Click here to download the report

A Journey of Inorganic Growth

Piramal Enterprises Limited (‘the Company’ or ‘PEL’), formally known as Piramal Healthcare Limited, of the Piramal Group is a large diversified Company with its presence in financial services and pharmaceuticals industry. Of the total consolidated revenue of Rs.13068.3 crore in FY20, financial services contributed 59% and the rest was by the pharma sector. PEL has a large global presence with 34% of the total revenues in FY20 being generated internationally.

In financial services, PEL offers a complete range of financial products in both wholesale and retail financing. In wholesale lending, the Company provides financing to real estate developers and corporate clients, whereas in retail lending, the business offers housing loans to individual customers. In the pharma segment, PEL offers end-to-end manufacturing capabilities of drugs spread across 13 global facilities and a distribution network of over 100 countries. PEL’s consumer products business ranks among the top five in the Country. Its top brands include Saridon, Supradyn, I-Pill, Polycrol, Jungle Magic, and Lacto Calamine among others.

The Company is considered as the preferred partner in India for various strategic investments by leading organizations across the Globe. PEL has a long-standing trusted strategic partnership with Bain Capital, Allergan, The Carlyle Group, and IFC among others.

Origin of PEL

A billionaire industrialist and the Chairman of PEL, Ajay Piramal, started his career at the age of 22 in his father’s textile manufacturing company. Soon, he experienced personal tragedies of losing his father and one of his brothers in a short period. It was then that he moved to religion for spiritual guidance. He became a staunch believer in the tenets of the Bhagwat Gita so much such that today all his conference rooms are named after Arjun. When he inherited the textile business, ‘life looked bleak’ to him. But as he said, “I survived as the Lord must have carried me when I needed Him the most”.

While Ajay Piramal was the Chairman of the textile business, a strike forced all textile businesses in Bombay to closure. Ajay soon decided to exit the textile business. He then started his acquisition drive since he believed that the only way to grow was to acquire companies in the relevant fields. In 1988, Ajay acquired Nicholas Laboratories, an Australian MNC wanting to exit India, since he thought that the next boom in India would be in the pharmaceuticals industry. In 1992, Nicholas Laboratories Ltd. was renamed to Nicholas Piramal India Ltd. There was no looking back for Ajay, as he started with a spree of overseas acquisitions which helped Nicholas enter the list of top 5 pharma companies in India. In 2008, Nicholas Piramal India Ltd. changed its name to Piramal Healthcare Ltd. (PHL). In 2010, PHL had the highest valuation in the pharma industry. This motivated Ajay to sell his Healthcare Solutions business to US drug maker Abbott for a record Rs.17,000 crore. In 2012, PHL was renamed to what it is now known as, Piramal Enterprises Limited.

An inspiration for many, Ajay Piramal diversified from the textile business to a field completely new to him, the pharma business. At that time, nobody was interested in the pharma industry and multinationals wanted to leave India. But, in the words of Ajay Piramal, “We saw a huge opportunity. The market was growing. The penetration of modern medicine was still limited. There were lots of new doctors coming in, and treatments were required. That’s why we entered into the pharma space then”. Apart from being an exceptional leader with farsightedness, Piramal is also a perfect example for someone looking for spirituality in management and negotiations.

Industry Analysis

Financial Services Industry

- Between FY17 and FY19, Non-Banking Financial Companies (NBFCs) witnessed a sharp growth with 25% CAGR. The asset size of NBFCs and Housing Finance Companies (HFC), by March 2019, was Rs.44.4 lakh crore. This was dominated by loans to industries, real estate developers and retail (a majority of them being MSMEs).

- The real estate sector accounts for 7% of GDP and 17% of employment. This sector has long been impacted by the various regulatory reforms and policies such as GST, Real Estate Regulatory Authority (RERA) Act and demonetization announced in the previous few years. Liquidity crunch in the real estate sector has led to the tightening of cash flow positions of the financers.

- In India, retail lending penetration is relatively low accounting for approx. 15% of the Country’s GDP, as compared to 81% in the U.S. and 66% in China. Within retail lending, housing finance forms a major part of the loan book.

