Click here to download the report

A Hidden Gem in the Packaging Industry

Huhtamaki PPL Limited (“the Company” or “HPPL”) offers a wide range of packaging solutions which include flexible packaging, labelling technologies, specialised cartons, holographic options, and some other high-end packaging solutions based on the client’s requirements. The Company’s packaging machine division provides complete packaging solutions to customers.

HPPL is a leading consumer packaging company in India, having a Pan-India presence, backed by 18 manufacturing sites and 2 Research & Development centres. The Company’s international business division has its presence across 4 continents catering over 50 clients.

The Company’s business model caters largely to FMCG and healthcare industry. HPPL provide flexible packaging solutions for:

- Food

- Beverages

- Pet Food

- Health Care

- Personal care & household

- Recyclable solutions

Major Clients of Huhtamaki PPL Ltd.

How was HPPL born?

At a young age of 18 years, Mr Sardarilal Talwar was already running his successful inherited departmental store, which besides being the largest retailer, was a major importer and wholesaler. Mr Talwar soon got the idea of importing paper and converting it into paper products, thus starting flexible packaging. They soon got their first assignment of converting paper products from the “British Army Dairy”. This new idea revolutionised the packaging industry and “The Paper Products Ltd.” or “PPL” was born in 1935. The Company originally started as a partnership concern and was set up in Lahore, Pakistan (erstwhile India). Post partition the Company shifted to Delhi, India in 1947 and later went public in 1950. PPL later became a part of the global packaging group “Huhtamaki Oyj” in 1999, who were the global leaders in the consumer and industrial packaging segment. In 2014, PPL was renamed as Huhtamaki PPL Ltd. (HPPL).

Indian Flexible Packaging Industry

- Ranked 11th largest in the world and 5th largest in India’s economy, the Indian packaging industry is among one of the fastest-growing sectors.

- As per the Packaging Industry Association of India (PIAI), the industry’s growth was observed at 22% to 25% p.a. before the impact of COVID-19.

- The growth in the flexible packaging sector in India is mainly driven by food processing, pharmaceutical, FMCG, and healthcare sectors. FMCG is the 4th largest sector in the Indian economy, and food processing accounts for more than 50% of total demand for flexible packaging.

- With the recent growth in e-commerce and technology advancement, the demand for flexible packaging has gone up considerably.

- As per Technavio’s latest market research report, the Indian flexible packaging industry will grow at a CAGR of almost 12% from the year 2020-24.

- The growth of the Indian packaging industry will be highly influenced by rapid urbanisation and rising income level, and the recent trends (COVID-19) have clearly shown the need for well-packed quality foods and beverages.

- The per capita packaging consumption in India is kind of low at 8.7 kg compared to countries like Germany and Taiwan where it’s 42 kg and 19 kg, respectively.

- India is the 5th largest retail destination in the world which is expected to generate revenue of ₹71,986 billion by 2020. The expansion of the retail industry will directly lead to the expansion of the flexible packaging industry in India.

- Environmental regulations have a severe impact on the packaging industry; however, it has also provided opportunities for the flexible packaging industry to grow due to its eco-friendly nature and low cost of production. For instance: HPPL saw significant benefit due to the plastic ban in March 2019, where the companies started considering flexible packaging as a better option to market their products.

Business Model

- HPPL is a provider of aesthetic and sustainable packaging solutions and holds a wide range of product portfolio. HPPL is a leading converter in the flexible packaging industry (Converters are companies which combine raw materials such as polyester, adhesive, inks, foams, plastic, metals, etc. to create a new product).

- HPPL follows a business to business (B2B) model and mostly caters to FMCG and Pharmaceutical companies across India. It operates through consumer packaging segment, where almost 23% of the revenue is derived from exports.

- The products offered by HPPL are utilised in various packaging application which includes food and beverage, personal, oral, healthcare, tube laminate, pharma and other speciality products.

- The Company’s key raw material consists of films, inks, adhesive, and solvents, which are derivatives of crude oil.

Films include Biaxially Oriented Polypropylene Films (BOPP Films), Polyethylene Terephthalate Films (PET Films), and Polyvinyl chloride Films (PVC Films), which account for more than 50% of total input cost. These materials are fairly standardised and less differentiated, for which the Company has domestic as well as international suppliers.

- The Company passes the increased cost to its customer due to fluctuation in raw material prices.

