There was always a deal on the table. Work hard, spend little, defer everything, and one day, after enough sacrifice, you’d arrive somewhere worth the wait. Most people took that deal without reading the fine print. Gen Z read the fine print. And a lot of them decided it wasn’t worth signing.

This isn’t a story about a generation that’s bad with money. It’s a story about a generation that looked at the traditional financial playbook, ran the numbers on their actual lives, and concluded the playbook was written for a world that no longer exists. What they’ve built in its place is still being named: ‘Soft Life.’ ‘Soft Saving.’ ‘Financial Nihilism.’ The labels keep changing. The underlying logic doesn’t.

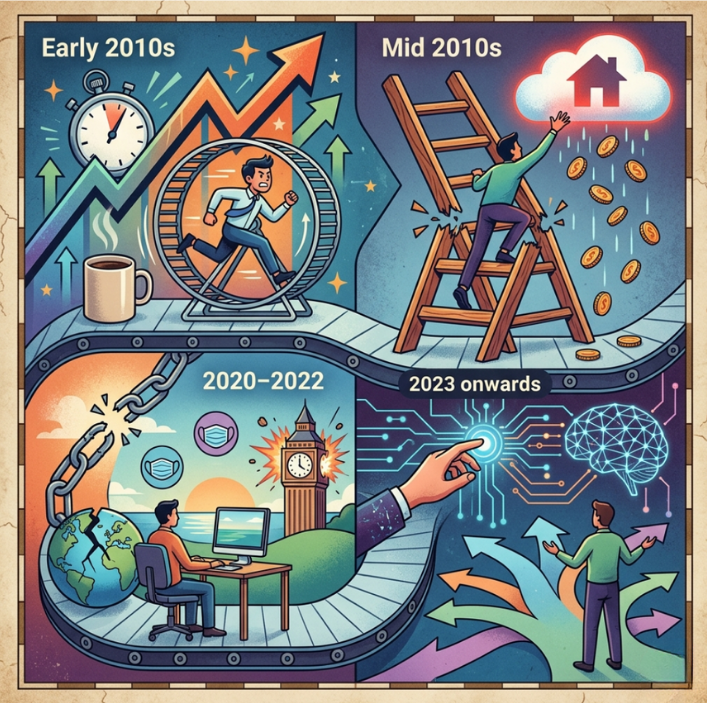

The Shift Unfolded: A Brief, Honest Timeline

This shift didn’t happen overnight. It was assembled from a series of very public disappointments, each chipping away at the idea that patience and sacrifice reliably lead somewhere good.

● Early 2010s: Hustle culture peaks. The gospel of grinding, 4 AM routines, monetise everything, sleep when you’re dead, sells the idea that sheer effort is the only gap between you and success.

● Mid 2010s: The ladder starts wobbling. Entry-level salaries stagnate. Housing prices in every city worth living in begin compounding faster than any starting salary can chase. The ‘climb’ becomes more expensive and less rewarding simultaneously.

● 2020–2022: The pandemic breaks the illusion. Job losses, remote work, and a sudden confrontation with mortality reshape what ‘work’ means. The corporate track loses its grip on identity. Burnout gets its clinical definition.

● 2023 onwards: AI enters the stability conversation. The careers that young people were told to build toward are visibly in flux. Planning thirty years ahead for a role that may not exist feels less like prudence and more like guesswork.

By the time Gen Z enters the workforce in numbers, the deal has been renegotiated so many times that it barely resembles the original. The response isn’t rebellion. It’s a recalculation.

Three Ways This Generation Changed the Rules

The shift isn’t just financial. It’s semantic. The words haven’t changed, success, wealth, ambition, security, but what they point to has moved significantly.

| Success | Used to mean: | Now means: Owning your schedule. Work that fits into life, not the other way around. |

| Wealth | Used to mean: | Now means: Time wealth. Experiences that can’t be inflated away or market-corrected out of memory. |

| Security | Used to mean: | Now means: Portable skills. Flexibility. A safety net just thick enough to survive a bad quarter. |

None of this is irresponsible on its face. A generation that defines wealth as time and security as flexibility isn’t delusional, they’re responding to an economy where traditional wealth is harder to build, and traditional security is harder to find.