- The Government has been introducing measures to inject liquidity, relax reforms and assist in partial guarantees to NBFCs to improve their financial condition.

- The major players in the industry include Bajaj Finance Limited, HDFC Securities, Mahindra & Mahindra Financial Services Limited, and L&T Finance Limited among others.

Pharmaceuticals Industry

- The Indian Pharmaceutical Industry holds an important position in the global pharmaceuticals sector, catering to 50% of global demand for various vaccines, 40% of generic demand in the U.S., and 25% of all the medicines in the UK.

- The industry was valued at $37 billion in FY20 and contributed 1.5% to the GDP directly (another 3.5% indirectly).

- Medicines are priced very low in India (amongst the lowest in the world). The Government plays an important role in the pharma industry. As per Economic Survey 2019-20, the government expenditure on health sector as a % to GDP increased to 1.6% in FY20 as compared to 1.2% in FY15.

- Pharma industry has been expected to play a pivotal role during the pandemic.

- Major players in the pharma industry include Cipla, Sun Pharma Industries Limited, Dr. Reddy’s Labs, and Biocon among others.

Business Model

PEL operates in the Financial Services Industry and the Pharmaceutical Industry.

Financial Services Business

- Wholesale Real Estate (RE) Lending: The Company offers end-to-end RE financing to residential RE, hospitality sector as well as commercial RE where the portfolio is split across under-construction projects, lease rental discounting and loans against property.

- Corporate Financing Group (CFG): CFG offers loans to clients from the non-RE sector such as infrastructure, cement, logistics, etc. to develop credit solutions that tie into their underlying cash flow positions. The yield from these loans’ ranges from 12% to 16%. PEL has also formed an Emerging Corporate Lending (ECL) platform which is a sector-agnostic platform which offers funding with a ticket size of Rs.10 crore to Rs.100 crore. Presently, the average ticket size is Rs.47 crore across 14 deals.

- Housing Finance Company (HFC): HFC offers individual retail loans to home buyers. PEL issues housing finance loans with an average ticket size of Rs.70 lakh. HFC accounted for 11% of overall loans as of FY20 and is expected to increase in the medium to long-term. The Company is also in the process of developing a multi-product retail lending platform, taking cues from the current environment and it would be ‘digital at its core’.

- Alternative AUM: This consists of various investment platforms and joint ventures (JVs). Alternative AUM includes strategic partnerships with marquee partners like Bain, APG, Caisse de Depot et Placement du Quebec (CDPQ), and The Canada Pension Plan Investment Board (CPPIB) to develop fund-based platforms such as IndiaRF-Stressed Asset Investing, Mezzanine investments in Infra, Residential RE, and senior-debt in non-RE, non-infra sectors. These are innovative financial products developed to cater to specific opportunities across sectors for scalable returns.

- MSME financing: PEL had invested Rs.4583 crore in Shriram group, a leading MSME financing company, for a 9.96% stake in Shriram Transport Finance Corporation (STFC), a ~20% stake in Shriram Capital Limited and a ~10% stake in Shriram City Union Finance. In Q1FY20, the Company sold its entire stake of 9.96% in STFC for ~Rs.2300 crore. The total remaining investments are worth ~Rs.3954 crore as of March 2020. Through these investments, PEL aims to diversify its operations across MSME financing.

Pharmaceuticals Business

- Contract Development and Manufacturing Organisation (CDMO): Offering integrated end-to-end drug discovery, development and manufacturing services to pharma companies for drug substance and drug formulations with strong capabilities in High Potency Active Pharmaceutical Ingredients (APIs) and Anti-Body Drug Conjugates. PEL has manufacturing facilities located in India, US, UK and Canada with a diversified customer base.

- Complex Hospital Generics: Global supplier of niche inhalation anesthesia, injectable anesthesia, pain management and other products used in hospitals. The Company launched 9 injectables during FY20 and has strong commercial capabilities with a distribution network of over 100 countries.

