Click here to download the report

Key Highlights of Redington Ltd.

- Due to a significant rise in IT products, the Company saw its highest-ever revenue of ₹62,731cr, representing a 10% YoY increase

- The channel partners have increased to 39,500 in FY22 from 33,950 in FY21, and leading brands increased from 235 brands in FY21 to 290 brands in FY22

- The Company recorded its highest-ever PAT growth of 69% in FY22

- Redington India became a net debt-free company in FY22

Indian IT Industry

- The Indian IT hardware market is expected to reach a production objective of $300bn by 2026

- The consumer PC market grew by 44.5% in FY21 with 14.8mn in sales

- In the Union Budget of FY23, the government announced some significant digital developments, such as further digitization in banking, higher education, the health sector, and government administration, helping the IT industry

- The total end-user spending on information and risk management in the enterprise is projected to reach $2.08bn in FY22, an increase of 9.4% from FY21

- Industry forecasts predict that India’s consumer digital economy will touch $800bn by 2030, registering 10x growth from FY21

Three Decades in IT Industry

Redington Limited (NSE: REDINGTON) is one of the most trusted and leading IT solutions providers for information technology, cloud, telecom, lifestyle, solar verticals, and mobility across more than 38 emerging markets, including 60 subsidiary offices. It provides end-to-end supply chain solutions for all categories of IT products like PCs, computer spare parts, software, etc. Further, it offers Consumer & Lifestyle products like digital printing machines, entertainment products, telecom, and digital lifestyle products. With a portfolio of more than 290 brand associations and 39,500 channel partners, it is changing the ecology of distribution and supply chains by combining technological adoption and innovation. Redington Limited group has three main subsidiary companies: Redington India, Redington Middle East & Africa, and Redington Singapore. The Redington group is maintaining a market leader position in all operating markets. Its wholly-owned subsidiary in India, ProConnect (a logistics service company), serves pan India and various countries in various industry sectors as a partner for a full value-added range of Third-Party Logistics (3PL) supply chain solutions. Established in 1993, the Company has constantly moved up the distribution value chain to become one of India’s best Technology & Mobility distributors. It also maintains its position as the top distributor in the Middle East and Africa.

Journey

Redington India Limited was incorporated on May 2, 1961. In 1994, operations commenced for IT products with the distribution of Epson, Tripp Lite, and the distribution of Samsung monitors in Northern India. A year after, in 1995, Redington began its operations in Eastern India. The Company also started distributing Compaq and Philips products in the same year. In 1996, it created the distribution of Intel products. Moreover, it made a tie-up with Microsoft to distribute software products in 1997 and tied up with IBM APC and Canon to distribute their products in 1998. It was also ranked as the Best Distributor in India for 2002-2003. By entering the consumer durable distribution area in 2005. For the distribution of Apple products in India, they signed a distribution agreement in 2007 and a distributor and Licensing Center partnership with Adobe in 2008. However, in 2019, they pivoted towards becoming a Solution Oriented Distributor of Machine Learning (ML) and Artificial Intelligence (AI). In FY21, Redington divested its shareholding from its wholly-owned subsidiary M/s. Ensure Support Services Limited. Additionally, ProConnect, the subsidiary of Redington, acquired full ownership of Auroma Logistics as a subsidiary.

Key Personnel

Mr. Raj Shankar, former Managing Director of Redington, served for almost 17 years. Under his leadership, Redington transformed from a single-product and single-country organization to the emerging market’s $7.7bn multinational behemoth. He envisioned and carried out the growth of Redington into several markets in the Middle East, Turkey, Africa, and South Asia regions. He developed the plan that has been the cornerstone of Redington’s enormous success in the META region. However, Mr. Rajiv Srivastava was re-designated as Managing Director, leading to Mr. Raj resigning from the Company on May 21, 2022.

The Indian IT Industry

Redington operates in the computer peripherals industry, which is expected to grow at a CAGR of 6%. The global industry is expected to reach ~$1217bn by FY32 and is set to reach $443.3bn in FY22. The rapid change in the industry is why companies invest in newer products and solutions. The industry is growing due to the increasing demand for hardware devices, the introduction of innovative technical products, and rising per capita income; adding to this, the prices of consumer peripherals products are also reducing.

