Click here to download the report

Butterfly Gandhimathi Appliances Limited (‘The Company’ or BGMAL) mainly operates in the domestic kitchen appliances sector and is among the top 5 leading manufacturers. BGMAL enjoys market leadership in South India, with a 25% market share and a 10% market share across India. The Company is involved in manufacturing kitchen products, home appliances, and cookware, including mixer grinders, LPG stoves, pressure cookers, table top wet grinders, and others.

BGMAL caters majorly to the domestic household consumer base and has three product segments:

- Kitchen Appliances

- Cookers/Cookware

- Electrical appliances

How was BGMAL born?

‘Gandhimathi Appliances Limited’ was founded by Late V. Murugesa Chettiar and was incorporated as a Private Limited Company in the year 1986, and later converted into a Public Limited Company in the year 1990. The Company started its business mainly as a trading concern, but in 1867, it started the production of LPG stoves and geysers. While brass was considered the magic metal by everyone, Mr. Chettiar found an opportunity in stainless steel. This helped the Company become a pioneer in stainless steel kitchen appliances in India. It further made them the first acquirer of the ISO-9001 certificate of registration for manufacturing and supply in India. The Company changed its name from ‘Gandhimathi Appliances Limited’ to ‘Butterfly Gandhimathi Appliances’ in 2011 after the merger with its associate ‘Gangadharam Appliances Limited’.

Indian Kitchen Appliances Industry

- According to Statista, the Indian Kitchen Appliances Industry is ranked second among the top five countries in terms of market volume. TTK Prestige Limited, Bajaj Electricals Limited, Stove Kraft Limited, Butterfly Gandhimathi Appliances Limited, Franke Faber India Limited are some of the major players operating in the Indian kitchen appliances market.

- The revenue from the kitchen appliances segment stands at $10,767mn (growth rate of -0.8%) as of 2020, but the sector is projected to grow annually at a CAGR of 5.4% (2020-2025), according to Statista.

- According to IBEF, the Government of India has doubled import duty on most steel items and also imposed measures like anti-dumping and safeguard duties on iron and steel items. The increase in import duties can affect the sector as they are involved in importing of few parts or products (raw materials) from China.

- As digital penetration is increasing in India, the online consumer electronics and appliances market is expected to see a CAGR of 24.5% from 2019 to 2026, as per Business Wire.

- The urban region accounts for the majority of the total revenue of this sector. Some contributions can also be seen from the rural market since the launch of ‘Pradhan Mantri Ujjwal Yojana (PMUY)’ by the Government in 2016, which aims to provide clean cooking fuel and a clean environment to safeguard the health of women and children. PMUY project has shown a positive impact on the sector, from the rise in sales of the pressure cooker to the growth of 15% YoY in the overall performance.

Business Model

BGMAL is involved in the manufacture and sale of the kitchen, and home appliances, mainly popular in the domestic household segment and has its headquarters and factory in Tamil Nadu. The Company has 17 branches across India and 25000+ retail points, whereas in 2014, it had 18000 retail locations. BGMAL sells its products through distributors like modern retail stores, e-commerce websites, direct dealers and oil marketing companies such as BPCL, Indian Oil, HPCL and also exports its products to countries like the United Kingdom, United States of America, Mauritius, Sri Lanka, Japan and United Arab of Emirates. In 2018, the Company registered itself with alternative sale channels like the Canteen Stores Department (CSD), Central Police Canteen Store (CPC) and Tamil Nadu Police Canteen Stores (TNPC) and has also executed orders for the Government of Tamil Nadu in the past. In 2005, BGMAL was the first in India to receive ‘Green Label’ certification for high thermal efficient LPG stoves, and in 2010, the Company won the National Award for “Quality product in Micro, Small and Medium Enterprises.