- HPPL has 18 manufacturing units across India namely Parwanoo and Baddi (Himachal Pradesh), Taloja (Maharashtra), Thane (Maharashtra), Mahape (Maharashtra), Khopoli (Maharashtra), Rudrapur (Uttarakhand), Gangtok (Sikkim), Guwahati (Assam), Silvassa (Dadra and Nagar Haveli), Daman, Sri City (Andhra Pradesh), and two plants in Ambernath (Maharashtra), Hyderabad (Telangana), Bengaluru (Karnataka) each and is still on the way of expanding their reach.

- HPPL is a subsidiary of the global packaging group Huhtamaki Oyj, Finland.

COVID-19 – Positive Outlook for the Flexible Packaging Industry

The current pandemic has no doubt impacted all the sectors and has put industries in severe pressure where survival is a primary concern. HPPL’s majority of revenue is derived from the FMCG and Pharmaceutical sector, where the COVID-19 impact is the least amongst all the sectors. FMCG companies are expected to get back on track by the end of Q3CY20 with more focus on delivering safe and quality packaged hygienic products. Indian pharma, being a global leader in generics both in domestic as well as in the international market, has been relatively resilient to the COVID-19 disruption. Made in India drugs exported to developed countries such as the U.S., Japan, and Europe are known for their safety and quality. Hence, since pharma is the need of the hour, and ensuring such high-level safety and quality standards is important, all of this acts as a booster for the packaging industry.

Differentiating Strategies

- Strategic Acquisitions

The Company’s acquisition strategy has helped them penetrate those market segments which were out of reach and acquire some major domestic and international clients, with the recent one being where they acquired the flexible packaging division of Mohan Mutha Polytech Private Limited (MMPPL). Through this acquisition, they are focusing on improving service levels to existing customers and build new client relationships across Southern India. A significant portion of HPPL’s revenue comprises of their strategic acquisitions. - International Presence

HPPL has expanded its business in the overseas market intending to acquire a significant global market share and compete with other players worldwide. Today HPPL has its presence in 4 continents (South America, North America, Africa, and South East Asia) and caters to over 50+ international clients. With the recent acquisition of MMPPL, that had several domestic and international clients, the Company looks forward in expanding their business in other geographies very soon.

- Cost Controlling Measures

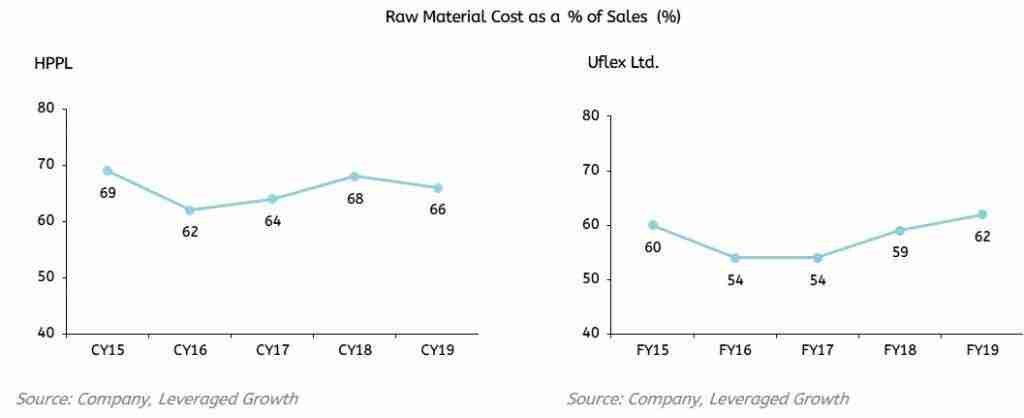

The Company has been working towards cost reduction over these years, by increasing its focus on producing environmental-friendly products which could be easily recycled and using renewable resources to improve the eco-efficiency of the manufacturing plants. In terms of raw material cost, HPPL is working towards bringing the input cost as low as Uflex Ltd.’s, one of its leading industry competitors. HPPL is planning to achieve this with the help of supply-chain optimisation activities that would focus on nurturing relationships with current as well as prospective suppliers. By far the Company has been successful in reducing the cost slightly as compared to previous years.

SWOT Analysis

Strengths

- Strong Presence: HPPL is a leading converter in the domestic flexible packaging industry with a strong manufacturing base all over India. It has dominated the industry with its diversified range of products.

- Strong Parental Support: HPPL is backed by the parent company “Huhtamaki Oyj” which is focused on enhancing and bringing new products in the market. Parent’s strong presence in more than 35 countries has given HPPL vast international exposure.