The Indian consumer IT sector saw a growth of 44.5% in FY21, with 14.8mn of total units sold. The consumer business includes Personal Computers (PC), which include notebooks, workstations, desktops, etc. The notebooks category sales stood at 11.6mn, and desktops sales saw a rise of 30% due to higher demand from small and medium businesses, consumers, and enterprises. Further, the spending in the enterprise information security and risk management end-user is projected to reach $2.08bn in FY22, an increase of 9.4% from FY21. The growth was a result of the hybrid working model of companies. Companies are heavily investing in data security and privacy to reduce data breaches and create a security wall. Globally the computer peripheral industry is divided into submarkets by products, end users, connectivity, and geography. The industry globally is divided into two segments commercial & residential. Among these two segments, the commercial segment was the largest and accounted for more than 50% of the market share globally in FY21. The residential segment is also picking pace as the online education industry is rising, driving the market in FY22. Some of the leading players in the industry are Apple, Epson, Dell, Samsung, Microsoft, Intel, etc. Moreover, Redington has partnered with all, contributing to the Company’s major revenue.

The geographical landscape is an important factor to consider in the computer peripheral industry. As North America has the largest market share in the global computer peripherals market compared to all the countries around the globe. The demand for computer peripherals is rising in the US and other countries like the Middle East, Africa, Europe, China, Canada, India, the UK, etc. The main reason for the uptrend of the industry is the early adoption of sophisticated IT products like machine learning, artificial intelligence, robotics, etc., in the commercial space. Additionally, e-education and remote work are rising post-pandemic, due to which the demand for retail space is also increasing.

Business Model

Redington follows a direct sales model wherein it is involved in selling directly to the customer. It is a supply consolidator between IT manufacturers and thousands of IT channel partners. Redington purchases products in bulk from the vendors and sell them to the resellers/sub-distributors/system integrators and retailers on a principal-to-principal basis. The Company mostly makes its purchases in cash to avail cash discounts instead of buying goods on credit to stay in the competition. The cash discounts availed help improve its profit margin, which is generally very thin because of the nature of the distribution industry. However, large Indian corporates and small & medium business houses favor purchasing from the distribution channels more than the vendors. As corporate houses make bulk purchases, the distribution channels offer them hefty discounts, which vendors cannot provide, and therefore, it will be beneficial for both corporates and small & medium enterprises. It has a diverse market share in the computer peripheral industry and operates both in India and overseas. The various revenue-generation business model is helping Redington to grow faster than its competitors.

The Company has organized its business into two main segments:

- Volume Business: The products falling under this category are generally high-volume & fast-moving products such as Samsung monitors, HP peripherals, Intel CPUs, Seagate Expansion hard disks, etc. Since the brands are well established, demand generation is through vendors, whereas the distributor acts as a liaison. The volume business requires stocking across branches and a considerable amount of capital.

- Value Business: High-end & high-value products fall under this category. These products are sold as an entire package to corporates, which requires a complete IT solution. The selling cycles are longer, and many solutions require products from various brands. This category mainly includes products for networking from brands such as CISCO, Tyco, Systimax, and products for high-end storage such as IBM, HP, and EMC, and brands such as Mcafee, CA, Sybase, etc.

It provides distribution services, while its subsidiaries complete it by offering services like logistics. This makes Redington a one-stop shop for its customers.

Subsidiaries

As of FY22, Redington had two Indian and two overseas subsidiaries in Mauritius and Singapore, respectively. It forayed into the logistics, pharma, and FMCG business via the ProConnect subsidiary to increase business efficiency. Later, to consolidate all its business, the Company merged its subsidiaries, like Auroma Logistics Pvt Ltd, into the ProConnect business to operate as a single entity. The overseas subsidiaries saw a shift in the business from hardware to software, subscription, and services. These evolving dynamics prompted the subsidiary to re-strategize its market focus which impacted the business opportunities in Singapore but opened up new avenues in the distribution business for India.

The Singapore subsidiary partnered with the globally leading tech innovators who helped it to introduce complex IT systems that can automate and modernize operations in India. It caters to the country’s top and most reputed & leading brands.

SWOT Analysis

Strengths

- Strong Portfolio

Redington India offers supply chain solutions to over 245+ international brands in IT and Mobility spaces, serving over 38 emerging markets for the last 28+ years with 70+ offices globally.

- Wide Product Range

The Company offers a bunch of IT products like scanners, peripherals, printers, packaged software, PC components, high-end servers, etc., through multiple vendors. Moreover, it also supplies mobile handsets. This comprehensive range of products helps Redington achieve economies of scale with low raw materials costs and provides its customers with a single sourcing point.

- Broad Reach & Superior Logistics

India is a vast country, which makes the delivery of products challenging to reach every location in the country. Leveraging its 200+ warehouses, Redington makes it easier for its products to be delivered to every corner of the country.