COVID-19 Impact on the Company

The coronavirus pandemic has affected economies on a global scale, which impacted all the industries around the globe. The turmoil has led to a difficult situation for all businesses as they struggle to survive. BGMAL’s performance for Q4FY20 and Q1FY21 also got affected due to it, but the Company is expecting a revival in the Q2 and Q3FY21. Considering the current scenario, the demand for kitchen appliances will increase as the lockdown is getting eased slowly and also because of the increased cooking at home as people cannot venture out, leading to more kitchenware usage. However, BGMAL might lose its overall profit for FY21 as the Company lost revenue worth Rs.75.2 cr in Q1, due to strict lockdown rules which were imposed across the Country

Differentiating Strategies

- Diversified Product Portfolio and Integrated Distribution Network

BGMAL is a significant player in the kitchen appliances sector. It has a diversified range of products spread over 20+ categories such as LPG stove, Mixer Grinders, Table Top wet Grinders, Pressure Cooker and also a variety of electrical appliances like Fans, Water Heaters, Electric Irons, etc. In FY19, the Company opened 36 new stock-keeping units (SKUs) totaling it to 687. The Company also has tie-ups with various channels like online, modern trade, Tamil Nadu police canteen stores, etc. The launch of multiple products and expansion plans will increase the revenue flow in the future.

- Market Consolidation

BGMAL enjoys a strong presence in South India, which accounts for 77% of the Company’s total revenue. To grow its leadership position even further, the Company had designed a three-dimensional model growth strategy for its existing market Tamil Nadu, Kerala, and Andhra Pradesh. The strategy included:

– Increased promotional activities to increase the current market share

– Providing better post-sales services to attract new customers

– Cross-selling products to existing customers

BGMAL might not have much revenue inflow from the non-south regions. Still, the market consolidation strategy has helped the Company make more sales and generate more revenue annually than its peer Hawkins Cooker.

- Targeting New Markets

BGMAL is continuously aiming to increase its market share across the Country. The Company has focused on improving and strengthening its distribution network in non-south regions through channels like modern trade and various e-commerce platforms which will also help in having greater market penetration. The Company has been leveraging its existing leadership in the southern markets to step and expand profusely in the new markets.

- Increase in-house manufacturing

Until now, BGMAL has been manufacturing 80% of its products in its in-house manufacturing facility. The rest 20% of the products are being outsourced from China, including electric rice cookers, breakfast category products, etc. The Company aims to manufacture all of its products in India and not be dependent on any other country for the imports. The current COVID crisis has taken a toll on all nations’ financial conditions, accelerating towards deglobalization. So, to avoid any future contingencies, BGMAL aims to become self-reliant.

SWOT ANALYSIS

Strengths

- The Company has its own ‘State-of-the-Art’ manufacturing facility, which is equipped with the latest technology and ensures proper control of its products’ quality.

- The Company has 25000 retail points and over 550 distributors, which helps them provide post-sales service to its customers, allowing it to create an enhanced brand image.

Weakness

- A massive part of BGMAL’s revenue is generated from the Southern part of India, as the Company enjoys a high market share there. However, lack of diversification can affect the Company’s growth in the long run.

- Failure to estimate the seasonal demand timely is a big challenge for the Company. Lack of preparedness to meet the high order or overestimation of demand leads to overstocking and unnecessary spends on working capital.

- The Government of Tamil Nadu completed the distribution of the committed quantity of home appliances, to the eligible households, in 2016 itself. Hence, BGMAL did not receive any Government orders FY17 onwards, which led to lower revenue in the last four years.

Opportunities

- As the consumers are shifting more towards online shopping platforms, the Company can use innovative digital media marketing techniques to create more brand awareness and increase their revenue flow through the online channel.

- The increase in 0% finance schemes, credit cards, cashback schemes and affordable monthly instalment payments have changed the perception of customers and made those expensive, unaffordable products accessible to them. This will widen the target audience of the Company’s products.

- Factors such as demographics and lifestyle like an increase in the number of nuclear families can show positive trends and enhanced growth for the Company.

Threats

- The industry is highly fragmented, which increases competition across the industry. International companies that have entered the industry through mergers, joint ventures, etc., have further intensified the competition.

- Inflation rates have always followed the upward trend and is expected to follow the same trajectory in future as well, further decreasing the purchasing power of the customers and affecting the industry.

