Click here to download the report

Key Highlights

- Lux Industries Limited registered revenue of ~₹2,300 crores in FY22

- The business is increasing its multi-channel footprint and targeting newer geographies

- Interest coverage was maintained at around 29.48x in FY22

- The company is concentrating on widening and deepening its distribution systems to make products easily available

Industry Innerwear Industry

- In 2021, the innerwear market was projected to be valued at ₹32,000 crores or ~9% of the domestic fashion market

- A substantial number of small-scale firms dominate the innerwear sector, making up 60–65% of the unorganized sector

- Long-standing players in the innerwear market in India include companies like Amul, Lux, Rupa, and Dollar, whose presence is increasingly more noticeable in Tier-II and III cities

Lux Industries- Fashionable on the Inside

Lux Industries Limited (NSE: LUXIND) is one of the country’s largest innerwear and outerwear producers. Lux offers over 5000 SKUs (Stock Keeping Units) across a wide range of products. Moreover, it is the top exporter of innerwear in India and is ranked first in India in terms of volume.

It operates under 16 key brands while maintaining relevance for people of various ages, regions, genders, and seasons. Lux Cozi and Venus are the highest revenue-generating brands contributing to 37% and 28% of the total revenue, respectively. Lux Cott’s Wool and Lux Inferno cater to winterwear, whereas brands like Lyra and Karishma focus on womenswear. In addition to these power brands, it has consistently enriched and expanded its product line in new market segments like GenX for casual wear.

The brands under Lux Industries are mentioned below:

Renowned for its innovative and customer-demand-driven product offerings, the company aims to double the market share of its brand, Lux Venus (focusing on menswear and kidswear), in the Indian innerwear market. The company operates in India, serving domestic and international needs, and owns Artimas Fashions Private Limited, a wholly-owned subsidiary.

Lux has become a prominent player in the industry by ensuring superior customer satisfaction, developing top-notch products via innovation, and maintaining the highest ethical standards in its business dealings. In India’s hosiery industry, Lux has been one of the most persistent brand builders and has consistently invested significant amounts of its branding revenues. Additionally, it has emerged as the cost leader by operating at one of the lowest costs throughout the industry, driving operational excellence.

Journey of Lux Industries Ltd.

Indian Innerwear Industry

The innerwear sector has expanded its horizons over time, evolving from an essential commodity to a fashion accessory focused on comfort and styling. Rising earnings, discretionary expenditure, and the working women population, coupled with growing fashion consciousness among millennials, have altered the domestic market for undergarments. Therefore, manufacturers and companies emphasize developing a product range that caters to the current customer’s needs.

To ensure that their unique positioning translates into a retail connection with customers, organized players have heavily invested in creating expertise around design, fit, sourcing, and channel presence. This has fueled the market’s transition from the unorganized segment to organized goods. Additionally, the innerwear category’s distribution channel is more varied and balanced, allowing for more favorable terms of trade for the branded player.

The industry has developed brands supported by celebrity endorsements, elevating the entry barrier. Moreover, innovative brand communication was used to highlight individual businesses employing modules and fixtures for product display, eye-catching packaging, and point-of-sale images. The market for men’s innerwear was estimated to be worth ₹110 billion in 2018 and is anticipated to increase at a CAGR of 7% in the following ten years, reaching ₹218 billion by 2028. Women’s innerwear makes up most of the innerwear market in India, accounting for over 66% of the entire market.