- Consumer Healthcare: Portfolio includes marquee brands such as Saridon, I-Pill, Lacto Calamine, Polycrol, etc. across Over-the-counter (OTC) segments of vitamins, women care, skincare, etc. PEL is the leading player in India in the self-care space with a wide distribution network across India.

- In the consumer healthcare segment, the Company has grown from a 6-brand portfolio in FY11 to 20+ brands in FY20. PEL has adopted an ‘e-commerce first’ strategy to deliver successful new products.

- PEL has developed its pharma business mainly through inorganic growth acquiring mid-size companies and businesses.

COVID-19 Impact

- The NBFCs were already facing liquidity stress owing to rating downgrade and default post-IL&FS crisis. The COVID-19 pandemic added fuel to the already burning financial sector. Since the RBI announced a moratorium on loans repayments between March 1 and August 31, 2020, cash inflows are expected to be impacted and liquidity stress may also increase.

- The pharma industry is expected to undergo significant changes in the post-COVID-19 era. For the manufacturers, the emphasis has shifted from cost-effectiveness to resilience and increased importance to supply chain strategies including backward integration, geographical diversification, etc. Inspection of manufacturing sites by agencies such as the US Food and Drug Administration (USFDA) has sped. This is because USFDA could not inspect as they would do, due to lockdown restrictions in various parts of the globe. Hence, they had to inspect using alternative approaches and give approval so as to minimize drug shortages in the time of crisis. This may result in increased industry-wide capacity for some products.

- Demand for preventive healthcare products is bound to increase due to the pandemic. While hospitals are repurposed to prioritize COVID-19 patients, surgeries have reduced and so the demand for anesthesia and other allied products used in the surgeries. However, it is expected to normalize over time.

- The drugs manufactured by PEL are considered essential by many governments across the world. Hence, their manufacturing operations were largely open and operational. The Company, through its CDMO facilities, has been assisting customers to develop therapeutics or vaccines for COVID-19. PEL has also launched two new brands of hand sanitizers in the wake of the pandemic and has also ramped up the production of multivitamins, wet wipes and alike seeing the surge in demand for these products.

Steps Taken by PEL to Counter COVID-19

- As a matter of prudence, PEL made an incremental provision of Rs.1,903 crore for COVID-19. This accounts for 5.8% of the overall loan book and 246% of Gross Non-Performing Assets (GNPAs). GNPA ratio in FY20 increased to 2.4% compared to 0.9% in FY19. This was because some of the Stage-2 loans (30 days past due) of the Company had to be transferred to Stage-3 (90 days past due).

- The Company has also diversified its borrowing mix by raising long-term funds and reducing its exposure to Commercial Papers (CPs) by 94% YoY.

Differentiating Strategies

- Differentiated Business Model in the Pharma Space

PEL has carved itself uniquely in the pharma space due to its differentiated business model. The Company acquired Coldstream Labs (2015) and Ash Stevens (2012) to add sterile injectables and high potency API manufacturing to its portfolio. This, along with Antibody Drug Conjugates (ADC) capability, has allowed PEL to become the preferred integrated partner in the field of oncology. An integrated CDMO acts as a growth driver for the Company since pharmaceutical companies who outsource their requirements to CDMOs prefer a one-stop solution for all their requirements. For PEL, over 90% of revenues in the pharma space is derived from the niche business of complex generics and CDMO. For most of the Company’s peers, which includes Cipla Ltd., Aurobindo Pharma Ltd., etc., this figure is less than 5%. - Sustainable Model for Financial Services

The Company has built a differentiated and innovative business model for the financial services that has paved its way through the most difficult times characterized by demonetization, followed by GST Act and RERA. PEL entered the financial services industry in 2011, post the Great Financial Crisis.

– Partnering with developers throughout the project life cycle for end-to-end real estate financing.

– Ability to cross-collateralize (when collateral for one loan is used to secure another loan) and innovatively structure deals.

– Having a stronger relationship with Tier-1 developers.

– 100% secured lending.