- Early Investing in Emerging Technology

Redington enjoys the first-mover advantage due to its commencement of operations post-liberalization, privatization, and globalization of the Indian economy. In the 1990s, the technology distribution sector was not explored, and the Company moved into it to secure its place in the industry.

Weaknesses

- Declining Market Share

Despite the increase in revenue, the market share of Redington is declining. The Company could focus on the computer peripheral industries, owing to its fast growth.

- Growing Competitors

The computer peripherals industry is a fast-growing business in India and globally, and the competitors can easily replicate the business model of Redington. To overcome this issue, a platform model could be created to integrate suppliers, vendors, and end-users.

- Cyber Security Risk

As the Company is catering to the IT industry, it is prone to hacking, as cyber security is widespread today. The risk of hacking is increasing as the world shifts toward high-tech technologies and data sharing. These rising technologies pose a major threat to the IT industry today, making it difficult for players to operate safely.

Opportunities

- Government Support

Government and PSUs are digitizing the economy, making them significant buyers of IT products and services. The back-end office and use of public interface functions require the latest technology. Moreover, India’s digital economy could contribute 18-23% of the overall economic activity.

- Online Market

The usage of online services is increasing, and the Company can take this opportunity to provide new offerings to consumers and create a strong customer network.

- Domestic Collaboration

To expand its international presence, the Company can use the opportunity to team up with local players, which can bring a global process and execute expertise on the table.

Threats

- Changing Political Environment

Due to the recent pandemic and the Russia-Ukraine war, Redington’s threat of doing business in domestic and international markets has increased.

- Shortage of Human Resources

With increasing dependence on innovative solutions and high employee turnover, Redington faces a shortage of skilled laborers.

- Short Supply of Semiconductors

An integrated circuit chip used in the computer peripheral and the automobile industry is facing a supply shortage globally. Due to this, the industry is facing a shortage in production and cannot meet the demand on time. This issue is hitting all the players in the industry, including Redington.

Differentiating Strategies

Dynamic Business Model

The business analyzes all decisions and evaluates each circumstance taking into consideration the methods and necessities of the business. It requires a strong understanding of social, economic, technological, and ecological dynamics. As a result, the business adopts, evolves, interacts, and eventually takes the lead with the ability to navigate with the signals from the external world.

Future Ready Mindset

The Company is aware of the new emerging consumer purchasing behaviour changes, thereby evolving services-based business models and technology adoption in every process step. It plans to be able to get ready for the future and disrupt the market with technology and new business models.

Technology Led Initiatives

Redington is investing its time and capital to build a cutting-edge platform to create a future-ready infrastructure and services for its customers and stakeholders. Effectiveness comes from the digital workspace, operations, confidence, satisfaction, & loyalty from the digital customer experience. Digital business models disrupt and reshape the market appropriately.

Global Presence

The strategy of inorganic growth and expanding its business globally have led to a vast network. It operates in India and other countries like Turkey, the Middle East, Singapore, Africa, and other South Asian Countries compared to its peer, which is concentrated in India and Singapore only. This has helped Redington have a global presence and a robust system of distribution of IT products to create a moat around the Company.

Michael Porter’s 5 Forces Analysis

Barriers to Entry

The Company regularly adjusts its strategies according to customers’ preferences to make their lives easier. Redington India invests in R&D continuously to safeguard from competitors. The threat to entry is relatively low to moderate.

Bargaining Power of Suppliers

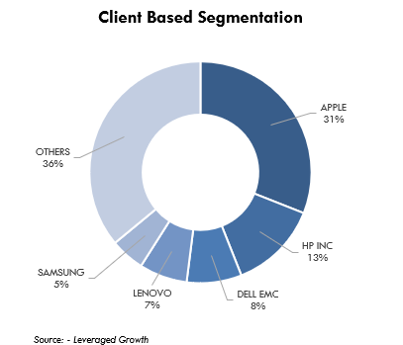

The Company has five major suppliers, Apple, Samsung, HP, Dell EMC, and Lenovo, contributing to the major part of revenue, thereby having strong bargaining power. This will impact its potential to maintain above-average profits in the Computer Peripherals industry.

Bargaining Power of Buyers

The buyer’s bargaining power seems to be low to moderate. The Company offers the top global brands like Apple, Samsung, Hp, Dell, etc., which are the most demanded in the retail and commercial segments. Due to this, Redington has the upper hand in this area with higher bargaining power.

Rivalry Among Competitors

Competition in the IT industry is intense, which makes it difficult for new businesses to enter. As the competition among the existing players increases, the scope for higher profits will also be blurred.