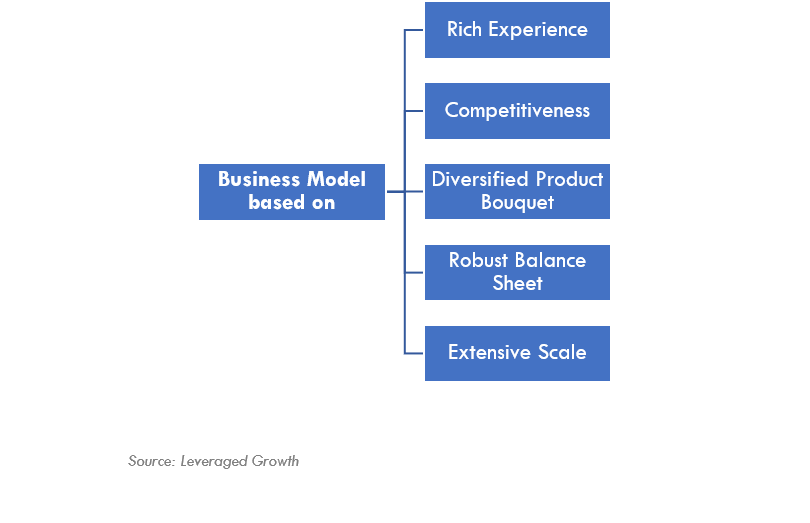

Business Model

1. Products

The Company manufactures and markets knitwear and undergarments for premium, mid-premium & economy segments, selling shirts, boxers, vests, and briefs. The product line also extends to shorts/pajamas, sleepwear, activewear, thermal wear, racerbacks, camisole straps, and slips.

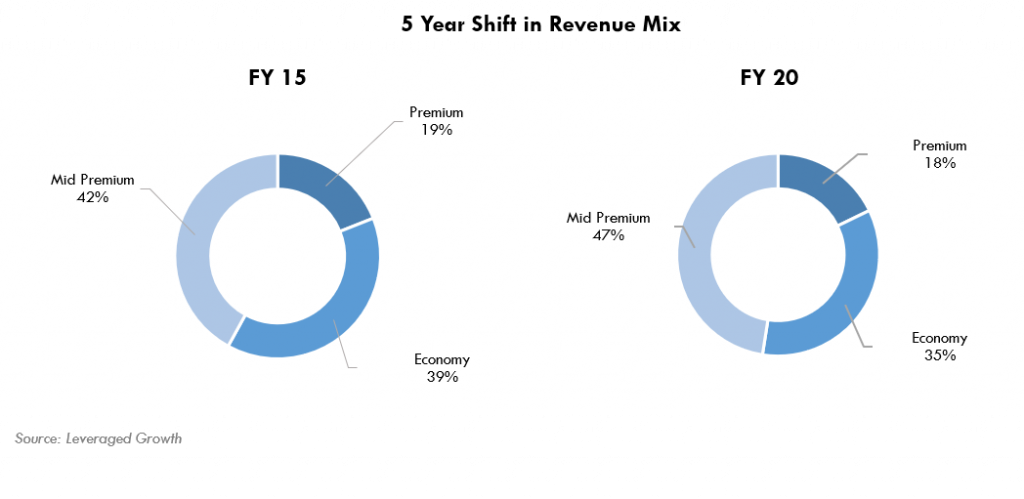

The volume growth for the premium segment was stable, while the growth for the mid-premium and economy segments was 5% and 9% YoY, respectively. Revenues increased by 26% YoY for 9M FY22 due to robust demand growth across all product categories.

The women’s apparel portfolio, which is mostly unexplored by branded companies, is also experiencing a positive trend for the company. Lyra, a women’s clothing brand, contributed 13% of total sales in 9M FY22.

2. Distribution Channel

The company has production facilities in Kolkata (West Bengal), Tirupur (Tamil Nadu), and Ludhiana (Punjab). In India, it has seven manufacturing facilities and more than 1,150 dealers. Due to its 100% internal production facility and as none of its goods are outsourced, it has robust control over the value chain. Additionally, it uses a variety of independent distributors and merchants to become easily available to its target audience. The company has more than 950 distributors in India, 160 large-format stores, and nine exclusive brand outlets.

3. Global Presence

Lux is constantly pushing its boundaries while upholding its unwavering commitment to quality. It has a well-established Pan-India presence with major sales from states such as MP, UP, and Uttarakhand. Moreover, it also has a robust export market and serves in more than 47 countries, and has generated 7% of its revenues from exports in 2021-22.

4. Merger

Lux Industries merged with two other group companies in March 2021 through a non-cash deal. GenX, a men’s athleisure brand owned by J M Hosiery & Co Ltd, and Lyra, a women’s leggings brand owned by Ebell Fashions Pvt. Ltd. LUX issued 4.8 million new equity shares in the merger as a consideration for the merger that resulted in a 16% equity dilution. The Company’s number of outstanding shares climbed to 30.1 million, and its FY20 EPS after the merger was ₹66.91 as opposed to ₹48.66 before the merger.