– A differentiated model for HFC space using product differentiation, geography selection and customer selection. Since HFC is a highly competitive space, PEL would differentiate itself by choosing deeper geography, self-employed customers instead of salaried-class, and a disaggregated product. For example, in case of a home loan, the Company would try to disaggregate the home loan to loans for an under-construction apartment, loan for self-construction on a plot and likewise and offer it to smaller geographies also and to cash-salaried or self-employed people. - Looking Ahead of the Curve

PEL has always looked ahead of the curve and continues to do so. This has always paid the Company well in the long-run and helped create value for its stakeholders. A few examples:

– In 2005, India started recognizing drug patents. Consequently, the Company anticipated price controls and heightened competitive regime and thus, exited Healthcare Solutions in 2010. It was one of the highest valued deal in branded generics space globally at 9x sales and 30x EBITDA. Later, the domestic industry was impacted by the tighter regulatory environment.

– In FY18 and FY21, PEL raised ~Rs.7000 crore (to fund the growth of the financial services business) and ~Rs.14,500 crore respectively. These both were done much in advance of the need. Especially, in the current times, the Company has successfully raised a substantial amount which shows the confidence of investors in PEL during such a stressed period. Out of the total Rs.14,500 crore, ~Rs.3650 crore was through a rights issue which was oversubscribed by 1.15x times.

These instances show the farsightedness of the management of the Company and its prudent nature of management. - Organic as well as Inorganic Growth

The Company, which was once a family textile business, has now been evolved into a conglomerate in completely diverse sectors. This has been a result of organic growth accompanied by very fruitful inorganic growth of PEL. The Company first forayed into the pharma business by acquiring Nicholas Laboratories in 1988. Since then, PEL has been looking for inorganic opportunities in India as well as abroad. It has till now completed around 50 acquisitions.

SWOT Analysis

Strengths

- The Company provides integrated CDMO facilities ranging from drug discovery and clinical development to commercial manufacturing of API. This integrated model of PEL helps it become a one-stop-shop for all the various services required across the drug lifecycle. This also helps PEL in building a stronger client relationship and lock-ins and facilitates cross-selling.

- Healthy asset quality: PEL has healthy assets due to its robust asset monitoring framework which takes place throughout the life-cycle of the project. The entire lending of the Company is 100% secured. The Company has consistently proved its ability to cure stressed projects which are in Stage-3 also.

- PEL has diversified its loan book by decreasing the share of loans given to the real estate developers from 83% in FY15 to 70% of the overall loan book as on FY20 while increasing the share of retail loans. This diversification will reduce single-borrower exposure of the Company and help focus on a calibrated growth.

Weaknesses

- PEL’s corporate structure is such that the Company is not able to unlock its full potential. Since the IL&FS crisis in September 2018, the NBFC industry has not revived to normalcy yet. PEL’s pharma business continues to do good and the Company is also growing inorganically. But since both these businesses are merged with the parent company, PEL, investors are not able to reap benefits of the growth in the pharma business. Nor is PEL able to show good margins in their consolidated balance sheet. PEL, however, has plans to demerge its pharma business in the future.

Opportunities

- Continuous tightening of liquidity in the NBFC sector and consequently the major reforms undertaken by the Government will lead to a consolidation in the industry. Only well-capitalized and well-governed NBFCs are expected to survive. Hence, competition is expected to reduce.

- Due to the tough environment and consolidation taking place, many NBFCs and real estate developers that face liquidity and other issues would be willing to take a haircut and down-sell their portfolio. PEL sees this as an opportunity to capitalize on the assets and portfolios available at a cheap discount. The Company could be looking at either a portfolio buyout from an NBFC or buying-out a developer.

- Emerging biotechs that are looking for integrated solutions across drug substance, product development and manufacturing are key drivers of growth for PEL’s pharma business.

Threats

- The moratorium placed on the loans by Reserve Bank of India (RBI) till August 31, 2020, will result in rising NPAs & end up weakening the economic conditions. This would again build pressure among the lenders in the industry unless RBI issues some measures to uplift the situation.