Michael Porter’s 5 Force Analysis

Barriers to entry

- Many competitors have emerged over time, attracted by the growth and returns of this industry. Importing cheap (both in terms of price and quality) products from China made it easier for these competitors to participate in the Indian market to fulfil their short-term agendas of profit-making. This causes price fluctuations in the market and affects the players focused on long-term growth, by providing sustainable and good quality products. The barriers to entry might be low, but sustainability is questionable.

Bargaining power of suppliers

- Though BGMAL has its in-house manufacturing facility, it needs to import raw materials that are extensively used in manufacturing its products. As the market is fragmented, the Company does not enjoy bargaining power over its suppliers and hence, is greatly affected by fluctuation in the prices of raw materials.

Bargaining power of buyers

- Due to the presence of intense competition, it is nearly impossible for BGMAL to hike prices as the customers can quickly switch to their peers.

- The current crisis has made customers even more price-sensitive and given them relatively higher bargaining power over the Company.

Threat of substitutes

- High due to great opportunities, massive potential, fragmentation and presence of unorganized as well as organized players.

Rivalry among competitors

- The kitchen appliances industry has seen enormous growth in the past few years, which has led many international brands to enter the market and further increase the competition. Industry, being highly fragmented, leads to an intense price war among competitors.

Branding and other initiatives

- Branding

BGMAL, over the past three decades, has built a brand name BUTTERFLY in the eyes of its customers by providing innovative and high-quality products. Also, by receiving and executing orders for the Tamil Nadu Government, they have created a distinct brand image in the southern markets.

Government orders received in FY16 gave a significant push to revenues, in the same year the Company ended up spending around Rs.68 cr. towards marketing & advertisement. This was done to accelerate branded sales which were affected due to Tamil Nadu floods and moderated festival sales during the year. Whereas in 2017, BGMAL did not receive any Government orders, also the effects of demonetization decelerated the branded sales and led to decreased profitability during the year. So, the Company started focusing more on advertisement and marketing of its products FY17 onwards. In FY20, BGMAL spent Rs.65 cr. as advertising expenses, which are approximately 10% of the total revenue for the year.

- New Product Launches

In 2014, BGMAL acquired the domestic kitchen and electrical appliances division of LLM appliances, one of its associate companies. This acquisition added more than 12 products to BGMAL’s product basket. The Company launched 16 new products during that year, including 12 products of LLM appliances, which increased BGMAL’s product categories to 20+, from 6 product categories in 2013. In FY20, the Company launched new innovative products in non-stick cookware items, LPG stove, blenders, choppers and also relaunched stainless steel vaccum flasks and water bottles with improved versions.

- Increasing Distribution Network and Brand Visibility

BGMAL has over 550+ distribution centres across the Country showcases a strong distribution network. The Company has seen growth in sales through various distribution channels like online and modern trade (supermarket chains) channels in the recent times and also reported a revenue of Rs.145 cr. in FY20 through the online sales, whereas it was only Rs.45 cr. in FY19. The Company has also been indulging in extensive branding and promotional activities across different media platforms such as television, magazines, and newspapers. The Company is also planning to invest in social media to influence through tie-ups with various influencers across the platform and increase brand visibility Pan-India.

Financial Analysis

- Segment Analysis

BGMAL has two major product segments: kitchen appliances and cooker/cookware. The Kitchen appliances sale grew by 0.68% YoY to Rs.517.8 cr. and the cookware segment sales grew by 18.20% to Rs.123.4 cr. in FY20. However, the growth was lower than FY19 supposedly due to the COVID impact but is expected to revive in Q2FY21. The overall sales growth was the highest in FY18 as the Company took the initiative to build a strong foundation in the channels like online, modern trade, corporates, etc. The PMUY scheme also contributed about 20-25% to the branded sales revenue. However, in FY17, the Company faced a setback due to various factors like demonetization, the cyclone in Chennai, and drought in Tamil Nadu.