Soft Saving: The Myth of the ₹300 Coffee

For years, personal finance advice leaned heavily on the ‘latte factor’, the idea that if you skipped your daily coffee, those compounding rupees would eventually build a house. It became the dominant parable of financial self-improvement, repeated in every budgeting guide and money podcast ever made.

Gen Z finds it insulting. Not because they don’t understand compounding, they do. But because the math on a flat in any major Indian city makes the latte irrelevant. A down payment in Mumbai or Bengaluru requires a decade-plus of aggressive saving and considerable market luck, on a starting salary that hasn’t kept pace with the cost of reaching that starting point.

| Wage growth, urban India (last decade) | ~6–7% annually, Salaries have grown, but not at the pace that matters for wealth accumulation |

| Urban property price growth (last decade) | ~10–14% annually. The gap between income and property prices has widened every year for a decade |

| Inflation on everyday spending | Persistent, compounding. The cost of living now is not the cost of living when the financial advice was written |

So they soft save. They keep a basic emergency fund. They maintain enough liquidity not to drown in a bad month. But the surplus, the money that previous generations shoveled into fixed deposits and endowment plans, gets redirected toward things with an immediate, guaranteed return: a trip that changes your perspective, a course that builds a skill, a wellness practice that makes the rest of life feel manageable.

The reframe: Soft saving isn’t ‘no saving.’ It’s a shift from asset accumulation to life accumulation, the deliberate collection of experiences, skills, and moments whose value doesn’t depend on market conditions or a retirement date.

When Pragmatic Turns Into “Meh, Whatever”

There’s a harder, more honest version of this story that most soft-life content refuses to engage with. Some of what looks like intentional living is exactly that. But some of it is driven by something closer to resignation, a growing belief that the traditional financial future is not just difficult to reach, but essentially inaccessible.

| “If the traditional milestones are out of reach anyway — why deny yourself the present to chase them?” | |

| What feeds the belief→ Parents’ retirement funds wiped out in market crashes→ Older siblings doing everything right — and still struggling→ AI disrupting careers before they’ve been built→ Climate anxiety is making long-term planning feel absurd→ Housing prices are compounding faster than any salary | The logic it produces→ The only guaranteed dividend is the one you enjoy today→ Saving for a future you don’t trust feels irrational→ Experiences can’t be taken by a market correction→ Time is the only currency you can never earn back→ Flexibility beats accumulation in an uncertain world |

The problem with financial nihilism isn’t the emotion behind it, the emotion is earned. The problem is that uncertainty is not directional. The same unpredictable world that makes saving feel pointless also means you might live to 85 with no pension and rising healthcare costs. Nihilism as a response to systemic failure is understandable. As a forty-year financial plan, it’s a gamble with slow consequences.

The present is the only thing guaranteed. That’s true. It’s also true that ‘the present’ eventually includes being 70.

So… What Is Worth Focusing On Now?

The soft life isn’t without consequences, and the honest version of this conversation has to hold both things at once. Rejecting hustle culture was right; it was extractive, it overpromised, and it treated human beings as productivity machines with occasional maintenance windows. The soft life as a philosophical corrective makes complete sense.

But there’s a version of soft saving that’s genuinely intentional, a light safety net, experience-first spending, and a clear plan to scale financial contributions as income grows, and there’s another version that’s just deferred anxiety dressed up in wellness language. The difference between them isn’t visible from the outside. It’s whether the safety net ever actually thickens.

Time is the only currency you cannot earn back. Gen Z understood this early on, and they’ve built a philosophy of life around it. The question, the one worth sitting with, is whether ‘don’t waste the present’ and ‘don’t ignore the future’ are actually opposites, or whether someone who’s thought carefully about both ends up living quite differently from someone who’s only thought about one.

The most rebellious act in 2026 isn’t aggressive saving. It isn’t spending everything either. It’s deciding, with full awareness of the trade-offs, exactly what your money is actually for.

Disclaimer

This blog is for educational and informational purposes only and does not constitute investment or financial advice. Please consult a SEBI-registered financial advisor before making investment decisions.

Contributor: Team Leveraged Growth