- PEL has ~70% of its loan book exposure to the real estate sector as of FY20, a sector which has been deeply impacted by the pandemic. This exposure may lead to higher than expected funding requirements by the Company to keep the projects floating.

Michael Porter’s 5-Forces Analysis

Barriers to Entry

- NBFCs are highly regulated. Stringent regulatory norms pose a barrier to the entry of new players. Because of the ongoing period of stress in the finance industry and the sectors related to it such as real estate, etc., consolidation is expected to take place where only well-governed and strong companies would be able to survive.

- The pharmaceuticals industry is also highly regulated. Companies have to go through quality inspections. New entrants would have to build their brand image with doctors for long-term survival.

Bargaining Power of Buyers

- The bargaining power of buyers is substantial in the financial sector in the sense that the customers can easily shift from one company to another if the other is providing better returns with more agreeable terms and conditions of the services provided.

- In the pharma sector, there is a marked difference between the end-user and the influencers, i.e., doctors. Since many companies are providing a similar product in the market, doctors can pressurize the manufacturers to reduce their prices by not prescribing their medicines. The end users have no bargaining power since they have to buy the medicines prescribed by the physician.

Bargaining Power of Suppliers

- The suppliers in the finance sector are mainly banks and other financial institutions. Since the terms on which they operate are mainly regulated by the RBI, they have low bargaining power.

- Even in the pharma sector, suppliers have low bargaining power. Main suppliers of the pharma industry belong to the chemical industry. These suppliers are large in number and the pharma company can easily switch from one supplier to another.

- PEL has been trying to diversify its vendor base to mitigate supplier-concentration and location risks. The Company has also been trying to do backward integration for the same reason. The sourcing of Key Starting Materials (KSMs), APIs, and finished dosage forms for its complex hospital generics products are done from vendors across different countries to bolster supplies.

Rivalry among Competitors

- The financial services industry, as well as the pharma industry, is highly fragmented. There is, thus, high competition in both these industries. The pharma industry is characterized by high competition with the Herfindahl index of less than 1.5 (a measure of competitive intensity of an industry with <1.5 indicative of a competitive marketplace).

- Companies in neither of the industries can hike prices or charge exorbitant rates due to the stiff competition.

Threat of New Substitutes

- Substitutes available for financial products are limited. But customers have the option to consider banks for the same financial products than going for NBFCs.

- From the viewpoint of the pharma industry as a whole, there is a very low threat of new substitutes. Advances made in the field of biotechnology, Ayurveda, etc., may act as a substitute for some of the products in the pharma industry.

Branding and Other Initiatives

- Marketing Efforts of PEL

– PEL has been doing some advertising mainly in the form of digital marketing. The Company associated with Havas Media for digital marketing of the consumer products division in 2019. Havas has been responsible for marketing over social media, Search Engine Optimization (SEO), Online Reputation Management (ORM) and website duties for 22 brands which run across vitamins, nutrition, skincare, antacids, baby care, etc.

– The Company’s consumer products division has also roped in Sourav Ganguly, former captain of the Indian cricket team and the current President of Board of Control for Cricket in India (BCCI), as the brand ambassador of the PEL’s antacid brand, Polycrol.

– In 2018, PEL’s wholly-owned subsidiary Piramal Capital and Housing Finance Limited (PCHFL) launched a brand campaign called ‘Bada Socho’ for a period of 60 days targeting the cities of Mumbai, Delhi, Bangalore and Pune. This campaign ran across radio, digital modes and Out-Of-Home (OOH) advertising. The campaign was intended to highlight the ethos of the Company and its financial services business and how PCHFL encourages its customers to ‘think big’ and transform their dream into reality whether it is by buying a new home or by growing their business.

- Corporate Social Responsibility (CSR) Initiatives

The Company conducts its CSR initiatives through Piramal Swasthya Management and Research Institute, the subsidiary of Piramal Group’s Section-8 company, Piramal Foundation, and Piramal Foundation for Education Leadership. With a focus on universal primary education, youth empowerment and transforming health, these entities have taken the following initiatives:

– Remote Health Advisory and Information (RHAI): It provides 24×7 health advise to remote and vulnerable sections of the community through a toll-free number.