- Product Differentiation: Superior technology-driven manufacturing plants, better designing capabilities, innovations and strong parental support have helped the Company in creating and sustaining market differentiation along with providing a competitive advantage in the global market.

Weaknesses

- High Customer Concentration: Top 10 clients of HPPL contributes to more than 60% of the total revenue, which is a huge concern as any changes in this client list may severely hamper the profitability of the Company. Hence, client retention is a vital component of the Company’s business in order to maintain its revenues.

- High dependence on the FMCG Industry: Around 90-95% of the revenue is derived from the FMCG industry. Any slowdown in this industry might have a huge impact on the earnings of the Company. During the recent COVID pandemic, the FMCG industry has been running on lower capacity than usual thus, slashing the demand for flexible packaging. Currently, HPPL’s growth is highly dependent on the recovery of the FMCG industry.

- Debt-based Acquisitions: From the past acquisitions by HPPL, it shows how aggressively the Company is willing to expand their business. It is predicted that the Company will keep following the acquisition strategy to eliminate its competitors which might result in, rise in debt.

Opportunities

- Huge Untap Market in Southern part of India: The recent strategic acquisition of MPPL has allowed HPPL to improve its agility in Southern India. The acquisition has provided more advanced product portfolios such as cold seal laminates, peelable films, and collision shrink films. The Company is expecting to tap the flexible packaging market in Andhra Pradesh and other regions in South India through sea routes by leveraging the acquired MMPPL’s manufacturing site in Sri City, Andhra Pradesh.

- Growing demand: The increasing demand for packaged foods due to its safety and easy to carry feature has provided humungous opportunities to the flexible packaging industry by offering products that could serve the end consumer need. As discussed earlier, COVID-19 will also play a huge role in the rising demand for safe and hygienic products.

Threats

- Highly Competitive Sector: The flexible packaging market in India has numerous players in the unorganised sector and very few in the organised sector. Due to the highly competitive nature of the industry, the Company has not been able to increase its margins.

- Environmental Regulations: HPPL’s product portfolio includes a significant number of plastic products and due to increasing environmental concern, the Company can be forced to shut down its plastic products segment or can face certain sale restrictions as the flexible packaging takes time to disintegrate.

- International Exposure: Almost one-fourth of the Company’s revenue is generated from exports, and thus any changes in the foreign policies might hamper the Company’s revenue drastically.

Michael Porter’s 5-Forces Analysis

Barriers to Entry

- Huge capital investments are required to set up flexible packaging manufacturing plants. HPPL has a competitive edge over other players in respect of having superior technology-driven manufacturing plants at 18 strategic locations throughout India. Huhtamaki Oyj, being a major stakeholder in the Company, is expected to inject heavy capital for the expansion of HPPL in India, thus, raising funds won’t be a problem for HPPL as far as eliminating competitors is concerned.

- Product differentiation is one of the most crucial parts in the flexible packaging industry and one has to keep experimenting and creating new products in order to survive, for which high investment in R&D is required. HPPL has two R&D centres, located at Thane and Khopoli in Maharashtra.

- Flexible packaging industries are prone to comply with several regulations due to high exposure to plastic products, any unfortunate ban of plastic products could severely hamper the Company’s overall sales or it could even lead to the shutdown of businesses.

Bargaining Power of Suppliers

- The raw material used in the process of manufacturing flexible products are fairly standardized and less differentiated. Moreover, the number of suppliers catering to this industry are more than the buyers, so the suppliers are required to quote reasonable prices and hence, have a low bargaining power.

Bargaining Power of Buyers

- The flexible packaging industry is highly fragmented and thus, puts pressure on the profitability of the Company. Even though there are very few companies who cater specifically to the FMCG and pharmaceutical sector, there is intense competition among them, which restricts pricing flexibility. Thus, giving less scope for bargaining to buyers.

Rivalry among Competitors

- The flexible packaging industry is highly competitive & around 60-65% of the market is unorganised. There are several unorganised players in the sector apart from a few organised players like Uflex. Therefore, price competition exists among competitors. Due to the competitive nature of the industry and the presence of both organised and unorganised players in the sector the rivalry among competitors is significantly high.

Threat of Substitutes

- Innovations and product differentiation are the most vital element in the packaging industry, and HPPL never disappoints in this aspect. They have a list of advance product portfolio which helps them stand out in the industry.

