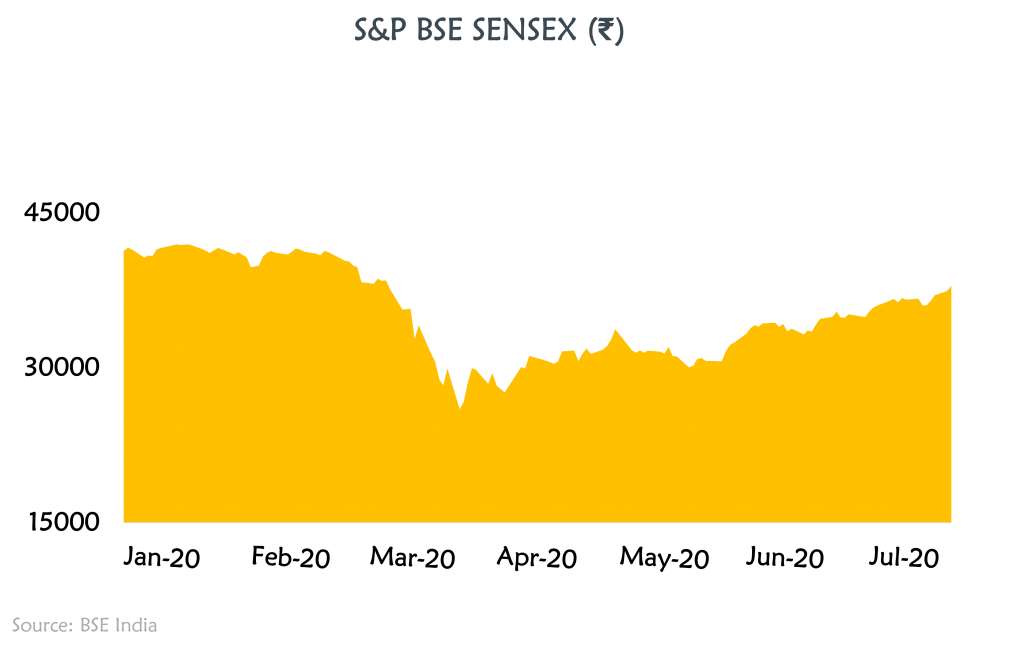

The economy has leapt into a depression in most of the world, yet stock prices are moderately down in most markets. According to the World Bank, the global economy is facing the worst recession since World War II and it is anticipated that the economic growth will decline by 5.2% in 2021. Manufacturing activities in India reached a record low of 22.4% in March 2020. According to the Federation of Indian Chambers of Commerce and Industry (FICCI), the Indian GDP growth forecast for 2020-21 is expected to be -4.5%. Even when the global economy is facing such severe deterioration due to COVID-19 the stock markets are booming, creating opportunities for those at the top of the economic pyramid to make a fortune when billions of people are losing their means of livelihood. Analysis of stock market data shows, between March 2020 and June 2020 the BSE SENSEX rose by 19.35%. This brings us to a crucial conclusion that “Markets and Economy are not the same.”

Signs of Disconnect between Economy and Stock Market

During the COVID-19 pandemic, numerous nations across the world resorted to lockdowns to “smoothen the curve” of the contamination. These lockdowns were intended to confine millions of citizens to their homes, shutting down businesses and terminating nearly all the economic activities. India was among the nations with one of the strictest nationwide lockdowns and this action severely impacted the economy.

India’s unemployment rate reached a record high of 23.5% in April and May 2020 as a consequence of subsequent lockdowns due to the COVID-19 pandemic which forced the business to shut down their operations and cut their workforce. The worst-hit sectors were aviation, automobile, and real estate. According to Bloomberg, about 4 lakh aviation workers have been laid-off or furloughed due to the coronavirus. According to the estimates given by MyHiringClub.com and Sarkari-Naukri.info, more than 60,000 jobs have been slashed so far, and around 2 lakh employees are expected to be laid off due to the coronavirus crisis. According to a report by KPMG, a loss of ₹ 1 lakh crores is estimated to the real estate sector by the end of FY21.

The IHS (Information Handling Services) Markit India Manufacturing PMI (Purchasing Managers’ Index) plunged to 27 in April’20 from the previous 52.5 in Mar’20 due to sudden nationwide lockdown. A reading above 50 indicates a growth of the manufacturing sector compared to the preceding month, a reading below 50 signifies a shrinkage of the manufacturing sector and a reading equal to 50 signifies no change.

The stock market experienced a deep dive on 23rd March 2020 when the Hon. Prime Minister Shri Narendra Modi announced the nationwide lockdown which extended for 65 days. Analysis of stock market data shows, between March 2020 and June 2020 the BSE SENSEX rose by 19.35%. Since then the stock market has rallied upwards without any significant downward deflections, baffling investors about the disconnect between the economy and the stock markets. The reasons why there is a disconnect between stock markets and the economy are discussed in the coming section.