– DESH (Detect Early and Save Him/her): The community is based on cancer screening programmes. More than 28,000 community members have benefitted from this.

– School leadership Development Programme: Partnered with corporates, educational institutes and governments of Rajasthan and Maharashtra to set up 375 functional libraries across the two states.

– State Transforming programme: Collaborated with 10 State Governments to build institutional capabilities of state-level education institutions.

- Fight against COVID-19

– Piramal Swasthya, in a public-private partnership, operated ‘104 toll-free number’ in eight State Governments across India in support of COVID-19 management. The helpline also helped create awareness around the preventive measures to be taken for the same.

– The Piramal School of Leadership at Bagar was made available as an Isolation Centre which accommodated >300 suspected patients.

Financial Analysis

- PEL Deleveraged to Comfortable Levels

NBFCs enjoyed a very good run before demonetization and hence, PEL had good financials then considering the favorable environment. But post-demonetization, cash flows were severely impacted and have failed to normalize till date. The Company has deleveraged its balance sheet to comfortable levels in FY20 by reducing the Net Debt to Equity multiple to 1.3x times as of FY20 compared to 2.1x in FY19. PEL was successful in raising ~Rs.14,500 crore in FY20 through various transactions:

– ~Rs.6,800 crore through the sale of DRG in February 2020

– Rs.1,750 crore through preferential allotment to CDPQ

– Rs.3,650 crore through a rights issue

– ~Rs.2,300 crore from the sale of a stake in Shriram Transport

This naturally increased the equity base from Rs.27,233.33 crore in FY19 to Rs.30,571.6 crore in FY20. At a time when the pandemic has struck the entire world, PEL successfully raising a substantial amount of capital is an indication of its strong position in the market and its reputation among the investors.

PEL’s ability to raise funds in such a stressed environment has been the main reason for the positive credit rating of the Company. Also, PEL has maintained a healthy asset quality despite the poor economic conditions. This is due to the strategy that PEL has adopted off-late to lend to only those developers that are in a better position than others since the Company fears consolidation will take place which would wipe out weak players. Also, PEL’s entire loan book is 100% secured, with healthy cash and security cover taken at the time of origination of deal. Even though the GNPA of the Company increased from 0.9% in FY19 to 2.4% in FY20, the Company has shown the potential of recovering money even from Stage-3 loans. For example, PEL has reduced its exposure to Nirmal Group from a peak of Rs.200 crore to Rs.7 crore.

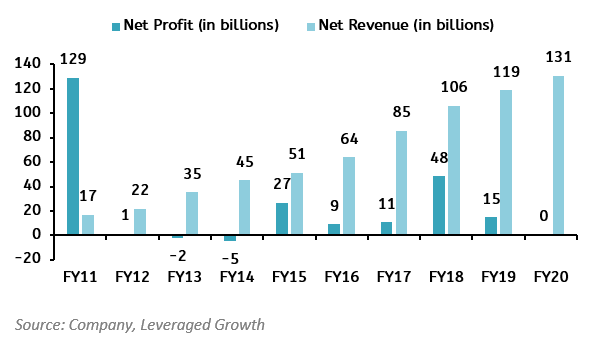

- Steady Growth in the Topline as well as the Bottom Line.

The Company has been posting steady growth in revenues with a 9.98% growth YoY. The pharma business performed well during the year. Depreciation of rupee helped the Company since more than 80% of pharma revenue comes from the global market. The net profit of the Company reduced from Rs.1,464 crore in FY19 to Rs.21 crore in FY20. This impact was mainly due to non-recurring items. PEL made an incremental provision of ~Rs.1900 crore in FY20 for the financial services business as a cautionary measure considering the risk from COVID-19. Other things such as one-time Minimum Alternate Tax (MAT) credit reversals and sale of DRG business impacted the figures. In FY11 also, the sale of the Company’s drug formulation business to Abbott resulted in such an exceptional profit figure. However, the normalized net profit for the Company (i.e., excluding the one-off items) for FY20 stood at Rs.2615 crore, a 22% growth on a YoY basis.

