And What It Means for Your Portfolio

India once led the world with a bold, principled idea that a newly independent nation could refuse to bow to either Washington or Moscow. Non-Alignment gave Nehru a global stage and India a moral authority far beyond its GDP. Fast forward to 2026: India is buying discounted Russian crude, negotiating a trade deal with the US that reportedly demands upfront concessions from India, quietly patching ties with China for commercial reasons, and simultaneously sitting in the QUAD, BRICS, I2U2, and the SCO. This isn’t idealism. This is pure, unapologetic pragmatism.

Foreign policy is no longer a diplomat’s abstraction. In a world where trade IS coercion and tariffs ARE weapons, every deal India signs, or refuses to sign, lands directly on your portfolio.

From Vishwaguru to Deal-Maker

India’s External Affairs Minister Jaishankar once said India is not ‘unsentimentally transactional’, a careful phrase that acknowledges the shift while retaining a veneer of relationships. But the architecture has changed. The old Non-Alignment framework was built for a bipolar world and a multilateral rules-based order. Both are now decaying. The US has withdrawn from 31 UN institutions. The WTO’s dispute mechanism has been paralyzed since 2019. UNSC reform remains a pipe dream.

What has replaced it is ‘multi-alignment’, simultaneous, issue-specific relationships with all major powers, without committing to any single camp. QUAD for security and tech. BRICS for economic multipolarity. I2U2 for infrastructure and clean energy. Voice of the Global South for soft power. This is not indecision; it is deliberate optionality. In a transactional world, dependence is vulnerability.

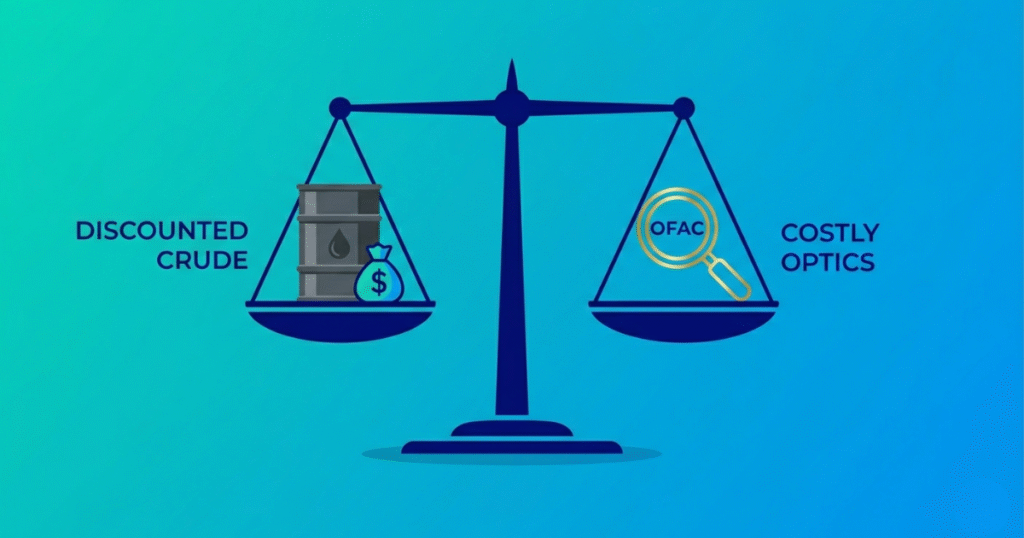

The Russia Trade-Off: Cheap Crude, Costly Optics

Russia, which had barely featured in India’s oil import basket before 2022, now accounts for a significant share of India’s crude imports, a purely economic decision that protected the margins of IOC, BPCL, and HPCL and kept fuel inflation in check. But the US Treasury’s OFAC sanctioned 21 Indian entities in October 2024 for facilitating Russian transactions. Washington is beginning to price in India’s hedging.