- Profitability

BGMAL has been reporting a downward trend in its profits since FY13 due to weak consumer sentiments coupled with continuous fallout due to Telangana issue in FY14 and also deferment of Government tenders from FY15 to FY16 further fueled up the decline in profits in FY15. In FY17, the Company reported a net loss as its revenue was heavily impacted due to demonetization and absence of Government tenders. In Q4FY20, BGMAL reported a decrease in revenue by Rs.40 cr. due to COVID impact. A revenue growth of 13% was registered until Q3FY20, but disruptions in sales in Q4 led to reporting of 4.41% as the total revenue growth For FY20, further affecting the net profit.

The Company aims to reduce its fixed cost from Rs.10 cr. to Rs. 8 cr. (a reduction of 20%) through various ways one of which is by giving pay cuts to the employees, to contain the damage caused by COVID-19. The crisis is also going to affect the overall revenue for FY21, and the Company expects degrowth of 20-21% but is targeting a breakeven at PBT level.

- Debt Level.

In 2011, BGMAL received its first order of Rs.285 cr. from the Tamil Nadu Civil Supplies Corporation (TNCS) on behalf of the Tamil Nadu Government and to execute the same, it required more funds; hence it reported a higher debt-equity ratio in FY12. From the revenue it generated in FY12; it was able to sustain the expenditure for the subsequent year leading to a lower debt level. Whereas in 2014, a rise in debt-equity level was reported due to delayed payments of Government orders. The debt level of the Company has been quite volatile in past years, mainly due to the fluctuation in the revenue levels and also due to the need for funds to meet the demands for the products. The Company reported a total debt obligation of 160 cr. in FY20 and planned to take the additional short-term debt of of Rs.20-25 cr. for capacity expansion in Q2FY21 but expects to revert at the debt level of FY20 by the end of FY21.

When the debt level of BGMAL is compared to its peer Hawkins Cooker, it is visible that the Company has been undertaking higher debt obligations in the past years mainly due to need for funding to execute Government orders and to expand its distribution network across India.

- Interest Coverage Ratio

The ratio was affected due to fluctuations in the revenue flow of the Company over the years. In FY20, the coverage ratio seems to be low probably due to the disruptions in income in Q4 but is expected to remain moderate rest of the year on grounds of revival of demand.

- Inventory Turnover Ratio

The ratio had a downward trend from FY13 onwards due to disruption in the sale of the products because of various factors which also affected the Company’s profitability. High inventory turnover ratio was reported in FY12 and FY16 due to higher branded sales and completion of Government orders. The Company reported approximately 90 days of inventory turnover days in FY20 vs. 78 days in FY19, majorly due to the impact on sales in Q4. Still, BGMAL expects ten days reduction in inventory days as the demand is expected to increase in the latter part of FY21, and sales are expected to revive.

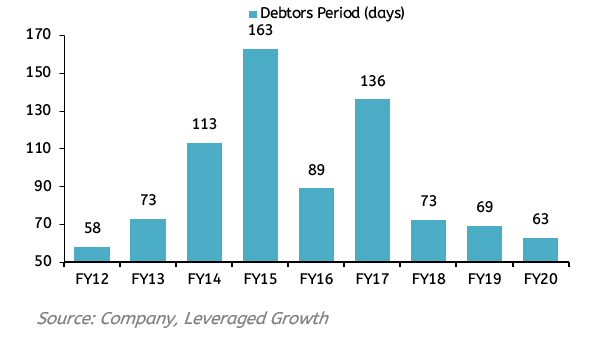

- Trade Receivables

BGMAL reported higher receivable days from the period ranging betweenFY14-FY17 due to failure in receiving timely payments for the Government supplies. Even though the stated number of receivable days in FY20 is lower when compared to FY19 but is slightly higher when compared to the estimations made by the management in the Q3FY20. Due to the sudden lockdown that happened towards the end of FY20, the Company failed to receive timely payments, further leading to the Company’s stretched working capital cycle in FY21.

Risk Analysis

- Geographical Concentration risk: BGMAL is a significant player in South India, and 80% of its revenue is generated from there. But lack of diversification gives an advantage to other competitors in terms of increased market share across India.