While the profit margins are on a downslide since FY18 onwards, revenues are on a rise. This is because although the pharma business is posing a steady growth, the financial services business is under stress from the past 18 months. The Company has strategized to give priority to improving liquidity and strengthening the balance sheet rather than focusing on growth. This also reasons out why the loan book of the Company has not grown much in FY20. While the wholesale loan book has decreased by 12% YoY in FY20, HFC loan book has increased by a mere 6.67%.

Risk Analysis

PEL has been taking very conservative steps for the past few quarters due to uncertainty in the financial services industry. And as Ajay Piramal once said in an interview,” My biggest focus is not to see that growth but to see that we are managing our risk well”. The Company faces a few risks by virtue of belonging to respective industries:

- Interest Rate Risk: PEL faces interest rate risk in the financial services business. It is the risk which a company faces due to a change in the market interest rates. For example, if the Company borrows at a higher rate and lends at a lower rate, it would face a loss. The duration of the assets and liabilities also matters to ensure there is no asset-liability mismatch.

- Liquidity Risk: NBFCs are going through a liquidity crunch for the past few quarters. In these times, maintaining adequate liquidity is of utmost importance since liquidity shortfall in one company can have repercussion effect on the whole industry. PEL has taken the strong initiative of reducing debt/equity to comfortable levels.

- Quality Risk: Due to strict regular inspections by the USFDA, the Company always has a risk of its products or facilities being red-flagged by the inspection agency due to issues in quality. PEL has cleared all its inspections successfully till date.

- Currency Risk: Since PEL has its pharma business largely distributed across the globe, currency fluctuations especially rupee appreciation will harm the revenues being generated by PEL outside India, that made up nearly 34% of the total revenues in FY20.

Corporate Governance

- The Company’s Board consists of 13 Directors out of which 8 are Independent Directors. No Nominee Directors are representing any institution in the Board of the Company.

- Two Independent Directors resigned the Board in FY20. There was no material reason given by both for the resignation other than an increase in professional commitments.

- Two Directors, Ms. Nandini Piramal and Mr. Anand Piramal are the children of another two Directors, Mr. Ajay Piramal and Mrs. Swati Piramal. Other than this, none of the Directors of the Company is inter-se related to each other.

- The Board of Directors met 7 times in FY20. Apart from this, the Independent Directors also had a meeting to review the performance of the Chairman, the Non-Independent Directors and the Board as a whole.

- Ms. Swati Piramal is an Independent Director in Nestle India Limited and Ms. Nandini Piramal is a Non-Executive Director in The Swastik Safe Deposit and Investment Limited. However, none of the Directors holds Directorship in more than 20 companies or more than 10 companies whether listed or not.

- Promoters have 46.06% shareholding in the Company as of June, FY21. The promoter holding has gradually decreased over the years from 51.38% in FY18 and 49.70% in FY19.

The EndNote

- Financial Services Industry is not expected to recover anytime soon. COVID-19 prolonged the crisis in the industry. More NBFCs would seek to raise equity at this time. PEL has comfortably raised enough capital at the right time to deleverage the balance sheet. However, this may result in reduced RoE for the Company in the coming quarters.

- While some segments of NBFC would see recovery earlier, real-estate lenders would have to wait longer due to delayed construction activities and a slowdown in sales. PEL has an exposure of 74% of loan book to the real estate developers. This raises concerns although the Company claims it would recover all the money. The Company may have to down-sell some of its assets to boost liquidity and cash flows.

- PEL has clearly defined its roadmap for the future. The Company is planning to demerge its pharma business which is expected to unlock value for PEL and investors in the pharma segment and also simplify the corporate structure of the Company. Apart from this, an online differentiated consumer-lending platform is being developed to tap into the digital ecosystem. This would create a differentiated space for the Company in consumer lending and would also diversify its business by expanding from Tier-I cities to Tier-II and Tier-III cities.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Gaurav Jalan

Research Desk | Leveraged Growth