Branding & Other Initiatives

- Branding – Huhtamaki Oyj

HPPL has strong backing from its parent company Huhtamaki Oyj, which completed its 100th anniversary in the year 2020. Huhtamaki Oyj is a pioneer in the flexible packaging industry and has its presence in more than 50 countries. HPPL being a trusted brand can leverage the expertise, network, experience, knowledge and technology of Huhtamaki Oyj to expand its business and increase exports in the near future.

- Innovation and R&D program like NASP

Innovation programs like NASP (New Applications, Structures, and Products/Processes) enables the Company to develop new products, moving in new geographies and helping them retain its technology leadership in the market by creating improved packaging solutions. The HPPL creativity program, called NASP is one of the major drivers of growth for the Company. The Company maps the sales of NASP products introduced into the market and calls these NASP sales. During CY19, the average NASP sales contribution to the overall sales was around 23-25%, helping to drive growth. The first NASP objective is building a new business by finding new applications and markets for existing layouts and technology processes. The second objective is to introduce new packaging products and structures and technology processes not just for new applications and markets, but also to offer new technically superior solutions which add value to the brand being packaged, or, importantly, solutions which provide cost advantage without compromising performance. Hence, the NASP exercise builds a new business, but most importantly, it also protects or even improves existing business share from a customer by creating improved packaging solutions, or improving cost competitiveness.

- Creating a Circular Economy

With rapidly growing environmental consciousness, every third customer in the industry prefers eco-friendly products. Supporting the change, HPPL has improved the eco-efficiency of the manufacturing plants and the sustainability of its offerings. HPPL has taken steps such as usage of renewable sources, improving carbon footprints through energy-efficient technologies, maintaining the highest safety standard and performance of products. The Company has installed rooftop solar power at most of its facilities which have reduced power cost as well as reduced 20MT of CO2 emissions annually (equivalent to planting 1 lakh trees).

Flexible packaging offers the best in class food protection while on the other hand recyclability of such packages is more difficult. To tackle this problem, HPPL has launched its recyclable solution called “Huhtamaki Blueloop”, another step towards creating a circular economy and supporting a robust waste management ecosystem that democratises recycling and creates a net positive impact on our ecology. In 2019, HPPL has commercialised recyclable solutions for shampoo, confectionery, industrial bulk packaging, and snacking applications, and are ready with many more.

Financial Analysis

- Significant increase in Profit Margins

The net profit margin declined from CY15 to CY17 due to the excess debt taken by the Company to acquire Positive Packaging Industries Limited (PPIL) along with the several capacity expansion plans undertaken during the same period. During CY18, the Company raised additional debt to complete the acquisition of one of its biggest competitors Ajanta Packaging Limited, which helped HPPL to expand their presence in the labelling business. In CY19, the Company repaid a huge portion of their debt liability and also benefitted from the reduction in tax rates, which helped HPPL improve its margins drastically.

- Cash-Rich Company

The Company is in the expansion phase where they are focusing on eliminating competitors and increasing their presence in the domestic as well as in the international market. From past acquisitions, the Company has excessively increased its revenue throughout the years. During CY17, the Company had constructed two factories in Assam and Sikkim and had undertaken other capacity expansion projects at various other plants, due to which the Company’s FCF stayed in the negative territory for two years. Apart from this, the Company has an impressive cash reserve.

- Moving towards the Vision of Building a Debt-Free Company

The Company has always maintained a low debt to equity ratio. As we can see in the graph, the curve is following a continuous downward trend. The high debt to equity ratio in CY15 due to the reasons mentioned was a time when the Company raising debt significantly to acquire PPIL and carry out capacity expansion projects at the Silvassa plant and other geographies as well. These expansion plans were running across from CY15 to CY17. The Company kept on raising and paying back a portion of the loan as and when they were due without default, however the total debt kept on increasing due to several acquisitions and expansion plans. In CY19, the management had fulfilled their promise of repaying non-convertible debentures (NCDs) which constituted 32% of their total debt, which subsequently improved the debt to equity ratio.

CRISIL has reaffirmed the ratings taking into account the prepayment of NCDs worth Rs.385 crore on December 20, 2019, which was raised to fund the acquisition of PPIL and it believes HPPL has a comfortable financial risk profile and holds a strong market share in the flexible packaging industry.