- Raw material price fluctuation: As BGMAL needs to import materials like stainless steel motors and ABS plastics, so the price of raw material is a crucial component for the Company. Any change in the price of raw materials can affect the cost of their products and lead to lower profit margins.

- Foreign exchange volatility: BGMAL is also involved in exporting its product in many countries like the United Kingdom, Sri Lanka, United States of America, etc. They have to deal with the fluctuation of the foreign currency rate. There has been significant fluctuation in the foreign currencies in recent times, and it is expected to continue in the future as well. The Company follows a policy of hedging 100% of its payables and has hedged around 61% of foreign exchange exposure.

- Global Economy: Due to COVID, the global economy has taken a hit, which has led to a decline in global financial conditions and trade disputes. BGMAL imports some products from China, but the increased tension between India and China might affect the Company until it completely shifts its sourcing requirements to India.

- Regulatory Changes: The Company is involved in the export and imports of its products and raw materials. So, any changes in the regulations can affect the operations of the Company.

Corporate Governance

- The Company’s board comprises 13 Directors, out of which seven Directors are independent, including one-woman Director. The composition complies with the SEBI (LODR) Regulations, 2015.

- Four directors, namely V.M. Balasubramaniam, V.M. Seshadri, V.M. Gangadharam, and V.M. Kumaresan, are brothers of Mr. V.M. Lakshminarayanan, other than this there are no inter-relationship among the other board members.

- The Company has one non-executive Director, Mr Anand Mundra, a member of the Private Equity Participants. However, none of the other directors of the Company hold Directorships in more than 20 companies or more than ten public companies, whether listed or not.

- Besides the 9 Board meetings held during FY19, a separate meeting was organized by the Independent Directors on April 6, 2018, to evaluate the performance of the non-independent directors and board as a whole, including the Chairman of the Company.

- A program for familiarization of Independent Directors was held to acquaint them with their roles, rights, and responsibility towards the Company and the industry’s nature in with the Company operates.

- The Promoter’s shareholding had a percentage change of 0.17, i.e., from 65.13% to 64.96% in FY19.

The End-Note

- The Covid-19 crisis has severely affected the industry, and the impact is quite visible in the Company’s financials. The losses faced in the last three months might prove burdensome for the Company in FY21 as well.

- The Management needs to focus on debt utilization and capacity expansion strategies to meet the demands projected by them.

- The Company is taking more debt as compared to its peers, so in future, if the Company is willing to grab an opportunity, it would have less legroom to take more debt.

- The continuous efforts of the management to expand its brand name in the non-south regions has shown results, and the Company aims to improve it even further in the future.

- In the current scenario, where more and more people are considering online shopping as the safest means to fulfil their needs, the Company should penetrate more funds in e-commerce platforms to keep up with the change in preferences of the consumers and also lessen its geographical restrictions.

Disclaimer: The report and information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent. This report and information herein is solely for informational purpose and may not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. Certain transactions -including those involving futures, options, another derivative products as well as non-investment grade securities – involve substantial risk and are not suitable for all investors. No representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. This information is subject to change without any prior notice. The Company reserves the right to make modifications and alternations to this statement as may be required from time to time without any prior approval. Leveraged Growth, its associates, their directors and the employees may from time to time, effect or have effected an own account transaction in, or deal as principal or agent in or for the securities mentioned in this document. They may perform or seek to perform investment banking or other services for, or solicit investment banking or other business from, any company referred to in this report. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting the document. This report has been prepared on the basis of information that is already available in publicly accessible media or developed through analysis of Leveraged Growth. The views expressed are those of the analyst, and the Company may or may not subscribe to all the views expressed therein. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject Leveraged Growth to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction. Neither the Firm, not its directors, employees, agents or representatives shall be liable for any damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The person accessing this information specifically agrees to exempt Leveraged Growth or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold Leveraged Growth or any of its affiliates or employees responsible for any such misuse and further agrees to hold Leveraged Growth or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

Contributor: Team Leveraged Growth

Co-Contributor: Pragya Pandey

Research Desk | Leveraged Growth