Threat to Substitutes

Due to the rapid shift in consumer behaviour and technological advancement in the industry, consumers can quickly shift to competitors. This poses a threat to the Company, therefore making the threat of substituting moderate to high.

Branding & Other Initiatives

- Redington India has established a brand image of “Brand behind Brands,” which signifies the Company’s motive of working with top brands worldwide while growing the Redington brand.

- The Company had a remodeling of its brand in FY18. It launched a new brand logo and tagline. The logo signifies synergy and how the organization believes in oneness with its consumers, vendors, partners, and other stakeholders to create an everlasting relationship. Adding new shades of green to the logo symbolizes the portfolio of businesses it is venturing into and diversifying its operations.

- The tagline is “Seamless Partnerships.” This tagline perfectly fits the Company as it has 38,350+ channel partners. Maintaining such partners is not easy, and Redington does it smoothly.

- The brand strategies help the Company differentiate itself from its brand partners. It needs to create a brand image that people can treat separately from its partners as a distribution firm. Earlier, its marketing strategies were driven only by vendor objectives, but now it markets its brand partners and the Redington brand along with the vendor objectives.

- The brand ProConnect was a logistics, transportation, and warehousing company when it was launched. However, as time passed, the Company merged several other businesses to consolidate its other businesses, and now ProConnect is also serving in the Pharma, Auto, FMCG/FMCD, Hi-Tech, etc.

Financial Analysis

1. Revenue

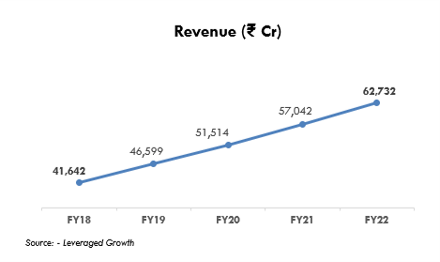

The Company reported a double-digit growth of 10%, which stood at an impressive figure of ₹62,731.60 cr in FY22 compared to ₹57,041.60 cr in FY21. Its revenue has been growing at a CAGR of 9.6% for five years. The pandemic has accelerated the trend of companies opting to pursue a cloud-first architecture, where they consider the cloud their first option for new components and migrating existing systems.

The increased adoption of the hybrid work culture across the country, increasing demand for personal computers in emerging markets, and the global commercial demand remained strong throughout most parts of the year, despite the supply chain disruptions in the market. FY22 has been a critical year with the re-emergence of the COVID-19 pandemic, shortage of microchips, and non-availability of components causing a significant delay in the supply of IT products. The Company registered strong growth despite the challenges due to the buoyant IT market.

2. EBITDA

The EBITDA grew significantly by 30.6% during FY22 to ₹1,879.20 cr as compared to ₹1439.10 cr in FY21. The Company saw a CAGR of 16.8% over the past five years. EBIDTA growth is substantially higher than revenue growth due to better margins and improved operating leverage. Its gross margins grew by 19.6% (6.2% of revenue) during FY22 compared to the previous year (5.7% of revenue). The gross margin rate in India remained flat at 5.7% in FY22, and the Overseas Gross margin increased to 6.5% in FY22 against 5.7% in FY21. The increase is due to the enterprise segment’s significant business performance and the higher volume of business growth in the African segment.

3. Profit after Tax (PAT)

Redington registered its highest-ever PAT of ₹1279.90 cr in FY22 compared to ₹758.30 cr in FY21. The Company reported a rise of 69% in PAT with a CAGR of 22.5% over the past 5 years. Moreover, Profit Before Tax (PBT) saw a growth of 43.8% because of a one-time tax payment of ₹89 cr in FY21. The PBT grew due to an increase in its EBITDA levels and less interest paid due to debt repayment. As a result, PBT as a % of revenue increased from 2.0% to 2.6% of revenue in FY22.

4. Dividend

The Company proposed a final dividend of 330%, i.e., ₹6.60 per share, whereas the dividend for the previous year was 580%, including a special dividend of 200% of the face value. The current year dividend was the second highest compared to FY21. It also issued bonus shares in the ratio of 1:1 per equity share of ₹2 each, and the record date for the bonus issue is August 20, 2021.

5. Return on Capital Employed

The Return on Capital Employed (ROCE) increased in FY22 to 28% compared to 19.9%in FY21. Higher operational profits due to effective global working capital management resulted in greater ROCE in the Company’s book. The EBIT also improved in FY22, pushing the ROCE to greater heights. The Return on Equity (ROE) also saw a rise in FY22 to 24.1% compared to 16.4% in FY21.

