainly restricts ROE to a certain extent but it provides the benefits of limited interest burden and thus mitigation of financial risk.

Although the Company has been on a streak of declining its long term-borrowings, it has been virtually debt-free up until FY19. Moreover, the total debt has constituted a very small portion of the total liabilities for the company. Short term borrowings have been nil since FY19.

PIL reported a spike in long-term borrowing in FY20 amounting to ₹151.70 million, which suggests the Company might consider using leverage to finance its long-term assets in future.

It suggests a very strategic move by the management of keeping its Balance Sheet debt-free and to utilize this strength in times of a recessionary phase or during a sudden emergency when it faces a severe liquidity crunch.

Risk Analysis

- Cyclicality and Seasonality of the Industry

The engineering business is a cyclical business in nature, i.e., this industry performs badly when the economy is doing poorly and vice-versa. Seeing the current downturn in the economy, a significant impact has been faced by the Company which has been hard to deal with. Any major R&D projects planned for the upcoming future will now have expected delays which is then going to impact the financials of the Company. - Input Prices

As we have already discussed, there have been significant increases in the cost of raw materials over the past few years. One of the inputs of the Company is steel. The Company has a high dependence on steel, the price of which is determined based on global demand. The Company also depends on crude oil, which in recent times has seen massive fluctuations thereby impacting the cost of raw materials of the Company. - Forex Risk

The Company is exposed to foreign currency risk on its account of revenue-generating and activities outside of India. The primary currency of the Company is INR, which has seen fluctuations over recent times and may continue to fluctuate in the future affecting the Company’s margins.

Corporate Governance

- The Company’s Board consisted of 10 Directors out of which 5 were Independent Directors including one-woman Director. This composition complies with the SEBI (LODR) Regulations. One of the directors Mrs. Parimal Chaudhari is the wife of executive Director Mr. Pramod Chaudhari, besides this, there are no other inter-se relationships amongst the Board members.

- Independent directors of PIL, Mr. Berjis Desai holds directorships in 8 other public companies, Mrs. Mrunalini Joshi is a director in Nichrome India Ltd., Dr. Shridha Shukla is the Managing Director of kPoint Technologies and the Co-founder and Chairman of the Board at GS Lab., Mr. Suhas Baxi is the Managing Director of Konecranes and Demag Private Limited, none of the directors of the Company hold directorships in more than 20 companies or more than 10 public companies whether listed or not.

- A total of 5 board meetings were held during FY19 . The intervening gap between any two meetings was within the prescribed period suggested by the Companies Act, 2013, and the SEBI (Listing Obligations & Disclosure Requirements) Regulations, 2015.

- A Familiarization Programme for Independent Directors has been put in place wherein an orientation program is conducted that includes familiarization with the Company, their roles & the industry in which the Company operates.

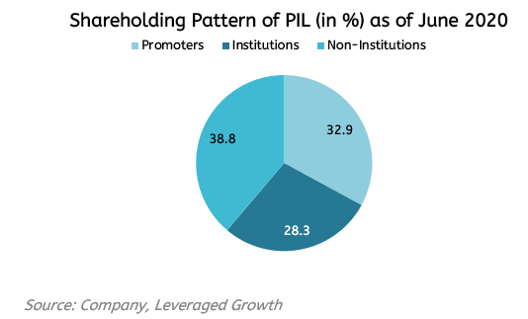

- The promoters of the Company held 32.92% shares of the Company (as of Jun 2020). There has been no significant change in the promoter shareholding of the Company.

- The average increase in the managerial remuneration of the Company for FY19 was around 4%. Whereas, the percentage increase in the salaries of employees other than the managerial personnel was around 9%.

The End-Note

- PIL’s business currently seems to be largely affected by the COVID-19 pandemic and a huge drop in oil prices. The pandemic has disrupted global supply chains, created manpower shortage, and decreasing oil prices have made bioenergy alternatives less attractive. This has affected the overall supply and demand dynamics of the Company, as moving forward, businesses will be more prudent about capital goods expenditure in the short-term because of tightened liquidity, which poses a severe threat to the ability of the Company to generate increasing revenues.

- As the businesses around the world face a liquidity crunch, PIL has decided to take on more debt to keep its supply chain running. This seems to be a prudent decision as the Company has been virtually debt-free until now and is in a position to use the financial leverage to sustain its operations and generate revenues.

- The Company has always been ahead in terms of R&D projects, developing sustainable and eco-friendly technology, and maintaining its focus on decarbonization, it reserves a great opportunity for itself to perform well as people and businesses around the globe become more mindful of the consequences of climate change.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Pratik Sharma | Mukul Gupta

Research Desk | Leveraged Growth