▸ India-Russia crude imports: Surged from near-zero to a leading share of India’s import basket (2022–2025)

▸ Russian arms share in India’s imports: 36% pre-2022 (SIPRI) — now being systematically reduced

India’s defence pivot away from Russia towards the US, Israel, and France, and domestic manufacturers, is a 10–15 year journey. The listed beneficiaries are already reflecting it in their order books: HAL, BEL, Bharat Dynamics, and Paras Defence.

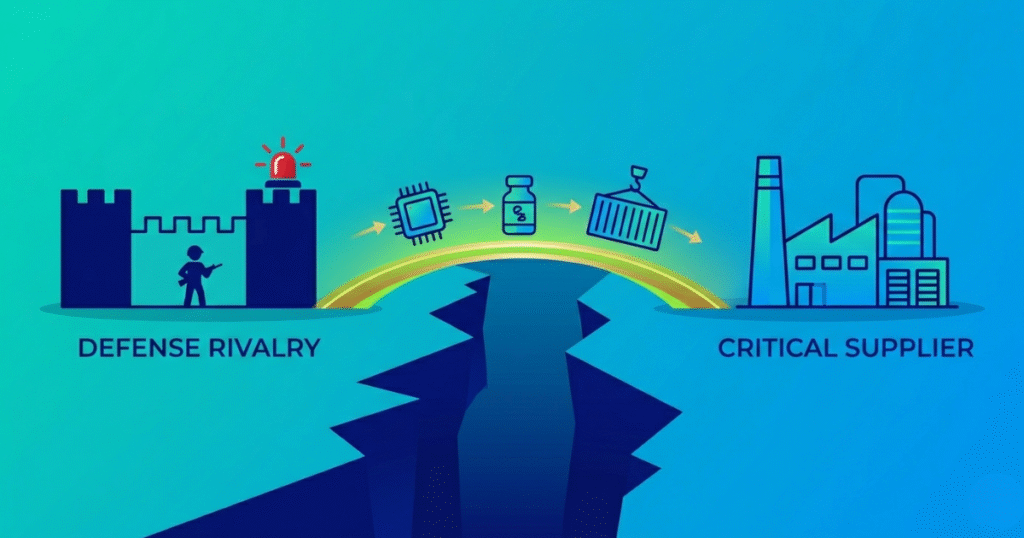

The China Paradox: Rival, Supplier, Reluctant Partner

India bans hundreds of Chinese apps. Soldiers clash at Galwan. And yet — India’s trade deficit with China hit $99.2 billion in FY2024, and in early 2026, New Delhi relaxed FDI norms for Chinese companies. In October 2024, Modi and Xi met for the first time in five years. By August 2025, Chinese FM Wang Yi was in Delhi, facilitating trade, flights, and investment flows.

▸ India-China trade deficit (FY24): $99.2 billion — India’s largest bilateral deficit

▸ India exports to China (FY26 YTD): $15.88 billion — up 38.37% YoY

India needs Chinese supply chains for electronics, pharma APIs, and consumer goods. A complete decoupling is off the table. India is managing this relationship purely on commercial terms, sector by sector. The investment angle: Dixon Technologies, Amber Enterprises, and Kaynes Technology in electronics; Divi’s Laboratories and Laurus Labs in pharma, all stand to benefit from India’s push to reduce import dependence while staying commercially engaged with China.

The US Tariff Shock: When Transactionalism Cuts Both Ways

Despite being a QUAD partner, India was hit with a 25% US reciprocal tariff in 2025. The India-US interim trade agreement reportedly demanded ‘concessions first’, requiring India to double industrial imports from the US before receiving any relief. The financial fallout was immediate.

▸ Net FDI (Apr–Oct FY26): $6.2 billion, with September and October turning negative

▸ FPI flows (Apr–Dec 2025): Net outflow of $2.9 billion vs. a $2.7 billion net inflow in the prior year

▸ MSCI India P/E: 25.6x vs. Emerging Markets average of 16.4x, a premium that requires geopolitical delivery

India’s valuation premium is partly a bet on its China+1 positioning. If that positioning falters, through tariff escalation or diplomatic friction, that premium compresses. Track monthly FPI flows; they are the real-time scorecard.