SWOT Analysis of Lux Industries

Strengths

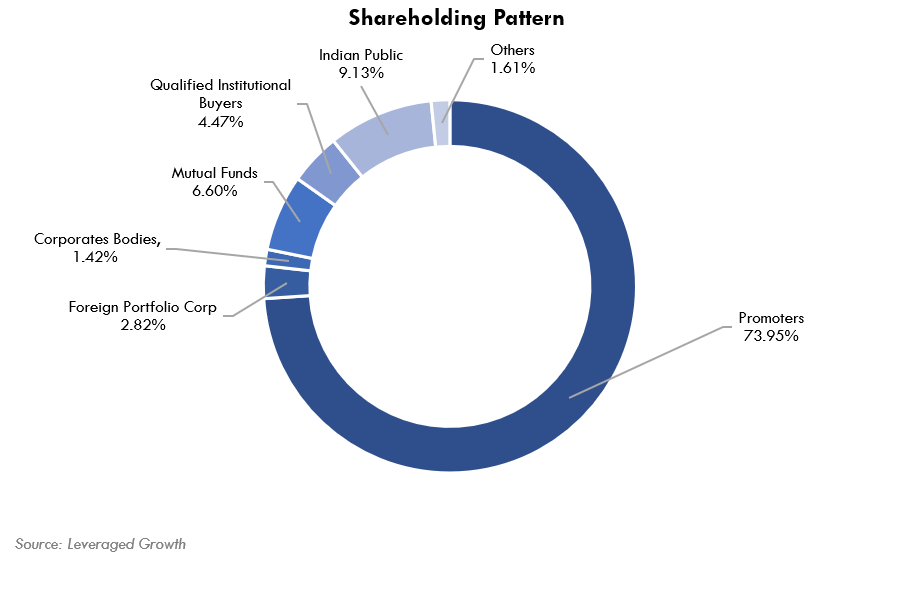

- LUX holds a dominant position in India’s branded innerwear market, with a market share of ~15% in the organized sector. The company’s well-established operations and management track record have aided in the development of positive relationships with its distributors and suppliers.

- Constant launch of innovative products for all ages, locations, and seasons. It offers more than 100 items for men, women, and children. Lux Venus, Cozi, Inferno, Cott’s Wool, ONN, Lyra, and GenX are some of its key brands.

- More than 950 exclusive distributors are currently part of the company’s extensive nationwide distribution network and presence in over 4.5 lakh retail locations. Over the years, Lux has successfully engaged several renowned Bollywood celebrities to endorse its brands that evoke strong emotions in viewers.

- To control quality and cost, Lux focuses on in-house manufacturing. All its high-end work is carried out in-house.

Weakness

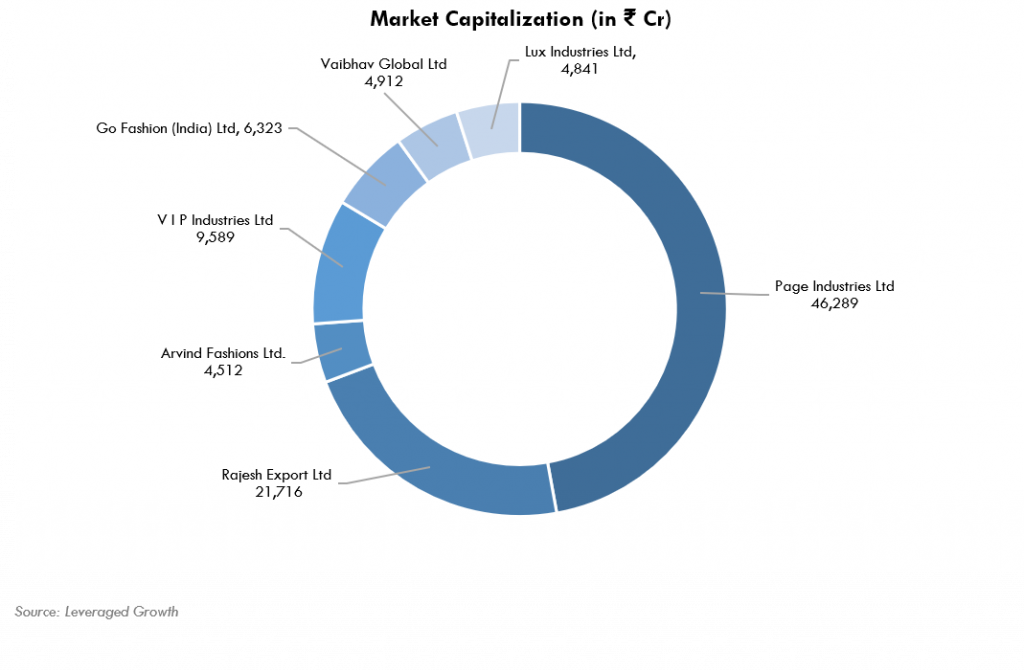

- Compared to its rivals, Lux industries have obtained lower margins. One of its top rivals, Page Industries, has achieved its sales goal of ₹1,255.02 crores, an increase of 15.78%, while Lux’s sales have increased by 1.84% to ₹631.45 crores.