Environmental, Social, and Governance

Environment

Redington is working towards a green and clean environment for the future aligned with climate change. The Company is solving this problem by renovating four village ponds which increased the water storage of 12,000 cubic meters and water catchment by 36,000 kilolitres. Further, it also constructed 3 model biogas plants, 16 community wells, and six rainwater harvesting structures with a new water storage capacity of 52 kiloliters. This has increased the water inflow and groundwater at respective villages, enabling villagers to access water all year round for domestic consumption and agriculture. Moreover, an alternative to biofuel was introduced to reduce fossil fuel usage, and biogas plants were constructed in five villages in Tamil Nadu.

Social

The Company has undertaken several projects to enhance higher education in India. Its major focus is on training and equipping the unemployed youth to avail of job opportunities and lead a financially independent life. It provides training on SCM skills and basic computer skills, and so far, it has trained 100 youth, of which 20 were differently abled. It assists in developing and strengthening infrastructure for children’s education by improving functional literacy and numeracy among children. These children are also improving their basic reading, writing, and arithmetic skills for classes six to eight. So far, 1800 students have benefitted from this initiative.

Governance

The Company’s Board comprised nine directors, of which two were Executive Directors, two were Non-Executive Directors, including one woman Director. Furthermore, there were five Independent Directors, including one woman Director constituting 20% of the Board’s strength

In the last 3 months of FY22, the foreign institutional holding has decreased by 0.65%. It declared a Final Dividend at the rate of ₹6.60 per equity share of the face value of ₹2 for FY22 in its meeting held on May 27, 2022, with approval of the shareholders at the AGM of the Company. Moreover, the major shareholder of Redington, Synnex Ltd., is an industry leader in IT distribution, supplying full-service integration and technological solutions, and is involved in the logistics business.

Risk Analysis

Redington India identifies its primary risks under three broad categories: Inventory Risk, Receivable Risk, and Currency Risk. It deploys adequate mitigation measures and management oversight to safeguard stakeholders’ value. Moreover, it has developed a dynamic business model that ensures it remains ahead of the competition in the ever-changing technological environment. It has been able to reduce its exposure to geographic risks, product and technology obsolescence, and over-dependence on a specific vendor and product. Further, the diversification of its product categories and brands, presence in numerous markets, and ongoing enhancement of reach and expansion of the business line. The diversified product categories and brands, alongside the presence in multiple markets and continued enhancement of reach and expansion of the business line, have helped to grow the business.

Inventory Risk

The inventory risk of the Company is high because it is into distributing and trading products. It takes marketing support, stock rotation, prudent provisioning, and price protection to mitigate this risk. Due to these measures, the provision for inventory over the past ten years has been set at 0.04% of sales.

Currency Risk

The Company operates in India and also globally. It has partnered with brands from all over the world and is exposed to high currency risk. It is implementing measures to mitigate this risk. In India, ~84% of purchases are made in rupee-denominated invoices, and for the remainder, a forward cover is offered, and the premium is added to COGS. In the Middle East and Africa, currencies are pegged, transactions are denominated in USD, borrowing in local currency, and effective control of forwarded transactions. These measures have enabled continuous operations irrespective of currency rate fluctuations.

Receivable Risk

It has a receivable risk due to the B2B model in which products are purchased in bulk and mostly on a credit basis. The credit risk is a financial loss to the Company if a customer or counterparty fails to meet its contractual obligations, which arises principally from its receivables from loans, customers, and other financial assets. It mitigates this risk through strict receivable management and policies. The credit risk is restricted to 15% of the receivable value. The concentration of credit risk is limited due to the large and unrelated customer base.

End Note

The IT industry in India and globally is on an uptrend as post-covid scenarios have changed the world entirely. Companies, organizations, and governments are making massive infrastructure investments to ensure they can modernize and automate themselves. So the investment and consumption-led scenario is playing out to the Company’s advantage. Redington is confident ––of leveraging the uptrend in the industry and is trying different strategies to keep up with the industry peers.

Will Redington be able to maintain its market leadership in the future?

What is the business model of Redington Ltd?

How has Redington Ltd performed financially in recent years?

What are the key partnerships and collaborations of Redington Ltd?

How does Redington Ltd ensure a sustainable and ethical supply chain?

What are the growth opportunities and challenges for Redington Ltd in the future?

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting

and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative product as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged growth, its associates, their directors and the employees may from time to time, effect or have affected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, Country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays

Contributor: Team Leveraged Growth