What This Means for Your Portfolio

India’s transactional foreign policy creates clear winners and pressure points across listed markets.

Tailwinds — Defense electronics, semiconductors (Micron’s Gujarat unit, Tata Electronics assembling iPhones), renewable energy (44.51 GW added in 2025, nearly double the prior year), and IT/GCC services all have structural support from India’s QUAD and minilateral positioning. PLI scheme beneficiaries in these sectors are particularly well-placed.

Headwinds — Export-dependent sectors facing US tariff risk: textiles, generic pharma exporters, gems & jewelry. Companies with a high concentration of US revenue warrant closer scrutiny. India’s $108 billion import bill from China in FY26 also underscores the depth of manufacturing dependence; any deterioration in ties would spike input costs.

Wildcards — The India-UK CETA (signed in July 2025, offering UK duty-free access to 99% of Indian exports) and the India-EFTA agreement (signed in March 2024) unlock new export earnings for IT services and pharma. The BRICS digital currency initiative, if India actively supports it as BRICS chair, could reshape cross-border payment rails for Indian exporters.

The Reality Check

Being in QUAD while being in BRICS. Buying Russian oil while selling to a sanctions-imposing US. Welcoming Chinese FDI while banning Chinese apps. These contradictions are manageable — until they are not. The risk is not that India picks a side. The risk is that no side fully trusts India, and deals become harder to close on India’s preferred terms.

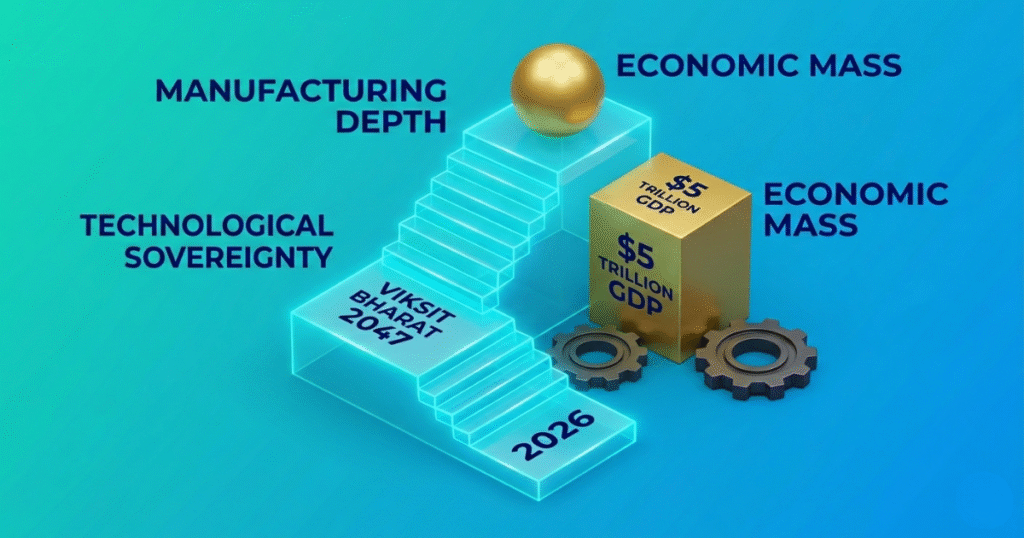

PM Modi’s acknowledgment in the Rajya Sabha that the world order is shifting — and that India must formulate a ‘new national identity and approach to international relations’ — is the most honest framing of the challenge. India is transitioning from a balancing power to an aspirational Third Pole. To succeed, it needs economic mass: a $5 trillion+ GDP, manufacturing depth, and technological sovereignty. That is the Viksit Bharat 2047 vision. Every geopolitical move India makes today is buying time and building that mass.

As an investor, your job is not to be a diplomat. It is to identify which sectors ride this tailwind, and which face the turbulence. The map above is your starting point.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice. All valuation and correlation figures should be independently verified. Past market behaviour is not indicative of future results.

Contributor: Team Leveraged Growth