- With a large majority of its sales coming from Madhya Pradesh, Uttar Pradesh, and Uttarakhand, the company has maintained a strong presence in western and central India. However, it has not been able to effectively position its product in the southern region of the country.

- Following SEBI’s ban on 14 entities for insider trading, Lux Industries experienced a 20% plummet. Although the company denied the allegations, such occurrences may lead to operational and reputation risk.

Opportunities

- With increasing disposable income, Indian customers are becoming more aspirational and fashion-conscious, increasing demand for contemporary patterns and fuelling growth in the maternity and innerwear market.

- Possibility of offering a range of goods across the nation by utilizing their effective distribution network. More than 600 distributors, 10,000 wholesalers, and more than 3 lakh retailers make up a robust national network.

- The company has a well-established brand presence in the Middle East, Africa, and Europe and intends to expand its footprint internationally, which may lead to significant advantages.

Threats

- Rupa Industries, Dollar Industries, Page Industries, and VIP Industries have been Luxind’s main rivals in the quest for a greater market segment. Additionally, it faces fierce competition from the unorganized sector of the industry and international brands expanding to India.

- Threat from price variations in the raw materials used in manufacturing, including cotton, yarn, and chemicals, as increasing the final product costs may not be reasonable in a competitive market.

- Innerwear products are considered more of a fashion accessory than a necessity. Being a fashion product, the Company must adapt to the constantly evolving fashion trends in the mass market to remain viable.

Differentiating Strategies

1. Developing a Powerful Brand

Lux has built strong brands in mid and economy innerwear segments with its 16 in-house brands, including GenX and Lyra. Through the years, it has successfully promoted several items and sub-brands. It invests 7-8% of its income in growing its brand. Customers are more loyal due to consistent marketing and branding efforts that have built substantial brand equity.

2. Price & Product Range

It has the greatest pricing range in the business, with more than 100 products available across 15 brands and priced between ₹35 and ₹1,350. Owing to this, Lux also works with all subcategories of the innerwear market and other ancillary items like socks and children’s clothing.

3. Attention to Premium Products

The Company has changed its product line over the past few years by steadily increasing the number of premium products. The Company boosted its brand spending and introduced GenX and ONN for the mid-premium consumer market in response to the shifting demands of the innerwear industry and the growing customer aspirations and spending on fashion, lifestyle, and comfort.

Michael Porter’s 5-Forces Analysis

1. Barriers to Entry

There is a high barrier to entry in this industry. Major manufacturers, including Rupa and Dollar, operate at substantially lower prices and benefit from significant economies of scale. Therefore, to maintain competitive pricing in the market, especially for the economy and mid-premium categories, an organized player will need to manufacture on a large scale.

The industry has developed a strong brand presence by onboarding many well-known endorsers. The industry also needs a strong network of distributors, multi-brand outlets, large format stores, and exclusive retail outlets to reach a larger audience.

2. Bargaining Power of Supplier

The Company performs most of its manufacturing chain operations internally, reducing its reliance on suppliers. The company relies on third parties for a few raw materials, but the dependence is lessened by entering into long-term contracts. The bargaining power of suppliers ranges from low to moderate

3. Bargaining Power of Buyers

Customers in the mid-premium and premium segments are fashion-conscious and are willing to switch to alternatives with greater comfort, better design, and higher quality- at competitive prices. The buyers have greater negotiating power in such a market. Therefore, the buyers of the innerwear industry enjoy high buying power.

4. Threats of Substitutes

The threat of substitutes in the innerwear industry is moderate to high. LUXIND has consistently delivered innovative items and has become a leader in markets such as thermal clothing. However, this industry focuses on product differentiation by developing various brands while offering clients identical product utility.

Every company has recently attempted to launch new brands and goods in the mid-premium and premium categories. As a result, there is a greater risk of substitutes due to the industry’s high intensity of competition.

