India’s energy transition is no longer just a policy aspiration, it’s a capital-intensive reality. With a net-zero emission target by 2070 and an interim goal of 500 GW of non-fossil fuel capacity by 2030, the country needs trillions of rupees in long-term financing. Enter green bonds, a financial instrument quietly reshaping how India funds its climate ambitions, while attracting global capital hungry for sustainable returns.

What Makes a Bond ‘Green’?

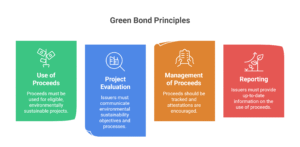

Green bonds aren’t your typical fixed-income securities. While conventional bonds raise capital for general corporate purposes or government expenditure, green bonds earmark proceeds exclusively for environmentally beneficial projects. Think solar farms in Rajasthan, wind turbines off Gujarat’s coast, or electric vehicle infrastructure in Delhi, all funded through instruments traded on stock exchanges.

What makes them “green” is the use-of-proceeds commitment, backed by reporting and disclosures, aligned with global standards like the ICMA Green

How Climate Science Met Dalal Street

In 2007, the Intergovernmental Panel for Climate Change (a United Nations agency) published a report that linked global warming and human activity. It prompted several Swedish pension funds to consider financing projects that contributed positively to the environment.

In 2008, the World Bank issued its first green bond in response to such increasing demand. Since the issuance of the first green bond, the market’s grown considerably.

Today, more than 50 countries have issued green bonds, with the United States being the largest source of green bond issuances.

India joined this green revolution relatively recently. YES Bank issued the country’s first green bond in 2015, raising ₹1,000 crore. But the real watershed moment arrived in January 2023 when the Government of India debuted sovereign green bonds worth ₹8,000 crore, a statement that sustainability had finally moved beyond boardrooms.

The Green Spectrum: Understanding India’s Bond Variants

India’s green bond ecosystem encompasses multiple structural formats, each serving specific financing needs and risk appetites:

By Issuer-

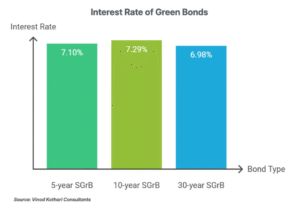

Sovereign Green Bonds are issued by the Government of India for large-scale national infrastructure projects, offering the highest credit quality with sovereign backing. They primarily fund railway electrification, renewable energy grid integration etc., with yields typically ranging between 7.1-7.3% at issuance. Yields typically hover 20-30 basis points below conventional government securities, reflecting lower credit risk and strong institutional demand.

Corporate Green Bonds are issued by private companies to finance their own sustainability initiatives, from solar installations to green manufacturing facilities. Major issuers like NTPC, ReNew Power, Adani Green Energy, and Greenko Group have collectively pushed the market forward, with yields typically ranging between 6.5-8.5% depending on issuer creditworthiness and project risk profiles.

Municipal Green Bonds are issued by city governments or local bodies for urban green infrastructure like public transport, water treatment, or waste management systems. Despite Ghaziabad Municipal Corporation’s pioneering ₹150 crore issuance in 2021 for Tertiary Sewage Treatment Plant replication has been disappointingly slow with very few cities following suit, hampered by weak autonomy and limited technical capacity.

By Structure-

Use-of-Proceeds Bonds represent approximately 85% of India’s green bond issuances, where funds are specifically earmarked for green projects while investors retain recourse to the issuer’s entire balance sheet, blending environmental accountability with conventional credit protection.

Project Bonds are limited to specific green projects with investors having recourse only to that project’s cash flows and assets. These exist sparingly in India, mainly financing large standalone renewable installations where dedicated solar or wind assets independently service debt obligations.

Asset-Backed Securities are backed by pools of already-operational, income-generating green assets like a portfolio of 10 functioning wind farms collectively producing steady electricity revenues. These instruments eliminate construction risk since assets are already operational and cash-flowing.

The Upside: Why Smart Money is Turning Green

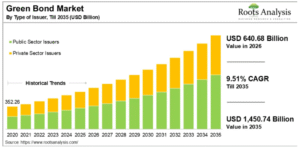

Green bonds offer portfolio diversification into growth sectors, renewable energy capacity in India must increase fivefold by 2030 to meet Paris Agreement targets. This creates sustained demand for capital, supporting bond values.

International investors, constrained by ESG mandates, find Indian green bonds attractive due to favorable yield differentials (7-8% compared to 2-4% in Europe/US), massive renewable capacity addition targets requiring sustained capital deployment, and emerging market opportunities all while India’s improving sovereign ratings (Baa3) enhance overall credit quality.

Transparency requirements, though imperfect, exceed conventional bonds. Issuers must publish annual impact reports detailing carbon emissions avoided or renewable capacity added data that proves to be very valuable to sophisticated investors.

Navigating the Risks

Here’s where it gets complicated. Project execution risk looms large delayed renewable installations or cost overruns can impair returns. The absence of SEBI mandated standardized measurement framework makes cross-issuer comparison difficult.

Unlike several European jurisdictions offering tax breaks on green bond returns, India provides no specific fiscal incentives for investors. The tax treatment mirrors conventional bonds, potentially dampening retail participation.

Liquidity remains thin compared to conventional bonds. Secondary market trading volumes lag, potentially trapping investors during market stress. Interest rate sensitivity hasn’t disappeared either; which means investors might have to tackle both volatility and illiquidity risk.

More troubling is greenwashing, when issuers label bonds “green” without substantive environmental impact. To counter this, SEBI introduced mandatory third-party verification requirements for corporate green bonds 2025. This in turn builds investor confidence and boosts retail participation.

Regulatory pressures present both opportunity and uncertainty. Will SEBI mandate standardisation? Will tax incentives materialize? These unanswered questions create valuation ambiguity.

Powering Tomorrow, One Bond at a Time

India’s energy transition requires $10 trillion in investments through 2070 to achieve net-zero emissions. Green bonds won’t fund this alone, but they’ve established crucial infrastructure demonstrating that sustainability and returns needn’t be mutually exclusive.

As frameworks mature and greenwashing diminishes, these instruments will likely become mainstream portfolio staples rather than niche allocations. For investors seeking returns aligned with environmental preservation, India’s green bond market represents a golden opportunity.

Contributor: Team Leveraged Growth