Reasons for the Disconnect Between the Stock Market and the Economy

Stock Prices Reflect Far Future

Warren Buffett once said that if you aren’t comfortable holding a stock for 10 years, you shouldn’t own it for 10 minutes. Stocks signify a proportion of ownership in a company that should normally harvest value for decades into the future. Therefore, stock prices reflect expectations for the far future and the impact of a bad year or two average out if subsequent years are promising. As a result, investors refrain from marking down stock prices even if the company is facing awful circumstances believing that the following years shall still be good.

Stock Market Indices

Economic recessions particularly have severe consequences for smaller companies, which generally do not have the same pliability as larger firms. This affects stock prices, as there is a strong relationship between the size of the company and the stock’s overall performance in the market. For example, the top three stocks of the BSE SENSEX – Reliance Industries Limited, HDFC Bank and Infosys Limited – accounted for 43% of gains in the index price between March 23 and June 12 2020. This shows that the stock market indices are more weighted towards larger and stable companies as compared to small and riskier companies which are more severely damaged by the economic downturn. Hence, investors’ faith in such stable companies with such high weightage has been the driving the market upwards.

Lower Bond Yield Make Stocks Attractive

Central banks push down interest rates to stimulate the economy. As a result, government bond rates in developed countries become significantly lower than in the pre-pandemic period. E.g. on 12th May 2020, the US 10-year Treasury yield was only 0.70% whereas the dividend yield on the S&P 500 was at 2%, thus making it hard for long term investors to reallocate stocks to bonds. It is important to understand that lower interest rates on bonds make them less attractive compared to stocks, thus increasing the demand for stocks and therefore their prices.

Monetary Relief

India’s 20 lakh crore COVID-19 relief package added a tremendous amount of liquidity to the economy which increased investor confidence and therefore, resulted into increased stock purchase owing to the belief that markets would benefit from the relief package as a whole.

The Market Hates Uncertainty More Than Bad News

On 8th May 2020, the US labour statistics figures showed that over 20 million jobs were lost by U.S. workers in April due to COVID-19 disruption. At the same, time S&P 500 futures gained 1.7% intraday, as the numbers were below market expectations of 22 million.

Implications for Policy Makers

Emotions Cloud Reason

Humans are bound to emotions and so news about the next year or so can fluctuate share prices significantly but this doesn’t mean that a faster or a slower economic recovery has a significant impact on underlying share prices. Therefore, politicians, as well as policymakers, should be careful about interpreting indicators from the stock markets and should not commit the mistake of believing that stock markets represent the economy as a whole.

Disproportionate Ownership of Shares

The wealthiest 10% of American households own 84% of all stocks whereas the bottom 90% own 16% of all stocks. The US billionaire wealth surged to $584 billion, or 20%, during the pandemic, between 18th March and 17th June 2020. Shares are disproportionately owned by the wealthier people and therefore the policymakers should understand the imperative to focus aid on those who need it the most. For example, the wealthier investors try to manipulate the stock market movements with the help of the large inventory of stocks and funds they hold. They constantly try to maintain stock prices in their favour by deliberate buying and selling of stocks and thus influencing the sentiments of weaker stock market participants. Relatively strong stock market prices create a narrative that the wealthier are escaping without much damage, while the poor are being hammered by the recession.

Share Prices Affect Economy Indirectly

Investors’ opinion of their prosperity and spending capability are influenced by stock prices. When stock prices are in a rising trend, i.e. a bull market, the economy tends to be surrounded by a great deal of optimism regarding the prospects of the stock market. If companies issue new stocks to raise capital, they can deploy those funds to hire more workers, invest in new ventures, or even expand current operations. The bull market tends to increase investors’ confidence in the stock market while generating more wealth. This confidence spills over into increased expenditure in things like real estate, automobile, consumer durables, etc. thus resulting in increased revenue for corporations and further boosting GDP.

Do Not Overreact

As discussed in the above point that stock prices do influence consumer confidence, but policymakers should refrain themselves from overweighing the significance of market movements. For example, the stock prices of dominant IT firms like Tata Consultancy Services Ltd. (TCS), Infosys, Wipro, etc. are sharply up while the movement of sectors such as airlines, automobiles, hotels, and restaurants have witnessed significant declines in their respective stock prices. It would have been a mistake to treat the recent Indian stock market returns to near peak levels as an indicator that no further policy actions are needed to deal with the devastating impact of coronavirus recession which has handicapped the travel and hospitality sector.

Contributor: Harshil Ghatalia

Research Desk | Leveraged Growth

I am an engineering graduate from Gujarat Technological University (GTU), Ahmedabad and currently pursuing MBA Finance from Pandit Deendayal Petroleum University, Gandhinagar along with CFA Level 1 from CFAI, USA. I am a sports enthusiast with state and national level exposure in Basketball. I have special interests in geopolitics, macro-economics and martial arts. I firmly believe that suffering the pain of discipline is much better than suffering the pain of regret. I’m an ardent learner who aspires to find a solution for every problem by employing my creative and analytical bent.