5. Rivalry among Competitors

Lux industries face intense competition from both organized and unorganized players. The business is expected to develop rapidly, so competitors are trying to maintain a stable price and expand into every product category to gain market share. If competition is fierce, it will be challenging for established businesses like Lux Industries Ltd. to achieve sustained profitability. Considering the above factors the rivalry among the innerwear companies is significantly high.

Branding

1. Impact through Advertisements

Lux heavily invests in advertising through celebrity brand ambassadors to reach customers of all ages, such as Amitabh Bachchan for the mainstream market and Varun Dhawan for the mid-premium market. The amount allocated to advertising campaigns is roughly 7-8 % of the business’s annual revenue.

2. Rapid Evolution

The company has taken steps to prevent brand aging by renewing its brand architecture every two to three years and embracing newer promotional strategies and themes. The brand’s most recent stunt is to revitalize the leadership of the Lux Venus brand in the hosiery market by onboarding a new brand ambassador through the dramatic and exhilarating campaign establishing a solid foothold.

Financial Analysis

1. Revenue

The company reported a revenue of ₹2,312 crores in FY22. Over the last two years, there has been a substantial contribution of outwear to the total revenue. The revenue of the premium and economy segments grew by 36% and 19%, respectively. Premium brands like Lyra and ONN crossed ₹300 crores and ₹120 crores, respectively, helping the revenue increase significantly.

2. Debt to Equity Ratio

Through consistent debt repayments, LUXIND has significantly reduced its Debt-Equity Ratio (D/E) over the years. The ratio of 0.25 for Lux Industries Ltd. implies that less long-term debt is used to operate the company. The company’s D/E Ratio improved from 1.03 to 0.44, mainly due to increased profit, net worth, and debt repayments. However, due to the company’s growing requirement for working capital, the D/E Ratio increased in the last year.

3. Return on Capital Employed

The Return on Capital Employed (ROCE) of the company has decreased over the years. However, following a value-accretive acquisition and organic business expansion, the company reported a 2.26% improvement in ROCE in FY21 to 36.11%. The need to stock up expensive resource inventory contributed to a marginal decline in ROCE by 1.11% again in FY22.

4. EBITDA

The company has shown an impressive EBITDA growth rate over the last five years. EBITDA increased by 33% YoY while the margin expanded by 1.54%. This was largely due to the company’s improved product mix, and long-term and sensible cost optimization decisions. In FY22, EBIDTA and PAT strengthened by 25% to ₹490.27 and ₹338.06 crores respectively because of the distribution and digitalization strategy adopted by the company.

Risk Analysis

1. Intense Competition

The domestic and foreign players in the innerwear market are highly competitive, both organized and unorganized. Margin pressure and market share pressure might result from such heightened competition. However, LUXIND has differentiated itself through its strong brand recognition and affordable production costs to distinguish itself from its rivals.

2. Demographics

Millennials, who make up most of the workforce, appreciate quality and innovative design. However, their style preference also changes rapidly, and the industry must adopt new strategies to stay relevant. Due to their preference for online shopping, having a digital presence is necessary and demands that they keep up with modern standards, practices, and trends.

Another essential consideration for millennial shoppers is sustainability, with a third saying they are more likely to patronize companies that prioritize social responsibility. Companies in the fashion industry must change with time in light of this shift in the marketing demographic or risk losing to competitors.

3. Exports

The Company generates revenues by exporting to more than 46 countries. Due to the possibility of expensive sanctions from export control authorities, it is vital to uphold the obligations arising from legislation, especially export controls. Therefore, keeping up with any changes that may impact the company’s operations becomes crucial, as export laws and regulations change frequently.

Environmental, Social, and Governance

1. Environmental

- LUXIND has a 1 MW rooftop solar panel at the Dankuni (West Bengal) unit, and 40-45% of the total power requirement is addressed through renewable sources.

- The company installed LED lighting systems in the factories to reduce energy consumption and replaced old equipment with more modern, energy-efficient equipment.

- Reduced plastic usage in packaging materials and ensured that 90% of raw materials used were natural fibers.

- Modern processing techniques saved 2 lakh liters of water per day.

- In the course of cutting and manufacturing, more than 95% of the waste produced was recycled.