- Dividend-Paying Company and Growing EPS

The EPS for CY19 was Rs.22.52, which was very high as compared to Rs.4.62 in CY18, the reason being a huge chunk of the debt which was raised to acquire PPIL (one of HPPL’s biggest competitor) was repaid back which lead to the rise in PAT figures and thus, increasing the EPS. The Company has paid a dividend of Rs.3 per share of the face value of Rs.2 each, for CY19. Considering the need to conserve its financial resources during the current economic slowdown consequent to COVID-19 pandemic, the Management revised its previous dividend recommendation of Rs.5 per share for the CY19 to Rs.3 per share.

Risk Analysis

- High Volatility in Raw Material Cost

HPPL’s key raw materials include inks, films, solvents, and adhesives. Films account for almost 50% of the total input cost, while inks, adhesives, and solvents account for 20%. The prices of these raw materials are linked with crude oil prices. Thus, exposing the firm to risk associated with volatility in crude oil prices. Currently, material cost constitutes around three-fourth of the Company’s total cost.

- Forex Risk

HPPL’s export contributes around 20% of the total revenue and it also imports a lot of raw material as well. Thus, exposing the Company to forex gains/losses.

- Regulatory Risk

The Company deals with flexible packages which are very difficult to dispose of and due to increasing environmental issues, the Company is exposed to regulatory risk. Any adverse regulatory changes will affect the Company’s margins.

Corporate Governance

- The Company’s board consists of 6 directors out of which 2 were Executive directors and 4 non-executive directors. There are 3 independent directors, including a woman director. The composition of the Board is in line with the requirements of Regulation 17 of the Securities and Exchange Board of India (SEBI) LODR.

- There are no inter-se relationships amongst the Board members and neither of the Independent Directors has any material pecuniary relationship or transactions with the Company, Promoters, or the Management.

- Independent Directors of HPPL, Mr Murali Sivaraman is an Independent Director at Bharat Forge Limited and ICICI Lombard, Ms Seema Modi is a Director at Trent Hypermarket Private Limited and an Independent Director at SEAMEC Limited, and Mr Ashok Kumar Barat is a member of the Board of Directors in 7 other companies. However, none of the other directors of the Company holds directorships in any other company.

- During the year, nine meetings of the Board of Directors were held and one meeting of Independent Directors was held as per the SEBI’s Listing regulations.

- Remuneration paid to Independent Directors and Non-executive directors were within the limits prescribed under Companies Act, 2013.

- A Familiarisation Programme for Independent Directors has been put in place wherein an orientation program has conducted that incorporates familiarisation with the Company, their roles, rights, responsibilities, nature of business, companies strategy, business plan, etc.

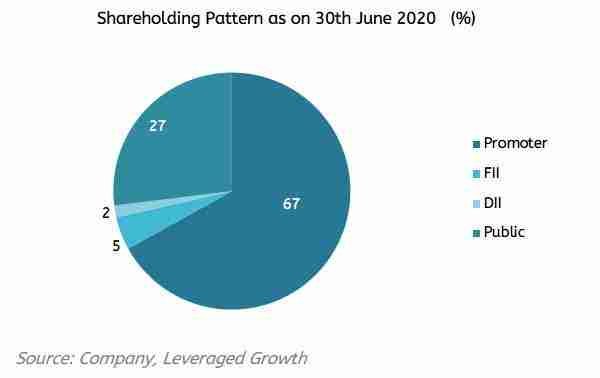

- Promoter’s total holding remains constant at 66.94%, out of which none of the shares are being pledged.

The EndNote

- The Company is expecting to have a high operating cash flow in CY20 due to the recent acquisition of MMPPL’s flexible packaging business, which has opened several opportunities in the southern part of India.

- With low debt levels, the Company has the potential to take risks and even raise funds if required. Huge untapped potential lies within the flexible packaging segment for India.

- HPPL, being one of the leading flexible packaging company in India, is growing at a massive rate and with the support of its parent, Huhtamaki Oyj, the Company is all set to capture the Personal protective equipment (PPE) market with their new products in the loop such as “Huhta Face Mask” and “Protective Face Shield” (which are already released in some countries).

- Moving forward, as HPPL deals in primary consumer packaging for essential commodities like food products, personal care, home care, pharmaceuticals thus, the Company won’t have major issues in respect of losses occurring due to lockdown. Unlike others, COVID-19 could be a boon for the flexible packaging industry, the demand for hygienic and safe packed foods will take a boost in the coming years. Being in the consumer packaging segment, the Company is shielded up to an extent from any slow-down in the economy.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Vikas Tiwari

Research Desk | Leveraged Growth