2. Social

Lux is committed to ensuring safe processes and safe materials are implemented for the benefit of its employees, vendors, and community. The organization has invested in sustainable development and ongoing improvements to manage quality, occupational health, safety, and the environment (QHSE). The company ensures fair access to development opportunities and training in safety, health, technical, and soft skills.

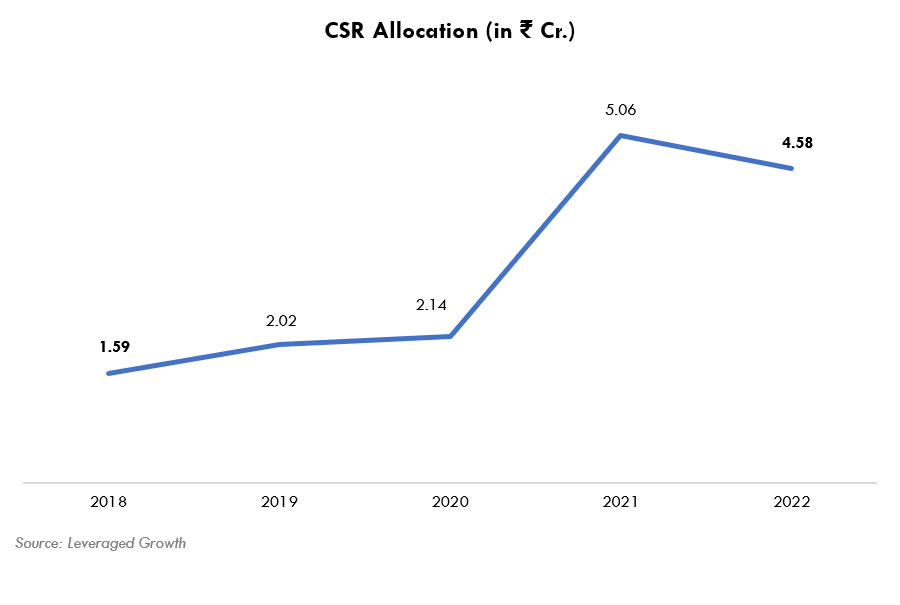

The Company runs its major projects through its foundation and deals with the registered trusts and/or section 8 companies undertaking CSR activities. The Company spent ₹4.60 crores on CSR commitments during the year.

In the financial year Company has undertaken two major projects. One is related to developing one OPD at Tata Medical Centre in West- Bengal. The other is related to supporting the building of a residential school project for over 1,000 underprivileged girls at Joka, West Bengal. Apart from this, Lux is taking the initiative to develop one consultation room at the State of Art Cancer Care Center at Tiruppur to support differently-abled children.

3. Governance

Promoters & Directors manage the company with an average of 24 years of experience in the sector and skills in sales and marketing, brand promotion, product development, board service, and governance. It received no charges of financial irresponsibility; and reported no defaults against payments to creditors, dividends, and statutory dues.

The Board of LUXIND is a mix of executive and non-executive directors. It comprises the Chairman of the Board as an Executive Promoter Director, five Promoter Executive Directors and six Non-Executive Independent Directors. There were no materially significant related party transactions in FY22 that could have a potential conflict with the interest of the Company at large.

Impact of Covid 19

Despite the COVID-19 epidemic, demand for innerwear goods in the economy and their price range remained strong. Revenues increased by 18% to ₹2,312.92 crores during the fiscal year that concluded on March 31, 2022. Additionally, the EBITDA and PAT grew by 25%, to ₹490.27 crores and ₹338.06 crores, respectively.

End Note

Lux Industries has been in the inner-wear and hosiery business for more than six decades and has been expanding its product line and market reach. In the last few decades, innerwear has emerged as one of the fastest-growing fashion subcategories. The changing demographic and expanding youth population, ready to experiment with colors, trends, and fashion, have helped brands grow their current product portfolio and expand their product range.

Considering all these factors, it will be interesting to note whether the Lux industries will cope with upcoming industry trends and retain their market share.

What are the latest developments at Lux Industries Ltd?

How has Lux Industries Ltd performed financially in recent years?

What is the competitive landscape of the innerwear industry in India?

What is the vision and mission of Lux Industries Ltd?

How has Lux Industries Ltd adapted to changes in consumer preferences and behaviour?

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances.

The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment.

The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative product as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged growth, its associates, their directors and the employees may from time to time, effect or have affected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document.

They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the company may or may not subscribe to all the views expressed therein.

This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, Country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction.

The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.